|

ASCLETIS-B(1672)

Analysis¡G

Ascletis Pharma¡¦s drug pipeline is mainly divided into three categories:

1. Metabolic disease pipeline, primarily focused on obesity treatment, emphasizing long-acting dosing and muscle preservation strategies. Products include:

• ASC30 once-daily oral tablet for obesity;

• ASC30 subcutaneous injection once monthly or less frequently for obesity;

• ASC47 subcutaneous injection once monthly or less frequently for obesity treatment without muscle loss.

2. Immunology pipeline, focused on IL-17 inhibitors targeting autoimmune diseases such as psoriasis. The main product is ASC50, an oral small-molecule IL-17 inhibitor for psoriasis.

3. Expanded indication pipeline, targeting acne, metabolic dysfunction-associated steatohepatitis (MASH), etc. Products include:

• ASC40 for moderate-to-severe acne;

• ASC40 for recurrent glioblastoma (rGBM);

• ASC40 for MASH;

• ASC61 for solid tumors.

The Group has made good progress in its metabolic disease pipeline:

* ASC30: U.S. Phase Ib trial (28 days) showed placebo-adjusted mean weight loss of up to 6.5%, with good tolerability, no serious adverse events, and mild gastrointestinal side effects. A U.S. Phase IIa trial (13 weeks) has been initiated, with enrollment of 125 subjects expected to complete in August 2025; top-line data anticipated in Q4 2025.

* ASC30 (injectable): U.S. Phase Ib trial showed a single-dose half-life of 36 days, supporting monthly or less frequent dosing; sterile solution suitable for combination therapy. U.S. Phase IIa trial (12 weeks) has begun with first subject dosed; enrollment expected to complete in 2025, top-line data in Q1 2026.

* ASC47: Australian Phase Ib trial showed a half-life of up to 40 days, supporting monthly to bi-monthly dosing, with good tolerability, no serious adverse events or increased heart rate. A U.S. combination trial with semaglutide has been initiated, with enrollment of 28 subjects expected to complete in July 2025; top-line data in 2025. Preclinical DIO mouse studies showed that low-dose combination with semaglutide achieved 56.7% greater weight loss than semaglutide alone, and restored muscle mass to healthy levels.

* ASC35: Selected as a clinical development candidate on October 13, 2025, supporting monthly dosing.

* ASC36: Selected as a clinical development candidate on October 30, 2025, for monotherapy in cardio-metabolic diseases and combination therapy focused on obesity. On November 12, 2025, a stable co-formulation with ASC35 was announced, with no aggregation or precipitation due to fibrosis. An IND application to the U.S. FDA is expected in Q2 2026.

In early November, the Group presented multiple obesity drug candidates, including ASC30 and the ASC31 + ASC47 combination therapy, via posters at ObesityWeek 2025 in Atlanta, Georgia, USA, demonstrating continued strong progress in its small-molecule and peptide obesity pipeline.(I do not personally hold the above stock.)

Strategy¡G

Buy-in Price: $13.00, Target Price: $14.50-$15.20, Cut Loss Price: $12.20

|

CANSINOBIO(6185)

Analysis¡G

CanSino Biologics, as a technological frontrunner in China's innovative vaccine landscape, has achieved a turnaround in its financial performance in the short term, leveraging the exclusive advantage of its tetravalent meningococcal conjugate vaccine (Menhycia ™). In the medium term, the volume expansion of its 13-valent pneumococcal conjugate vaccine (iPneucia™) and international expansion are expected to unlock new growth opportunities. In the long run, its globally innovative pipeline, including the inhaled tuberculosis vaccine, possesses significant technological barriers and market potential. The company's financial condition continues to improve, with net profit turning positive in the first three quarters of 2025. However, attention should be paid to uncertainties in pipeline progress, intensifying industry competition, and sustainability of profitability. We believe the company still has upside potential from the current price, with the investment thesis centered on a triple-threat driven by "commercial product scaling + R&D pipeline delivery + internationalization breakthroughs."

Strategy¡G

Buy-in Price: $46.00, Target Price: $51.90, Cut Loss Price: $43.88

|

|

FLAT GLASS (6865 HK) - FY25Q3 Saw Significant Improve, as the Anti-Excessive Competition Measures Strengthened

Investment SummarySignificant Performance Improvement in Q3 2025

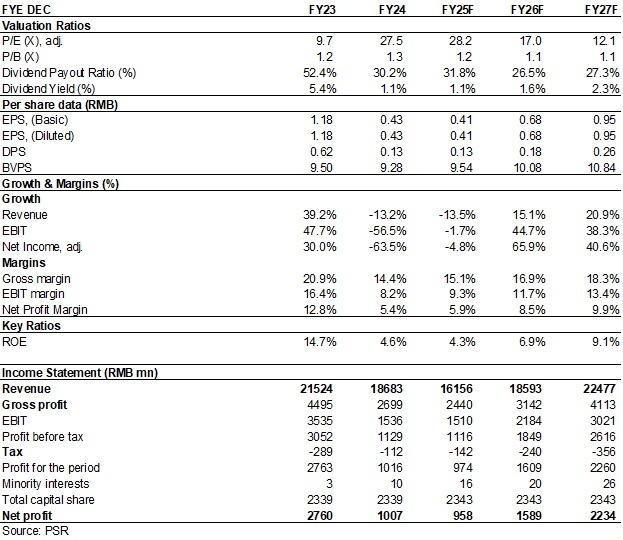

According to the Company's announcement, in the first three quarters of 2025, Flat Glass Group Co., Ltd. recorded revenue of RMB12.464 billion (RMB, the same below), down 14.7% yoy, and net profit attributable to the parent company of RMB638 million, down 50.8% yoy. Specifically, the Company recorded revenue of RMB4.079/3.658/4.727 billion in Q1/Q2/Q3, down 28.8%/26.4%/up 21.0% yoy and flat/-10.3%/up 29.2% qoq; net profit attributable to the parent company amounted to RMB106/155/376 million, down 86.0%/79.0%/up 285.5% yoy and up 136.7%/46.0%/142.9% qoq, respectively. The results showed a trend of improvement quarter by quarter, with particularly notable growth in Q3.

Anti-Excessive Competition Measures Strengthened, Driving Recovery in Profitability

The performance improvement was mainly driven by the accelerated inventory de-stocking that led to a recovery in industry prosperity, easing of cost pressures, and the support from overseas business (accounting for approximately 30%).

In 2025, the photovoltaic (PV) industry intensified its efforts to curb excessive competition. As of July 2025, the cold-repair capacity in the PV glass industry reached 7,750 tonnes/day, reducing the domestic operating capacity to 89 thousand tonnes/day---a decline of approximately 22.4% from the peak of 114.7 thousand tonnes/day in November 2024. This accelerated capacity reduction strengthened supply-side constraints, which supported PV glass price stabilisation. In July, prices bottomed out, followed by a rebound in August. In September, the price of 2.0mm PV glass rose 18% month-on-month to RMB13--13.5/sq.m, recovering approximately 25% from July's RMB10.5/sq.m.

The Company's gross margin for the first three quarters was 15.1%, down 3.9 ppts yoy. In Q3, gross margin reached 16.8%, up 10.8 ppts yoy and 0.1 ppt qoq, benefiting from increased shipments driven by price recovery, a decline in soda ash costs, and support from high-margin overseas business. The Q3 period expense ratio stood at 6.9%, down 3.7 ppts yoy and 0.6 ppt qoq, mainly attributable to scale effects. Additionally, a reversal of asset impairment losses of RMB80 million in Q3 further boosted profit. As a result, the Q3 net profit margin attributable to the parent company rose to 7.96%, up 13.2 ppts yoy and 3.7 ppts qoq.

Industry Expected to Maintain Weak Balance in Q4

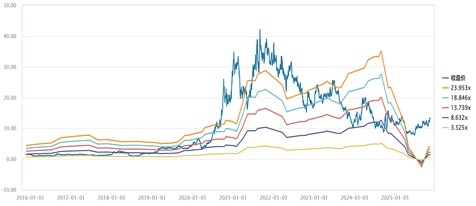

As of early November 2025, PV glass prices declined slightly due to weakening demand support, and industry inventories showed an increasing trend. The mainstream transaction price for 2.0mm PV glass was around RMB12.5--13/sq.m. However, considering the onset of the heating season and the resulting increase in natural gas prices, cost support is expected to limit the extent of price fluctuations. Benefiting from its advantages in technology, scale, capital, and clientele, the Company's cost advantages will become more prominent as market prices decline, potentially leading to an expansion in market share. The Company showed a clear downward trend in inventory in Q3. As of the end of Q3 2025, the Company's inventory balance stood at approximately RMB1.207 billion, down RMB751 million qoq, with a possible slight rebound in Q4. As of the end of September 2025, the Company's cumulative operating capacity totalled 16,400 tonnes/day, down 15% from the beginning of the year. The Company's two lines in Anhui (2,400 tonnes/day) and four lines in Nantong (4,800 tonnes/day) will commence operation based on market conditions. The two new production lines in Indonesia (3,200 tonnes/day) are expected to have a long construction period and will not commence production for at least two years. Investment ThesisDespite short-term pressure on industry prices, as a leading PV glass manufacturer, Flat Glass remains an industry leader in both scale and profitability. With continuous expansion of its overseas capacity, its profitability is expected to reach new heights. We expected the company's EPS for 2025/2026/2027 to be 0.41/0.68/0.95 yuan, respectively, and adjust the target price to HK$14.4, corresponding to a valuation ratios of 32.3/19.5/13.8x P/E and 1.4/1.3/1.2x P/B for the respective years, with an downgrade rating to "Accumulate." (Closing price as at 13 November 2025) P/E Band

Source: Wind, Phillip Securities Hong Kong Research Financials

(Closing price as at 13 November 2025) Click here to download PDF version...

| Recommendation on 17-11-2025 | | Recommendation | Accumulate (Downgrade) | | Price on Recommendation Date | $ 12.600 | | Suggested purchase price | N/A | | Target Price | $ 14.400 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|