|

TRAD CHI MED(570)

Analysis¡G

China Traditional Chinese Medicine primarily engages in the research, development, production, and sales of traditional Chinese medicine (TCM) and pharmaceutical products. Its operations span five major segments: Chinese medicinal herbs integration business, TCM decoction pieces, concentrated TCM granules,TCM finished goods, and TCM great health.

In the Chinese medicinal herbs integration business, the group continues to expand the construction of Good Agricultural Practice (GAP) bases to meet development needs. As of June 30, 2025, it has participated in establishing 162 TCM raw material production bases across 22 provinces (regions and cities), covering 109 TCM varieties and spanning over 459,000 mu (approximately 30,600 hectares). Of these, 95 varieties are integrated into the TCM quality traceability system. Additionally, 24 seed and seedling breeding bases have been established, covering 2,347.5 mu and involving 22 key TCM varieties. Leveraging its TCM full-industry-chain quality technology service platform, the group has built a closed-loop quality traceability system encompassing ¡§seeds and seedlings ¡V TCM raw material production ¡V industrial processing ¡V sales,¡¨ centered on the ¡§¡§Chinese medicinal herbs production quality traceability system¡¨ and the ¡§TCM Industrial Production Quality Traceability System.¡¨

In the TCM decoction pieces segment, the group is actively deepening its regional presence, strengthening cooperation with existing clients, and expanding into the medical terminal market, adding over 400 new medical terminal clients. It has also solidified its competitive edge in specialized TCM decoction piece operations, achieving regional leadership in Beijing, Shanghai, Guangdong, Shandong, and Guizhou, while accelerating regional integration and collaborative development. The group¡¦s shared TCM intelligent distribution center has driven significant growth in decoction piece sales, particularly in the medical terminal market, resulting in substantial revenue increases. Concurrently, the group has adjusted its sales strategy, focusing on toxic decoction pieces and protected-wildlife-based decoction pieces to explore new varieties and clients, continuously enhancing market expansion and product structure optimization.

In the Concentrated TCM granules segment, the group is intensifying academic research and clinical applications by analyzing pharmaceutical properties, accumulating evidence of efficacy advantages, and promoting substitution solutions to build an evidence chain, thereby increasing doctors¡¦ recognition and acceptance of concentrated TCM granules. It is also steadily advancing the development of comprehensive hospitals, improving terminal coverage, and enhancing client retention. In the TCM finished drugs segment, for prescription drugs, the group focuses on increasing direct sales to terminals and deepening market penetration. For over-the-counter (OTC) drugs, it has expanded its online presence, completing system integrations with multiple core e-commerce platforms. Additionally, it continues to refine its nationwide chain client network, concentrating resources to strengthen partnerships with key chains. In the TCM great health segment, on the product side, the group focuses on distinctive varieties, premium decoction pieces, and medicine-food homology varieties, while expanding and integrating marketing channel resources. In its TCM medical institutions, it provides comprehensive and diverse TCM health services centered on TCM products and technologies. (I do not hold the aforementioned stock)

Strategy¡G

Buy-in Price: $2.52, Target Price: $2.75, Cut Loss Price: $2.40

|

ANHUIEXPRESSWAY(995.HK/600012.CH)

Analysis¡G

The Company is the only listed expressway company in Anhui Province. At present, it has the toll rights and interests of 9 high-speed expressways/first-class highway/bridges. The mileage of roads in operation is 5126 km. Most of them are national east-west channels, and play an important role in highway transportation in Anhui Province and the whole country. The core roads of the Company, including the Sanhe Nanjing Expressway, Xuanguang Expressway, and Gaojie Expressway, are gradually being renovated and expanded, and the operating period is expected to be extended by 25-30 years. In 2025H1, the company's revenue was RMB 3.74 billion, a yoy increase of 11.7%, and the net profit attributable to the parent company was RMB 0.96 billion, a yoy increase of 4.0%. The Company plans to acquire Fuzhou Expressway and Sixu Expressway in the near future. In the first quarter of 2025, the company completed the acquisition of Fuzhou Expressway and Sixu Expressway. Meanwhile, the reconstruction and expansion of Xuan Guang Expressway was completed, combined with the adjustment of truck toll rates in Anhui Province, driving a 13.4% growth in toll revenue. The company's performance is expected to continue benefiting from the acquisition of road assets and the advancement of core asset expansions in the coming years. In April 2025, the company introduced a new round of shareholder return plan, pledging that the cash dividend ratio for 2025-2027 will not be less than 60% of the net profit attributable to the parent company, sustaining high dividend expectations.

Strategy¡G

Buy-in Price: $12.26, Target Price: $14.10, Cut Loss Price: $11.20

Buy-in Price: RMB14.33, Target Price: RMB16.50, Cut Loss Price: RMB13.16

|

|

SMIC (00981.HK) - Capacity expansion slows, while product mix begins to improve

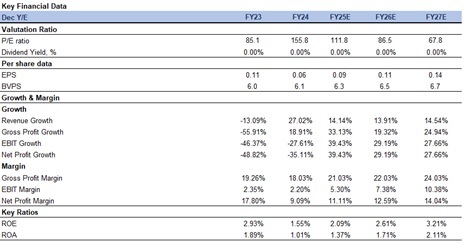

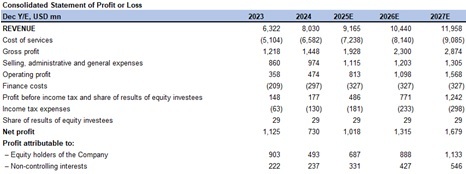

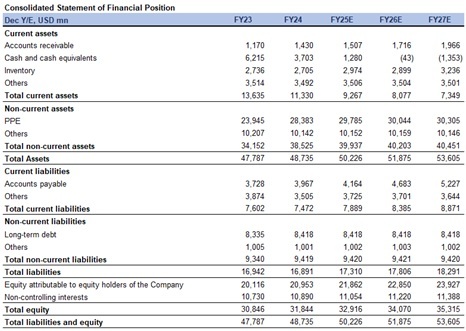

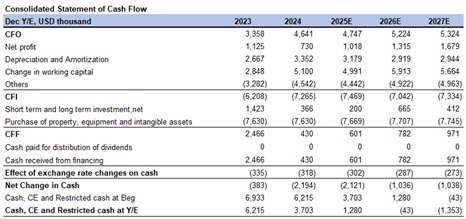

Financial performanceIn the first half of 2025, the company achieved revenue of $4.5 billion (USD, same below), a year-on-year increase of 22.0%. The gross profit margin was 21.4%, up 7.6 percentage points year-on-year. Profit before tax was $510 million, a year-on-year increase of 95.0%. Net profit attributable to the parent company was $320 million, a year-on-year increase of 35.6%. In the second quarter of 2025, the company achieved revenue of $2.2 billion, a quarter-on-quarter decrease of 1.7%. This was primarily due to a 6.4% quarter-on-quarter decrease in ASP, while the number of wafers sold increased by 4.3% quarter-on-quarter to 2.39 million 8-inch equivalent wafers, mainly driven by inventory replenishment. By application segment, management stated that the revenue contributions from smartphones, computers & tablets, consumer electronics, connectivity & wearables, and industrial & automotive were 25%, 15%, 41%, 8%, and 11%, respectively. The company's automotive electronics product shipments continued steady growth, with primary revenue contributions coming from automotive-grade chips such as analog/power management, image sensors, logic-embedded memory, and controllers. The overall automotive segment grew 20% quarter-on-quarter in Q2. The revenue contribution from 8-inch and 12-inch wafers was 24% and 76%, respectively. The absolute revenue from 8-inch wafers increased by 7% quarter-on-quarter, with capacity utilization outperforming peers. The company's gross profit margin for Q2 was 20.4%, down 2.1 percentage points quarter-on-quarter, mainly due to decreased ASP caused by production volatility and product mix changes. Capacity utilization was 92.5%, up 2.9 percentage points quarter-on-quarter, with utilization rates for both 8-inch and 12-inch wafers improving further. As of the end of Q2, the company's monthly capacity reached 991,000 8-inch equivalent wafers. Profit before tax was $160 million, a quarter-on-quarter decrease of 54.1%. Net profit attributable to the parent company was $130 million, a quarter-on-quarter decrease of 29.5%. The company guides for Q3 2025 revenue to increase by 5%-7% quarter-on-quarter, expecting both shipment volume and ASP to rise, reflecting an improving product mix alongside capacity expansion. The gross margin is guided between 18% and 20%, flat with the Q2 guidance, mainly due to increased depreciation from new capacity, though the improved product mix enhances profitability. Affected by the industry's traditional slow season, inventory was built up in the first three quarters to support customer demand pull-ins. Although customer confidence remains strong, the pace of urgent orders and demand pull-ins is expected to slow somewhat in Q4. Management indicated that as the company overall remains in a state of tight supply, the slowdown in shipment pace will not significantly impact capacity utilization. Based on the above, and assuming no major changes in the external environment, the company's full-year target remains to exceed the average of comparable peers. Investment thesisBased on SMIC's recent slower capacity expansion pace and management's more conservative outlook for 2H25E and 3Q25E revenue, we adjust the company's 2025-2027 revenue forecasts to $9.2 billion / $10.4 billion / $12.0 billion, respectively. We forecast net profit attributable to the parent company to be $687 million / $888 million / $1.133 billion for 2025/2026/2027, corresponding to EPS of $0.09 / $0.11 / $0.14. Overall, as a leading player in the foundry segment, we believe the company's reasonable valuation is slightly above one standard deviation of its historical average NTM P/B ratio, at 1.8x 2025 forecasted P/B. This corresponds to a target price of HKD 87 per share. We adjust our rating to 'Accumulate'. Risk factors1) Tightening of U.S. export controls;

2) Lower-than-expected ramp-up of capacity at the Wuxi wafer fab;

3) Weaker-than-expected increase in ASP. Financials

(Current Price as of: 16 Oct 2025)

Source¡G PSHK Est. Download PDF version...

| Recommendation on 20-10-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 73.900 | | Suggested purchase price | N/A | | Target Price | $ 87.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|