|

CHINA OILFIELD(2883)

Analysis¡G

China Oilfield Services Limited (COSL) announced its third-quarter results for the period ended 30 September 2025, prepared under China Accounting Standards. Revenue for the quarter reached RMB 11.533 billion, reflecting a year-on-year increase of 3.6%, consistent with the 3.5% growth seen in the first half of the year. Net profit surged to RMB 1.246 billion, marking a strong 46.1% rise compared to the same period last year¡Xa notable acceleration from the 23.3% growth recorded in the first half. This robust profit expansion was primarily driven by higher utilization rates of large-scale equipment and the steady, high-day-rate operations of the North Sea semisubmersible platform. Earnings per share stood at RMB 0.26, up 44.4% year-on-year.For the first nine months of 2025, the company achieved revenue of RMB 34.853 billion, representing a 3.5% increase over the prior year, while net profit attributable to shareholders rose 31.3% to RMB 3.209 billion.

Throughout the year, the energy services market has faced heightened uncertainty and volatility, with oil prices under increasing downward pressure at their core levels. Despite these challenges, COSL has remained firmly focused on supporting reserve growth and production enhancement. The company has continued to deliver high-quality equipment for high-value exploration and efficient production, while establishing a robust technology support framework and enhancing comprehensive, end-to-end risk management systems. These initiatives have significantly bolstered the company¡¦s resilience and contributed to steady performance with positive momentum.In drilling services, the group¡¦s rigs operated for a total of 14,784 days in the first nine months, a 12.3% increase year-on-year. Jack-up rigs contributed 11,624 operating days, up 9.7%, while semisubmersible rigs recorded 3,160 days, reflecting a 22.9% rise. Overall calendar-day utilization improved to 90.3%, an increase of 11.6 percentage points, with jack-ups achieving 92.6% and semisubmersibles reaching 82.7%.

In well services, the group has consistently powered its technology-driven growth engine. By building a core technology system grounded in fundamental research and deepening integration across the industrial and innovation chains, it has successfully extended technical capabilities toward both upstream demand and downstream applications. As a result, the workload of main business lines of well services continued to grow during the first nine months.

In marine support services, COSL operated and managed over 200 vessels by the end of the third quarter, with cumulative operating days totaling 62,589¡Xan increase of 9,427 days, or 17.7%, compared to the previous year. The company has further strengthened its leading position in the domestic market, improved equipment resource reserves and deployment flexibility, and introduced an innovative ¡§Vessel+¡¨ service model to address diverse client requirements.

For geophysical acquisition and surveying services, the group strategically concentrated limited production capacity on high-return activities, and optimized and adjusted the layout of certain production capacity. Consequently, 2D acquisition operation volume was 5,845 kilometers, down 61.8% year-on-year, and acquisition operation volume was 12,794 square kilometers, a decline of 40.3%. In contrast, bottom operation volume rose sharply to 2,079 square kilometers, up 131.3%, underscoring a clear shift toward higher-value ocean bottom node and cable operations. Looking ahead, with the introduction of new equipment, the application of advanced technologies, and the broader rollout of integrated projects, COSL is well-positioned to capture additional service opportunities. (I do not hold the above stock.)

Strategy¡G

Buy-in Price: $7.40, Target Price: $8.10, Cut Loss Price: $7.00

|

GANFENGLITHIUM(1772)

Analysis¡G

Recently, the proposal for the "15th Five-Year Plan" explicitly called for vigorous development of new energy storage and accelerating the improvement of markets and pricing mechanisms adapted to the new energy system. The plan specifically highlighted the need to promote coal power upgrades, develop pumped storage and new energy storage, and accelerate the construction of smart grids. This not only supports photovoltaic installations but also systematically addresses the issue of new energy integration, directly benefiting supporting industries such as energy storage and grid equipment closely related to photovoltaics. In terms of news, Ganfeng Lithium Group reported revenue of 14.625 billion yuan (RMB, same below) for the first three quarters of 2025, a year-on-year increase of 5.02%. Net profit attributable to shareholders of the listed company was 25.52 million yuan, compared to a loss of 640 million yuan in the same period last year. Basic earnings per share were 0.01 yuan. The company stated that the decline in revenue in the third quarter was mainly due to a decrease in both the sales volume and average selling price of lithium products compared to the same period last year. The growth in net profit was primarily attributed to the fact that, despite the impact of market fluctuations in lithium products leading to a decline in selling prices, the shortened pricing cycle for lithium ore at its subsidiary Windfield Holdings Pty Ltd significantly mitigated the previously existing timing mismatch between the pricing mechanism for chemical-grade lithium concentrate at its wholly-owned subsidiary Talison Lithium Pty Ltd and the sales pricing mechanism for the company's lithium chemical products.

Strategy¡G

Buy-in Price: $54.20, Target Price: $59.50, Cut Loss Price: $49.00

|

|

Feilong Auto (002536 CH) - Short-term fluctuations do not alter long-term trends

Investment SummaryStable Q3 Results with Continued Improvement in Gross Margin

According to the recently released Q3 2025 report, the Company recorded revenue of RMB32.37 million (RMB, the same below) for the first three quarters, down 7.38% yoy. Net profit attributable to the parent company reached RMB287 million, up 7.54% yoy, and net profit attributable to the parent company excluding non-recurring items was RMB304 million, up 16.66% yoy.

Operating costs for the first three quarters dropped 12.78% yoy to RMB24.03 million, a steeper decline than the drop in revenue, mainly driven by optimisation of product mix and cost control. This contributed to a 4.6 ppts increase in gross margin to 25.8%. The overall period expense ratio rose by 2.06 ppts to 14.94%, with the selling expense ratio up 0.64 ppts yoy and the administration expenses ratio up 1.11 ppts yoy. Financial expenses decreased by 31.2% yoy, benefiting from increased exchange gains. The R&D expense ratio rose slightly by 0.55 ppts to 6.7%. Asset impairment losses narrowed by 38.1% yoy, mainly due to a reduction in provision for inventory write-down. Profit growth was primarily driven by continued cost optimisation, partly offset by the rise in period expense ratio. Net profit margin attributable to the parent company increased by 1.23 ppts yoy to 8.86%.

Looking at the quarterly data, Q3 revenue was RMB10.76 million, down 4.68% yoy. Net profit attributable to the parent company was RMB76,301.6 thousand, down 7.9% yoy. Net profit attributable to the parent company excluding non-recurring items was RMB86 million, up 0.38% yoy. Compared to Q2, revenue/net profit attributable to the parent company/net profit attributable to the parent company excluding non-recurring items were up 2.28%, down 13.09%, down 9.34% qoq, respectively. Profitability continued to improve in Q3, with gross margin up 0.84 ppts yoy to 26.28%. The period expense ratio rose slightly by 0.45 ppts yoy, and operating profit margin increased by 1 ppt yoy to 8.9%. However, a sharp increase in non-operating expenses due to losses on disposal of fixed assets, along with a higher effective tax rate, significantly impacted profitability, resulting in a 0.25 ppts yoy decline in net profit margin attributable to the parent company to 7.09%. Overseas Business and Capacity AdjustmentIn terms of market layout, the Company continues to deepen its presence in the domestic market while enhancing its share in international markets through optimisation of overseas channels. The increase in exchange gains indirectly reflects the scale of overseas business settlements. Notably, construction in progress at the end of the reporting period decreased by 50.21% compared with the beginning of the period, mainly due to the transfer of Longtai Auto Parts's project to fixed assets, suggesting that capacity restructuring may provide support for future market expansion. Breakthrough in Liquid Cooling Technology and Entry into the Humanoid Robot Supply ChainDuring the period, the Company achieved significant technological breakthroughs. Its liquid cooling pipeline system gained strong market recognition driven by surging AI computing power demand, further reinforcing its leading technological advantage. The Company successfully introduced its joint module into the supply chain of humanoid robots, marking a substantive advancement in the application of thermal management technology in frontier industries. In addition, the Company continues to promote the integration of its thermal management technology with emerging fields such as robotics, accelerating its deployment in the humanoid robot market and striving to establish a long-term growth engine aimed at fostering new productive forces. Investment ThesisWith the rising penetration of new energy vehicles and increasing demand for liquid-cooled servers, the Company's dual-track strategy of "automotive + general industrial" is expected to continue unlocking result potential. The increase in expense ratio during the market development phase, does not undermine its long-term growth potential.

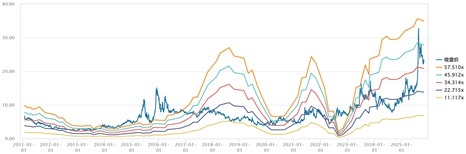

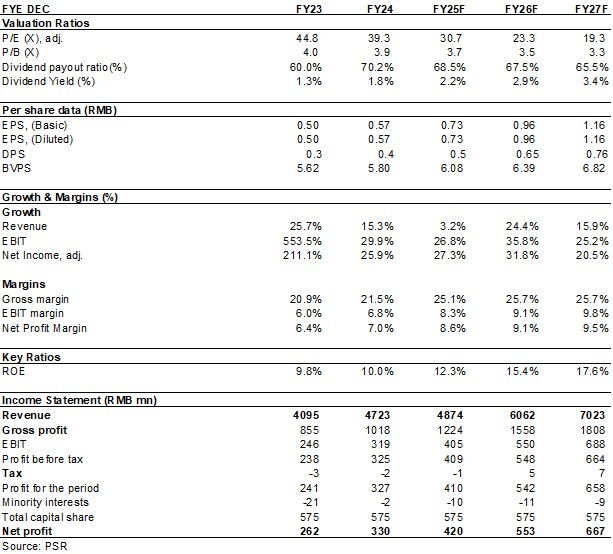

As for valuation, we revised diluted EPS of the Company to RMB 0.73/0.96/1.16 of 2025/2026/2027. And we accordingly gave the target price to RMB23.2, respectively 31.8/24.1/20x P/E for 2025/2026/2027. "Neutral" rating. (Closing price as at 30 October) Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research Risk1) Progress of new production line is below expectations;

2) Electric vehicle sales fall short of expectations;

3) Macroeconomic downturn affects product demand;

4) Sharply rising raw material prices or sharply falling product prices. Financials

(Closing price as at 30 October 2025) Click here to download PDF version...

| Recommendation on 31-10-2025 | | Recommendation | Neutral (Downgrade) | | Price on Recommendation Date | $ 22.400 | | Suggested purchase price | N/A | | Target Price | $ 23.200 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|