|

AUX ELECTRIC(2580)

Analysis¡G

AUX Electric is one of the world¡¦s top five air conditioner providers. Its business covers the design, R&D, production, sales, and related services of household and central air conditioners. Household air conditioners include wall-mounted units, cabinet-style, and mobile units, and other categories; central air conditioning systems include VRF systems, packaged units, heat pumps, chillers, and terminal devices. Its rich product line meets numerous application scenarios such as residential homes, office buildings, shopping malls, hotels, hospitals, and industrial parks. The group¡¦s business footprint covers 150 countries and regions worldwide and is also the leading brand for household air conditioners in China¡¦s mass market. It benefits from factors such as the incremental demand driven by rural revitalization policies and urbanization processes in lower-tier markets, as well as increasing consumer focus on cost-effectiveness. The group leverages its extensive sales network and cost-effective product advantages, while employing a multi-brand strategy to meet the diversified consumption needs of different markets.

To reflect its pioneering spirit, the group named itself with the transliteration of the English word for ¡§ox,¡¨ namely ¡§AUX,¡¨ and uses ¡§AUX¡¨ as its main brand to layout domestic and overseas markets. It further enhances market penetration through a multi-brand portfolio including ¡§Hutssom¡¨ and ¡§AUFIT,¡¨ with plans to launch premium brands in the future to reach a broader global consumer base. Facing industry competition, the group actively expands overseas business, launches multiple high-quality products tailored to local needs, and continues to advance its OBM strategy, achieving steady growth in operations. In the first half of 2025, total operating revenue reached RMB 20 billion, up 16.7% year-on-year. Among this, export revenue grew 28% to RMB 10.839 billion, while export OBM revenue surged 71%; net profit attributable to shareholders reached RMB 1.872 billion, up 5.1%.

In terms of overseas layout, targeting ultra-high temperature and dusty usage scenarios in the Middle East, it launched T3 inverter wall-mounted units incorporating R32 inverter + refrigerant cooling technologies, overcoming challenges in high-temperature attenuation and inverter drive reliability. In the Saudi market, the R32 inverter model achieved sales exceeding 300,000 units in just half a year after launch, accounting for approximately 80% of total sales in Saudi Arabia. For the ASEAN market, focusing on user needs and special usage scenarios, it continuously upgrades products; for example, in Vietnam, to cope with sideways motorbike transportation and coastal salt/humidity conditions, it introduced products equipped with 6th-generation inverter control technology, heat exchanger, and electronic control anti-corrosion processes, ensuring product reliability and durability. The group has deployed localized sales teams in Vietnam, the UAE, and Saudi Arabia, and initiated localized operations. On the product side, it deeply integrates AI technology, cloud voice capabilities, and AIoT technology. Its independently developed AI intelligent control system deeply integrates AUX¡¦s self-developed large model with Deepseek technology, enabling multiple modes of interaction ¡V such as offline/online voice, mobile app. According to Sullivan statistics, the group ranked first in national sales of smart voice-controlled air conditioners for three consecutive years from 2022 to 2024. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $15.50, Target Price: $16.70, Cut Loss Price: $17.40

|

GIGADEVICE(603986.CH)

Analysis¡G

The company is a leading domestic manufacturer of storage chip design, offering products such as NOR Flash (non-volatile memory) and DRAM (volatile memory). It is also actively developing and researching MCU (microcontroller) and related peripheral products. Its products are widely used in handheld mobile terminals like smartphones and tablets, consumer electronics, IoT devices, personal computers and peripherals, as well as automotive electronics and industrial control equipment. The company's core businesses include flash memory chip products, microcontroller products (MCU), sensor modules, and dynamic random-access memory (DRAM). The sensor business is operated through the acquisition of Shanghai Silil Microelectronics Technology Co., Ltd. in 2019. In the first three quarters of 2025, the company achieved operating revenue of 6.832 billion yuan, a yoy increase of 20.92%; net profit attributable to the parent company was 1.083 billion yuan, up 30.18% yoy. Benefiting from the rising storage price cycle, the company's profitability significantly improved, with Q3 alone reporting net profit attributable to the parent company of 508 million yuan, up 61.13% yoy and 48.97% quarter-on-quarter. Gross margin reached 40.72%, an increase of 3.71 percentage points quarter-on-quarter. Currently, AI continues to drive demand growth in sectors such as smartphones, PCs, and servers, positioning the company's products to benefit further.

Strategy¡G

Buy-in Price: RMB220.80, Target Price: RMB259.00, Cut Loss Price: RMB200.00

|

|

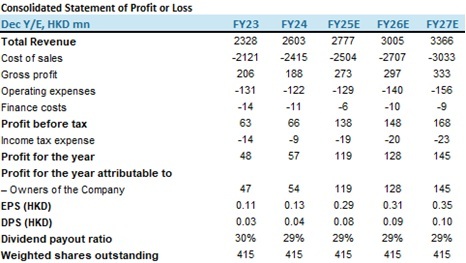

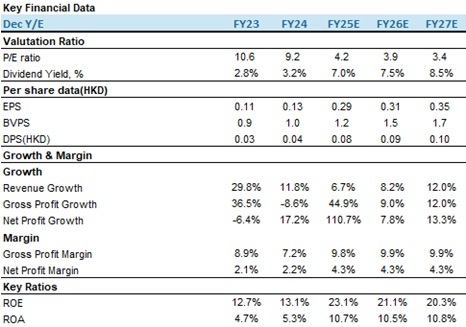

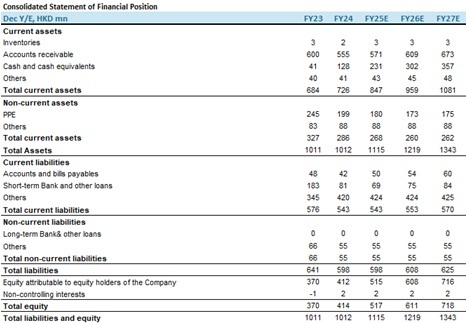

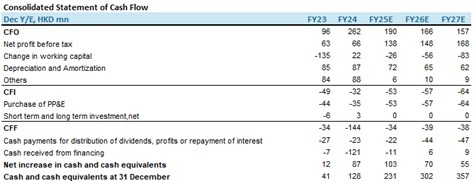

BAGUIO GREEN (1397.HK) - Driven by both policy dividends and profitability improvement, the leading position is securely maintained

OverviewBaguio Green ("Baguio") was established in 1980 and is one of Hong Kong's largest integrated environmental services groups, providing services such as environmental hygiene, resource recycling, waste recovery and recycling, green technology, organic fertilizer production, landscaping projects, pest control, and waste management. The company's main business is primarily divided into four segments, including: (1) cleaning services; (2) waste treatment and recycling business; (3) landscaping services; and (4) pest management business. Its clientele spans various industries and types of organizations, such as government departments, public organizations, and multinational corporations. Net Profit Surged in H1 2025, Profitability Improved SignificantlyBenefiting from revenue growth in the Cleaning and Landscaping segments, the Company's revenue for the first half of 2025 reached HKD 1.354 billion, representing a year-on-year increase of 4.8%. The Cleaning business, being the core operation, generated revenue of HKD 1.08 billion, up 4% year-on-year, accounting for 79.6% of the total revenue. Revenue from the Waste Management and Recycling business was HKD 150 million, down 1.4% year-on-year, accounting for 10.7% of the total revenue. The Landscaping business reported revenue of HKD 100 million, a significant increase of 40.9% year-on-year, accounting for 7.4% of the total revenue. The Pest Management business generated revenue of HKD 32 million, down 16.7% year-on-year, accounting for 2.3% of the total revenue. Benefiting from effective cost control and a decrease in financial expenses, the gross profit margin was 9.8%, an increase of 2.3 percentage points year-on-year. The gross profit for the Cleaning business was HKD 850 million, an increase of 27.4% year-on-year, with a gross margin of 7.9%, up 1.5 percentage points year-on-year, primarily due to new cleaning service contracts with various government departments and different organizations. The gross profit for the Waste Management and Recycling business was HKD 28 million, up 46.6% year-on-year, with a gross margin of 19.2%, a substantial increase of 6.3 percentage points year-on-year, mainly driven by the government's active promotion of recycling, significant expansion of the recycling point network including food waste, which facilitated public participation and effectively stimulated collection volumes, as well as contributions from the green technology business. The gross margin for the Landscaping business was 19%, an increase of 5.7 percentage points year-on-year. The gross margin for the Pest Management business was 3.6%, a decrease of 1.5 percentage points year-on-year. Net profit surged by 128.1% year-on-year to HKD 59 million. Earnings per share (EPS) for the first half of 2025 already reached 14.2 HK cents, surpassing the full-year 2024 EPS of 13.0 HK cents, representing a remarkable year-on-year increase of 142.7%. From 2021 to 2024, the Company's EPS achieved a compound annual growth rate (CAGR) of 61%. The average accounts receivable turnover days were 69 days, a decrease of 4 days compared to the end of 2024. The average accounts payable turnover days were 46 days, a decrease of 8 days compared to the end of 2024, demonstrating improved working capital turnover efficiency and faster collection times. Net cash generated from operating activities was HKD 200 million, an increase of 36.8% year-on-year. Available cash and bank balances were approximately HKD 291 million, an increase of 127.1% compared to the end of 2024, further proving the high quality of the Company's earnings and its sound financial health. Securing First Large-Scale Marine Cleaning Contract, Marking a Strategic Business BreakthroughThe company's cleaning services span across various districts in Hong Kong, comprehensively covering venues such as hospitals, police stations, streets, recreational facilities, airports, exhibition centers, the public stands of the Jockey Club, and universities. The company has been awarded the "Eastern Waters Marine Cleaning Contract" by the Hong Kong Marine Department. This three-year contract, effective from October 1, 2025, with a total value of HK$150 million, covers key areas of Hong Kong's eastern waters. These include internationally renowned landmarks like Victoria Harbour, Central, Causeway Bay, and Tsim Sha Tsui, as well as ecologically sensitive areas such as Sai Kung and Tolo Harbour. The services encompass marine debris clearance and the collection of domestic waste from vessels, playing a critical role in protecting Hong Kong's marine ecosystem and maintaining the city's image. The contract signifies a crucial breakthrough for Baguio Green, expanding its operational scope from land to sea, and stands as a significant milestone in its comprehensive environmental service capabilities. It will help further consolidate the market position of its core cleaning services business. Furthermore, as a key component of the environmental services supporting the Hong Kong government's "event-based economy," the contract strengthens the Group's long-term collaborative relationship with the government and lays the groundwork for undertaking high-value-added environmental projects in the future. Awarded Long-term Government Contracts; Green Technology Monetization Potential Awaits VerificationBaguio Green is a core service provider for the Hong Kong Environmental Protection Department (EPD) and plays a pivotal role in the recycling sector. The company provides collection services for thousands of recycling points across Hong Kong, covering various materials such as plastics, glass bottles, and waste paper. It has secured two contracts from the EPD with a total value of HK$43 million. Both contracts have a term of 35 months and primarily involve operating the "Green @ Tai Wo" and "Green @ Po Lam" recycling stations. These are key projects within the government's "Green Outreach" community recycling network. The high gross profit margin of the recycling business indicates significant profit elasticity, meaning its contribution to overall profits will far exceed its revenue share. The company is actively promoting green technology products, including office food waste recycling bins, smart scales, and solar-powered compacting recycling bins. It has won a new contract to supply the government with a new generation of solar-powered waste compaction bins. In the future, the company is expected to launch more green technology products, unlocking market potential and securing more new contracts. Producer Responsibility Scheme (PRS) Expected to Drive Growth in Both Volume and Price for Baguio Green's Recycling BusinessThe Producer Responsibility Scheme (PRS) is expected to significantly increase the recycling volume of plastic beverage containers and beverage cartons. The recycling volume for plastic bottles and beverage cartons is projected to grow 2-3 times over the next three years, creating incremental market space for Baguio Green's waste treatment and recycling business. As a leading recycling service provider in Hong Kong, the company, leveraging its existing smart recycling technology, government collaboration foundation, and recycling network advantages, is well-positioned to handle a majority of the new recycling demand. This is expected to drive the expansion of its recycling business revenue scale and help maintain high gross margins, making it a core beneficiary of the PRS implementation. Investment ThesisAs a leading player in Hong Kong's recycling services industry, Baguio Green is poised to continue benefiting from policy dividends, including the Plastic Beverage Container and Beverage Carton Producer Responsibility Scheme and the Northern Metropolis development. The government is advancing the Northern Metropolis initiative at full speed, with four new development areas---including Kwu Tung North/Fanling North, Hung Shui Kiu/Ha Tsuen, Yuen Long South, and the San Tin Technopole---already in the construction phase. Upon completion, all of Baguio's business segments are expected to benefit. As of June 30, 2025, the company's total contract value on hand amounted to approximately HK$3.1 billion, of which about HK$1.044 billion is expected to be recognized by the end of 2025. This indicates strong short-term earnings visibility and a solid foundation for long-term growth. Baguio's customer base primarily consists of government bodies, quasi-public organizations, and public utility providers, which collectively contribute 85% of the company's revenue. Demand from these clients is relatively resilient to economic cycles, underpinning stable and sustainable earnings. In addition, the company has maintained a consistent dividend policy, with a payout ratio of around 30% for five consecutive years. Baguio management expressed that it is actively seeking suitable merger and acquisition opportunities---such as property management-related companies---with the goal of achieving vertical integration across the entire industry chain. If successful, this could lead to economies of scale, further reducing costs, improving efficiency, and enhancing profitability. We forecast the company's EPS for 2025 to 2027 to be 29, 31, and 35 cents, respectively. Our target price is HK$1.55, implying a forward P/E ratio of 5x for 2026. We assign a "Buy" rating. Risk factors1) Intensifying industry competition;

2) Sharply rising operating costs;

3) Slowing service demand. Financial

(Current Price as of: 31 Oct 2025)

Source: PSHK Est. Download PDF version...

| Recommendation on 4-11-2025 | | Recommendation | Buy | | Price on Recommendation Date | $ 1.200 | | Suggested purchase price | N/A | | Target Price | $ 1.550 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|