|

CHINA UNICOM(762)

Analysis¡G

China Mobile (941), China Telecom (728), and China Unicom (762) have successively released their third-quarter results for this year. In terms of revenue scale and growth, China Mobile leads by a wide margin (approximately equal to the sum of the other two), with Q3 operating revenue of RMB 794.7 billion, up 0.4% year-on-year. Of this, communication service revenue was RMB 683.1 billion, up 0.8%. China Telecom¡¦s Q3 revenue was RMB 396.9 billion, up 0.6%. China Unicom¡¦s Q3 operating revenue was RMB 293.0 billion, up 1%. Of this, service revenue was RMB 261.6 billion, up 1.1%, marking the highest growth rate among the three operators.

In terms of new businesses, Unicom recorded Q3 cloud revenue of RMB 15.3 billion, up 26%; total revenue for the first three quarters reached RMB 52.9 billion, with computing power business scale breaking through. Data center revenue was RMB 21.4 billion, up 8.9%, reflecting significant results from intelligent data center upgrades. China Mobile stated that DICT business revenue maintained good growth in the first three quarters, with AI direct revenue achieving high-speed growth, though no specific figures were provided. China Telecom provided more data on emerging strategic businesses: IDC revenue for the first three quarters reached RMB 27.5 billion, up 9.1%; security revenue reached RMB 12.6 billion, up 12.4%; smart revenue grew 62.3%, visual networking revenue grew 34.2%, satellite communication revenue grew 23.5%, and quantum revenue grew 134.6%.

On the profit front, China Unicom also took the lead, with shareholders¡¦ attributable profit for the first three quarters at RMB 20.0 billion, up 5., mainly benefiting from optimized cost control. China Telecom¡¦s shareholders¡¦ attributable profit increased 5% to RMB 30.7 billion. China Mobile¡¦s shareholders¡¦ attributable profit was RMB 115.4 billion, up 4%. In terms of capital expenditure, the three companies¡¦ total plan for 2025 is nearly RMB 300 billion, focusing on AI and computing power. China Mobile: RMB 151.2 billion, down 7.8% year-on-year; China Telecom: RMB 83.6 billion; Unicom is moderately ahead in cloud and digital intelligence investments.

From an investment perspective, all three companies are high-dividend defensive stocks with annualized dividend yields of about 5-7%. However, the third-quarter results show that under slowing growth, new businesses (such as AI, cloud, and 5G private networks) have become key differentiating factors. China Mobile has strong scale advantages and ample cash flow (free cash flow exceeding RMB 100 billion), but lacks growth momentum. China Telecom is actively transforming, with rising contributions from emerging strategic businesses, but revenue declines are dragging down its share price. Unicom leads in profit growth, with explosive momentum in cloud business, and plans to spin off and list its Zhiwang Technology on the ChiNext board of the Shenzhen Stock Exchange, sparking market expectations of value unlocking.(I personally do not hold the above stocks).

Strategy¡G

Buy-in Price: $9.26, Target Price: $10.20 , Cut Loss Price: $8.86

|

CONANT OPTICAL(2276)

Analysis¡G

CONANT OPTICAL is a leading resin eyeglass lens manufacturer in China, with products sold in over 80 countries. The company offers a wide range of resin eyeglass lenses, including standardized and customized solutions. It has established an extensive network of reliable customers worldwide, including several renowned eyeglass lens brand owners and international ophthalmic optics companies. The company's XR business has achieved substantial progress, with collaborations smoothly advancing with multiple globally leading technology enterprises. As of August 31, 2025, cumulative revenue from the XR business reached approximately RMB 10 million. With several key projects entering or expanding mass production, the company expects XR business revenue to further grow in the second half of 2025 and into 2026. In the first half of 2025, the company reported revenue of RMB 1.084 billion, a year-on-year increase of 11.1%, primarily driven by sales growth across various channels, continuous upgrades in products and services, and optimized product mix. Net profit attributable to shareholders was RMB 273 million, up 30.7% year-on-year. EPS stood at RMB 0.59, representing an 18% year-on-year increase. CONANT OPTICAL has achieved steady growth through product structure optimization and global expansion in its traditional business. At the same time, its forward-looking strategic focus on the smart glasses (XR) business is expected to contribute significantly to future profitability.

Strategy¡G

Buy-in Price: $41.94, Target Price: $47.36 , Cut Loss Price: $39.00

|

|

Minth Group (425.HK) - Battery Box Becomes the Largest Business Segment

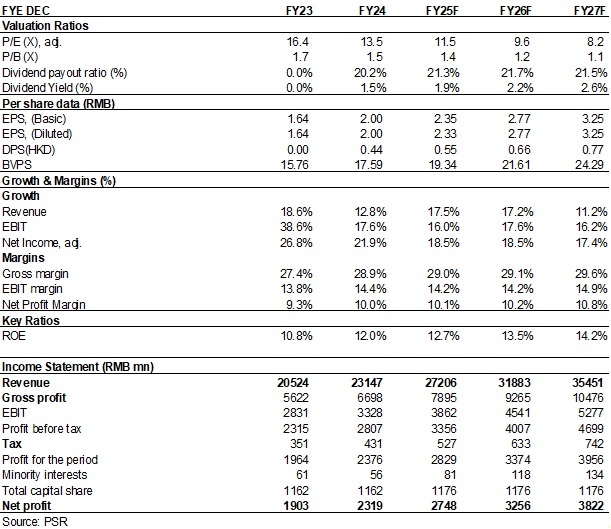

Company ProfileMinth Group is a world-renowned supplier engaged in the design, manufacturing and sales of automotive interior and exterior trim and body structure parts. The domestic market share of its core products exceeds 30%. The company has production bases in China, the United States, Mexico, Thailand, Germany, Serbia and other countries, and its customers cover major vehicle companies in the market. Based on a variety of new materials and surface treatment technologies, in recent years the company has developed new electrified and smart product lines such as aluminum power battery boxes and smart front faces, forming a series of competitive terminal products. Investment SummaryStrong Profit Growth Maintained in H1 2025, Net Profit Up Nearly 20%

Minth Group recorded revenue of RMB12.287 billion (RMB, the same below) in H1 2025, up 10.8% yoy; net profit attributable to the parent company reached RMB1.277 billion, equivalent to an increase of 19.5% yoy. The main drivers behind the profit growth include: 1) continued ramp-up of orders for NEV components such as battery boxes, leading to higher capacity utilisation; 2) incremental earnings contribution from capacity ramp-up at overseas production bases; 3) decline in unit transportation costs and favourable exchange rates. Meanwhile, the Company continued to advance its localisation strategy and implement effective cost control measures, resulting in lower expense ratios.

By region, domestic revenue was RMB4.31 billion, down 4.9% yoy, mainly due to the decline in market share of joint venture brands in China. International business remained strong, with revenue up 21.6% yoy to RMB7.98 billion, primarily driven by rapid growth in battery box and structural component businesses in the European market, as well as stable contributions from traditional exterior parts in international markets. The proportion of international business in total revenue rose by 5.2 ppts from 59.7% at the end of 2024 to 64.9%. The localisation strategy in North America, Europe and other regions has effectively reduced tariffs and geopolitical risks, while enhancing competitiveness in local markets. Battery Box Becomes the Largest Business Segment

In H1, the Company's revenue from plastic parts, metal and trims, battery boxes, and aluminium parts reached RMB2.87/2.66/3.58/2.47 billion respectively, up 0.9%/4.7%/49.8%/4.1% yoy. Their respective shares of total revenue changed by -2.3/-1.3/+7.6/-1.3 ppts yoy, to 23.3%/21.6%/29.2%/20.1%.

During the review period, the Company achieved breakthroughs in its battery box and body chassis structure businesses, with a more balanced customer mix: it broke into the structural component business for Toyota Europe, and secured chassis structure orders from multiple Chinese clients such as Great Wall and Geely; entered the battery box business of Chery for the first time and secured repeat orders from BYD; made its first breakthrough in battery box structural parts for General Motors; and continued to expand its battery box business with Stellantis and Volkswagen. In the area of smart interior and exterior parts, the Company achieved breakthroughs in bumper assembly business with Ford North America and Renault, while continuing to secure orders from clients such as Toyota, Hyundai-Kia, Changan, and General Motors. Profitability Continued to Improve SteadilyDuring the period, gross margin was approximately 28.3%, down 0.2 ppts yoy, mainly due to the rising contribution from the battery box business. The gross margins of the four major business segments were 26.1%, 28.1%, 23.0%, 32.6%, representing yoy changes of +2.0, +1.6, +2.4, -2.4 ppts, respectively. Among them, the battery box segment achieved a gross margin of 23%, moving closer to the 25% target. During the period, selling, administration and R&D expense ratios declined by 0.6, 0.1, and 0.5 ppts yoy respectively, lifting net profit margin by 0.8 ppts to 10.4%, indicating an improvement in the Company's profitability.

Operating cash flow rose by RMB 510 million yoy to RMB2.24 billion in H1 2025, reflecting sound cash flow conditions, which provide a solid basis for dividend payments and share buybacks. Capital expenditure stood at RMB902 million, down 17.5% yoy, as the Company has passed its peak investment phase and will focus on equipment upgrades and flexible transformation going forward. In H2, as several new overseas production lines continue to ramp up, overall gross margin is expected to see a slight improvement mom. New Businesses and Emerging Segments Gearing UpThe Company is actively exploring new business segments and has made forward-looking deployments in areas such as eVTOL (electric vertical take-off and landing aircraft), wireless charging for electric vehicles, and bionic robots---including core components such as electronic skin, smart masks, integrated joints, bodies, and rotors. During the period, the Company partnered with leading enterprises including EHang and Zhiyuan Robotics. Some products have completed small-batch sample deliveries to multiple customers, and some have already secured mass production orders, with revenue contribution expected to begin in 2026/2027. With the rapid development of robotaxis and autonomous driving, the wireless charging industry is projected to experience explosive growth in 2026. At the same time, leveraging its battery box technology, the Company is also focusing on the development and implementation of AI liquid-cooling system-related products, aiming to capture opportunities in the rapidly growing artificial intelligence market. ValuationThe company maintains stable overall operations, with continuous improvement in profitability, demonstrating strong risk resilience and growth adaptability. Meanwhile, the cultivation of new business areas and the expansion of new ventures are expected to foster a second growth curve, driving the company's sustainable development in the medium to long term.

We slightly revised the expected EPS for 2025/2026/2027 to 2.35/2.77/3.25 (from 2.43/2.89/3.30) yuan for the under expected GM.

We believe that it is reasonable to give the Company a valuation of 12.7/10.6/9.0 x P/E and 1.5/1.4/1.2x P/B for 2025/2026/2027, equivalent to target price of HK$ 32.6 and Accumulate rating. P/E Band

Source: Wind, Phillip Securities Hong Kong Research Financials

(Closing price as at 17 October 2025) Click here to download PDF version...

| Recommendation on 27-10-2025 | | Recommendation | Accumulate (Downgrade) | | Price on Recommendation Date | $ 29.480 | | Suggested purchase price | N/A | | Target Price | $ 32.600 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|