|

CIRC(1763)

Analysis¡G

China Isotope & Radiation Corporation (CIRC) focuses its business on two major sectors: nuclear medicine and health, and irradiation applications. The company is dedicated to providing comprehensive nuclear medicine solutions, radiotherapy solutions, and promoting radiation technology applications. The group has established a ¡§6+N¡¨ industrial layout centered on six core businesses: radionuclides, radiopharmaceuticals, nuclear medical equipment, integrated nuclear medicine solutions, radiation sources and applications, and irradiation applications. It is China¡¦s leading enterprise in nuclear technology applications, integrating R&D, production, sales, and services, and is also the global high-tech company with the most comprehensive product portfolio and the most complete industrial chain in the fields of isotopes, their products, and radiation processing.China Isotope & Radiation is the largest domestic manufacturer of radiopharmaceuticals for imaging diagnosis and treatment, as well as urea breath test kits and testing instruments. It is also the only company in China that provides full-process services covering the entire lifecycle of irradiation facilities¡Xfrom site selection, design, and construction to source supply and decommissioning. The group has partnered with Accuray Incorporated, one of the world¡¦s top three radiotherapy equipment suppliers, to enter the high-end radiotherapy equipment sector, focusing on the introduction, digestion, absorption, and re-innovation of advanced systems such as Tomo Therapy and radiosurgery robotic systems. Through independent innovation, the company has successfully developed a fully localized intelligent cobalt-60 gamma-ray Stereotactic Radiotherapy System (Gamma Knife).In terms of technological innovation, Chengdu Gaotong Isotope Co., Ltd., a subsidiary of CIRC, recently officially launched a new isotope separation technology based on fourth-generation ¡§MOF¡¨ materials¡Xthe ¡§Adsorption Trapper¡¨. This breakthrough injects new momentum into high-end nuclear medicine and controlled nuclear fusion, opening up new prospects for industrialization. The ¡§Adsorption Trapper¡¨ technology innovatively incorporates MOF materials¡Xthe focus of the 2025 Nobel Prize in Chemistry¡Xbreaking through the inherent limitations of traditional isotope separation methods and enabling ¡§customized design¡¨ of separation materials at the molecular scale. The technology demonstrates significant advantages in high purity, high efficiency, low cost, and low energy consumption, with broad applications across key national economic sectors, including nuclear medicine, nuclear fusion, heavy water reactors, and biomedical research. It will provide core technological support for China to build an independent, controllable, safe, and stable isotope supply chain, helping to reduce reliance on imports of certain high-end isotopes.The group has also successfully expanded internationally. Recently, it signed a Memorandum of Understanding on Cooperation in Isotope Procurement with Brazil¡¦s Brazil National Commission for Nuclear Energy (CNEN). The two parties will establish a long-term cooperation mechanism centered on isotope product supply, quality management, and information exchange to jointly enhance R&D and application capabilities for isotope products, supporting the development of Brazil¡¦s nuclear technology applications and radiopharmaceutical industry. As a backbone enterprise in China¡¦s isotope and radiopharmaceutical sector, China Isotope & Radiation will use this agreement as an opportunity to actively expand its international cooperation footprint and promote the global outreach of its technology, products, and services.(I do not hold the above stock)

Strategy¡G

Buy-in Price: $17.60, Target Price: $19.00, Cut Loss Price: $16.60

|

WUXI APPTEC(2359)

Analysis¡G

On October 26, WuXi AppTec released its financial report for the third quarter of 2025. The data shows that the company's Q3 revenue reached RMB 12.057 billion, a year-on-year increase of 15.26%. In terms of profit, net profit attributable to shareholders of the listed company was RMB 3.515 billion, surging 53.27% year-on-year. Net profit after deducting non-recurring gains and losses attributable to shareholders was RMB 3.940 billion, up 73.75% compared to the same period last year. The chemistry business remained the main growth driver, with revenue for the first three quarters increasing by 29.3% year-on-year. Among these, the TIDES business (oligonucleotides and peptides) performed exceptionally well, with revenue skyrocketing 121.1% year-on-year to RMB 7.84 billion. The small-molecule CDMO business also demonstrated steady growth. As of the end of September 2025, WuXi AppTec's orders for continuing operations amounted to RMB 59.88 billion, a significant year-on-year increase of 41.2%. This data provides a solid foundation for the company to raise its full-year performance guidance.

Strategy¡G

Buy-in Price: $115.00, Target Price: $126.50, Cut Loss Price: $104.00

|

|

Fuyao Glass (3606.HK) - High-End Products Continue to Expand

Investment SummaryNearly 30% Increase in Profit for the First Three Quarters, High-End Products Continue to Expand Proportion

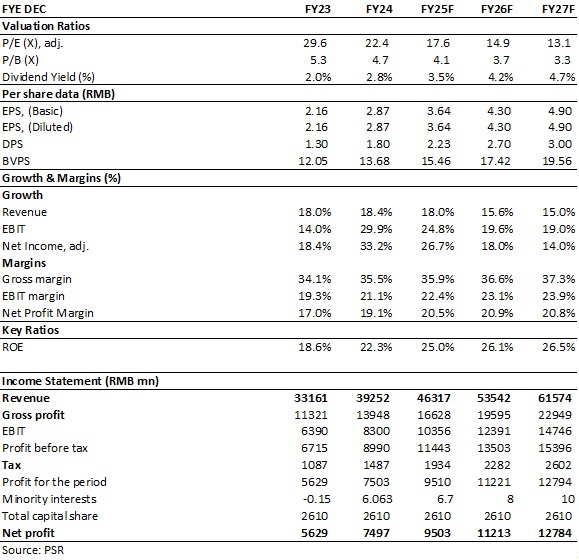

In the first three quarters of 2025, Fuyao Glass reported a revenue of RMB33.302 billion (RMB, the same below), a year-on-year (YoY) increase of 17.62%. Net profit attributable to the parent company reached RMB7.064 billion, up 28.93% YoY, setting a new historical high. In the third quarter alone, revenue amounted to RMB11.855 billion, a YoY increase of 18.86%, while net profit attributable to the parent company reached RMB2.259 billion, up 14.09% YoY.

Since the beginning of the year, the automotive market has continued to recover. In the first three quarters of 2025, the Chinese automotive market sold 24,363 thousand vehicles, a YoY increase of 12.9%. The new car sales of light vehicles in the United States increased slightly by 4.4%. The company's revenue growth continues to outperform the industry, mainly benefiting from the increased penetration of high-value-added products and further market share expansion.

During this period, innovative products such as intelligent sunroof glass, adjustable light glass, and HUD-integrated glass continued to ramp up, driving the steady increase in per vehicle glass value. In the first three quarters, the Company's average selling price (ASP) of automotive glass per square meter rose by approximately 6.9% YoY. The share of high-value-added products also increased by 4.9 percentage points. With the continuous advancement of automotive intelligence, autonomous driving levels, and the application and development of various new technologies and scenarios, as well as an increase in user experience-driven consumption, the trend towards high-end automotive glass is expected to continue. There is still room for further improvement in the proportion of high-value-added products in the Company's product mix.

Gross margin recorded a YoY increase of 0.99 percentage points. The net profit margin attributable to the parent company was 21.2%, a YoY increase of 1.86 percentage points. The main drivers of the performance were the operating leverage effect from improved capacity utilization, a YoY decrease in expense ratios, increased foreign exchange gains, and a narrowing of investment losses. In the first three quarters, the company's selling expense ratio was 2.84%, down 1.36 percentage points YoY; the administration expense ratio was 7.29%, down 0.07 percentage points YoY; and R&D expenditure amounted to RMB1.39 billion, accounting for 4.18% of revenue, a YoY decrease of 0.11 percentage points.

The company's cash flow remains strong, with net operating cash inflows reaching RMB9.88 billion in the first three quarters, a YoY increase of 57.3%. In the third quarter alone, net cash inflow amounted to RMB4.53 billion, setting a new historical high. Gradual Release of New Production CapacityThe Company is accelerating the release of production capacity at its production bases in Fuqing, Hefei, and Illinois, USA. Domestically, the smart manufacturing bases in Fuqing and Anhui are under rapid construction, with production expected to begin before the end of 2025. The new capacity will support the further expansion of global market share. In terms of overseas business, Fuyao's U.S. subsidiary achieved a net profit of RMB433 million in the first half of 2025, up 11.8% YoY. As local production capacity utilization gradually increases, the advantages of the localized production, sales, and R&D system will become more evident. It is expected that the net profit margin in the North American market will stabilize above 11.2%, with a target of reaching 15%. Chairman's Early Transition to Ensure Governance Upgrade and Strategic ContinuityTo drive strategic optimization of the Company's governance structure and sustainable development, Mr. Cao Dewang resigned from his position as Chairman, and the Board of Directors elected Vice Chairman Mr. Cao Hui as the new Chairman. We believe that this early transition (originally scheduled for January 2027) signals the management's proactive layout for the Fuyao's sustainable development. By clearly defining the succession system, the company has completed its governance upgrade. At the same time, Mr. Cao Dewang will remain on the Board as Honorary Chairman, ensuring the continuity of the Fuyao's strategy and minimizing the impact of the core leadership change. Investment ThesisWith the global trend of automotive electrification and intelligentization, Fuyao Glass's growth momentum is clearly visible. In the medium to long term, we expect the proportion of high-value-added products in automotive glass to continue to increase. The Company is also continuously expanding its product boundaries, opening up space for long-term sustainable growth.

In addition, the subsequent loss reduction of SAM and the improvement in the efficiency of the US factory are expected to bring more potential profit flexibility. As a global leader in the automotive glass industry, the Company is expected to continue benefiting from its competitive advantages and maintain a high dividend payout ratio.

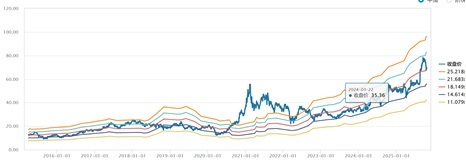

We forecast its EPS to be RMB 3.64/4.30/4.90 in 2025/2026/2027. We give the "Accumulate" rating, with a revised target price to be HK$79.8, equivalent to 20/17/14.9x P/E for 2025/2026/2027. P/E Band

Source: Wind, Phillip Securities (HK) Research Risk1) Demand for automobiles keeps sluggish;

2) Cost of raw materials increases;

3) RMB appreciates. Catalyst

Success market development of overseas automobile market; rebound of domestic demand for automobile; depreciation of RMB Financials

(Closing price as at 24 October 2025) Click here to download PDF version...

| Recommendation on 28-10-2025 | | Recommendation | Accumulate (Maintain) | | Price on Recommendation Date | $ 70.050 | | Suggested purchase price | N/A | | Target Price | $ 79.800 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|