|

CHINA SANJIANG(2198)

Analysis¡G

China Sanjiang Fine Chemicals is primarily engaged in the production and supply of chemical products, including ethylene oxide, ethylene glycol, polypropylene, MTBE (methyl tert-butyl ether), butadiene, ethanolamine, and surfactants. Despite facing numerous challenges, the Group¡¦s vertically integrated structure, diversified raw material procurement capabilities, and flexible market response strategies have led to a significant improvement in profitability in the first half of this year. Compared with the same period in 2024, profit attributable to shareholders surged 95.5% to RMB 301 million, driven mainly by favorable market trends for key products (especially ethylene glycol) combined with the Group¡¦s agile and adaptable operational strategies.

Robust downstream demand from the polyester industry continued to drive notable increases in the average selling price and gross margin of ethylene glycol. At the same time, in response to changes in the external market¡Xincluding the impact of U.S. tariffs on ethane exports to China¡Xthe Group dynamically adjusted its procurement strategies, raw material mix, and production portfolio to maintain competitive advantages in cost efficiency and product pricing. Operationally, the Group continued to benefit from the full-cycle integrated operations of its sixth-phase ethylene oxide/ethylene glycol production facilities and light hydrocarbon utilization units. On the other hand, the flexible ability to rebalance inputs of naphtha, ethane, propane, and methanol enabled the Group to optimize raw material costs and reduce exposure to price volatility of individual commodities. This integration also enhanced the ability to rapidly adjust product mixes, capturing favorable price spreads in ethylene oxide, ethylene glycol, butadiene, and surfactants.

In terms of product performance, ethylene glycol remained a standout, with both average selling price and gross margin recording strong growth compared to the same period in 2024. Butadiene has maintained strong momentum since 2024, supported by healthy demand from the synthetic rubber and automotive sectors. Ethylene oxide and surfactants benefited from stable demand in household cleaning, construction chemicals, and industrial applications. The Group expects demand for ethylene glycol, butadiene, and surfactants to remain solid, while pricing for polypropylene and ethylene oxide is expected to stay stable, with growth potential if downstream demand continues to recover. The Group will continue to pursue opportunities in high-value-added products and further downstream integration to enhance revenue resilience. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $2.82, Target Price: $3.15, Cut Loss Price: $2.67

|

HESAI-W(2525)

Analysis¡G

Hesai Group is a global leader in 3D light detection and lidar solutions. Its lidar products are applicable across multiple fields, including (i) passenger and commercial vehicles equipped with advanced driver-assistance systems (ADAS), and (ii) autonomous vehicle fleets for passenger and freight transportation, robotics, and other non-automotive industries such as automated guided vehicles/autonomous mobile robots, delivery robots, agricultural vehicles, a wide range of industrial applications like port and yard automation, as well as stationary applications or robotics. According to the Gaishi Auto Research Institute's installed capacity ranking of automotive lidars from January to August, Hesai continued to rank first in the industry in terms of installed primary automotive lidars in August. Hesai has maintained the top market share in primary lidars for seven consecutive months while achieving rapid growth, with its market share rising to 46%. This year, Hesai's lidars have supported the launch of several popular vehicle models, such as the Li Auto L6, Xiaomi SU7, and Leapmotor C10. Hesai has secured mass production designations for over 120 vehicle models from 24 OEMs, with deliveries scheduled to take place between 2025 and 2027. As a global leader in lidar technology, Hesai benefits from explosive demand in intelligent driving (ADAS) and robotics. The company is expected to achieve dual growth in revenue and profitability by 2025, with an overall optimistic long-term development outlook.

Strategy¡G

Buy-in Price: $187.90, Target Price: $213.00, Cut Loss Price: $173.30

|

|

NetDragon Websoft (0777.HK) - Deepening the `AI+Gaming` Strategy

Company profile

NetDragon Websoft Holdings Ltd. is primarily an investment holding company engaged in gaming and application services, as well as Mynd.ai operations. The company is a leading developer, operator, and distributor of online games in China and one of the first domestic online game enterprises to expand globally and operate successfully. It has independently developed multiple acclaimed online and mobile games, including Conquer, Age of Armor, and Heroes of Soul. Its products now reach game markets in over 180 countries and regions, supporting 11 languages, including English, French, Spanish, and Arabic. The company`s globally leading education solutions provider, Promethean, has achieved integrated innovation in product technology by combining its outstanding educational hardware and software with NetDragon`s proprietary 101 series products. For many years, Promethean has maintained a leading position in the global K-12 interactive display device market, ranking first in international market share.

Performance Summary

In the first half of 2025, the company reported revenue of approximately RMB 2.4 billion, a decrease of 27.9% year-on-year, primarily due to business adjustments. Gross profit was RMB 1.7 billion, down 24.7% year-on-year, while the gross profit margin increased by 2.9 percentage points to 69.5%. Net profit attributable to owners was RMB 30 million, a decline of 92.5% year-on-year, mainly due to intangible asset impairment losses and one-time expenses.

By business segment, gaming and application services revenue was RMB 1.7 billion, down 18.1% year-on-year, largely due to temporary factors. As cost reduction and efficiency improvements took effect, operating expenses for gaming and application services decreased by 14.7% year-on-year. Mynd.ai revenue was RMB 641 million, a decline of 45.7% year-on-year, primarily driven by customer budget cuts amid macroeconomic uncertainties. The company remains committed to shareholder returns and plans to distribute an interim dividend of HKD 0.5 per share for 2025, representing a 25.0% year-on-year increase.

Performance Review

Gaming and Application Services: Deepening the `AI + Gaming` Strategy and Building Evergreen Ips

In the first half of 2025, China`s gaming market achieved actual sales revenue of RMB 168 billion, a record high with a year-on-year increase of 14.1%. Among the top 100 mobile games by revenue, RPG games were the most numerous, accounting for 21.0%. The company`s gaming business has a strong foothold in the MMORPG segment, with three evergreen IPs (Age of Armor, Conquer, and Heroes of Soul). MMORPG is the longest-standing and most player-accumulated genre in China. Due to the appeal of its core gameplay, it boasts higher ARPU and user stickiness than the industry average.

Among its core IPs, the flagship evergreen IP Age of Armor continues to enhance content quality and has launched multiple collaborations with renowned projects, such as intangible cultural heritage initiatives and social welfare programs, driving sustained growth in user engagement. Its MAU has surpassed 2.5 million. Additionally, Age of Armor is an original design, accounting for 89.0% of game revenue, with low risk of IP dilution, maintaining a high operating profit margin. The highly anticipated new title Code: MY, developed by the original veteran design team, adopts a mature and proven business model while optimizing core pain points.

The Conquer IP has achieved an MAU of over 850,000, making solid progress in overseas expansion and content consumption. Overseas revenue now accounts for over 60.0% of the total, igniting the competitive spirit of global players and achieving regional resonance. Localized gameplay has accelerated its overseas expansion. The Heroes of Soul IP has successfully leveraged its "content + esports" engine, with the PC version maintaining year-on-year growth for five consecutive half-years. A collaboration with the domestic animation The Unyielding has driven APA growth.

The strategic layout of `AI + Gaming` continues to deepen, with significant results in cost reduction and efficiency enhancement, and innovation in user gaming experiences. According to management, AI has improved overall efficiency by approximately 15.0%, with some content achieving end-to-end AI production, and initial establishment of AI production centers and talent teams. Meanwhile, through multiple AI NPCs forming a complete minimal ecological cycle, the game achieves full AI generation and experience enhancement for elements such as mythical beasts and bosses.

In the application services sector, the company continues to deepen its strategy of fully embracing AI. Its domestic education technology business focuses on key AI projects, including national-level platforms, and the vocational education segment. The company has collaborated with the Thai Ministry of Higher Education to provide vocational skills training, such as electric vehicle technology, for university students and youth. Additionally, the Hong Kong subsidiary, Cherrypicks, has introduced strategic investment from Wenge, transforming into its exclusive overseas platform and commercialization partner, facilitating the deployment of China`s leading AI technologies in Hong Kong, Macau, and overseas markets.

Mynd.ai

Mynd.ai is a U.S.-listed company, with NetDragon holding a 74% stake as of the end of 2024. Its operating revenue primarily comes from hardware product sales under the Promethean brand and SaaS subscriptions for lesson preparation and delivery software. As a leader in K-12 classroom interactive displays, the Promethean brand offers a combination of hardware and software (interactive display devices and smart whiteboard software), enabling interactive teaching and collaboration. According to Futuresource and Technavio, the education technology market is expected to reach USD 300 billion by 2028, with the educational interactive display hardware market projected to reach USD 5 billion. Futuresource statistics show that as of the end of 2024, 8.89 million interactive display devices were installed in the global education market (excluding China), of which Promethean accounted for 1.37 million cumulative sales from 2016 to 2024, ranking first in the existing equipment market.

The company continues to adjust its strategic positioning, launching the ActivPanel SuiteTM software to empower SaaS across various operating systems, driving the evolution of its business model towards SaaS. In the first half of 2025, SaaS subscriptions increased by 8.0% quarter-on-quarter, with SaaS subscriptions from ActivSuite gradually rising alongside the shipment of new-generation hardware products.

In the third quarter of 2025, Mynd.ai accelerated the development of its AI solutions business by acquiring the AI voice technology company Merlyn Mind, significantly enhancing the interactive experience of its full ecosystem of hardware and software products in classroom teaching scenarios. The company`s voice assistant technology can build smart classroom interaction systems, helping teachers break free from the constraints of the podium and promoting teaching automation and content diversity. This strategic move is not only expected to strongly drive AI SaaS revenue growth but is also a key step in fully empowering the SaaS product line and enhancing the overall attractiveness of the product portfolio.

Company valuation

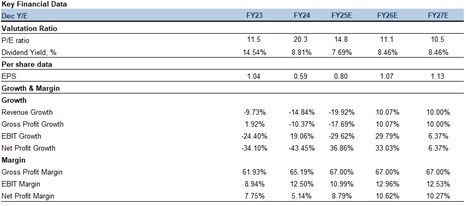

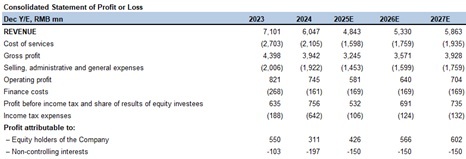

NetDragon`s gaming business maintains steady growth, with its Age of Armor series demonstrating exceptional long-term operational capabilities. AI technology is widely applied across business segments, effectively driving cost reduction and efficiency improvement. The education technology segment leads the industry in global expansion, with diverse investment project layouts and significant results. Therefore, we forecast the company`s revenue for 2025-2027 to be RMB 4,843/5,330/5,863 million, respectively, and net profit attributable to owners to be RMB 426/566/602 million, corresponding to EPS of RMB 0.81/1.07/1.14. The current stock price corresponds to a PE of 15/11/10x. Considering the significant results of the company`s platform transformation, we assign a 16x PE ratio for the 2025 forecast, corresponding to a target price of HKD 14.1 per share. We initiate coverage with a "Accumulate" rating.

Risk factors

1) Delays in new game launch;

2) Weaker-than-expected industry demand;

3) Cryptocurrency price volatility.

Financials

Current Price as of: Nov 10

Source¡G PSHK Est.

Download PDF version...

| Recommendation on 12-11-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 11.900 | | Suggested purchase price | N/A | | Target Price | $ 13.600 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|