|

CLOUD FACTORY(2512)

Analysis¡G

Cloud Factory primarily provides Internet Data Center (IDC) solutions, edge computing services, and other services, having been recognized as one of China¡¦s top 20 edge computing companies for three consecutive years. In the first half of 2025, the group expanded its focus from building edge computing infrastructure to developing scenario-based edge computing applications and deep integration with various industries. Aligning with the industry trend of integrating edge computing with AI, the group strengthened its core strategy of ¡§Edge Cloud + AI Services¡¨ and deployed nodes nationwide, creating a ¡§10-kilometer low-latency computing service circle¡¨ that covers over 2,000 counties in China, supporting localized computing power and achieving computing-network integration. Leveraging its computing power scheduling platform, model fine-tuning platform, and AI large-scale model applications, the group is building a comprehensive technology stack, covering diverse model capabilities at the Model-as-a-Service (MaaS) layer and deep industry scenario integration at the Software-as-a-Service (SaaS) layer. Its strategic focus is to anchor itself in the computing power network while deeply engaging in intelligent scenarios, providing real-time, fast-response edge AI solutions for sectors such as government, transportation, and education, and transitioning toward an ¡§edge intelligence foundation¡¨ to empower intelligent upgrades across industries.

In the first half of 2025, the group successfully launched several new services. The EdgeAIStation service completed adaptations for multiple mainstream AI models on its computing platform. With stable infrastructure and a global node network, the group can now provide reliable and secure computing services to meet market demands. Additionally, it launched the Lingjing Cloud Large Model Private Deployment Solution, offering various AI models, application platforms, and private deployment solutions for computing clusters, enabling enterprise clients to build proprietary knowledge bases, utilize model fine-tuning services, and benefit from secure, flexible, and efficient AI solutions integrated into the group¡¦s products. Furthermore, the group officially launched a computing power scheduling solution, a one-stop platform managing diverse computing resources, including GPUs, NPUs, and FPGAs, with features like mirroring and snapshots to simplify client operations. The group¡¦s efforts have earned recognition from clients and prominent institutions, with collaborations in the first half of 2025 with the Robotics Industry Alliance, renowned universities, and leading enterprises, providing support for edge computing, AI large model development, and computing-related services.

Looking ahead, the group will prioritize several key areas:

1. New business expansion: Intelligent computing services, including hardware consulting, server deployment, network enhancement, intelligent computing platform construction, equipment procurement and installation, technical support and maintenance, and cloud computing and computing resource leasing services.

2. Technology R&D: Building a full-stack technology system from Infrastructure-as-a-Service (IaaS) to SaaS, supported by self-developed computing power scheduling platforms, model fine-tuning platforms, and AI large model applications, achieving cloud-edge-device collaboration.

3. Ecosystem collaboration: Co-building a comprehensive ecosystem connecting hardware, platforms, and applications.

4. ¡§Government-Enterprise Dual-Driven¡¨ business model: Strengthening partnerships with government and enterprise clients.

(I do not hold any shares in the mentioned stock.)

Strategy¡G

Buy-in Price: $4.80, Target Price: $5.30 Cut Loss Price: $4.55

|

LYGEND RESOURCE(2245)

Analysis¡G

The Company is a nickel full industry chain company, with business covering nickel ore and nickel iron trade, smelting production, equipment manufacturing, and sales. In the field of nickel product trade, according to the Zhuoshi report, the company's nickel ore trade volume ranked fourth globally in 2020 and first in China. Since 2017, the Company has been involved in nickel cobalt smelting plants, including wet smelting and pyrometallurgy. The Company has fully utilized its resource advantages, forward-looking layout of the Indonesian industry, and taken the lead in realizing the production of wet smelting projects, with obvious first mover advantages. Starting from 2021, the production capacity of Indonesia's nickel HPAL project has gradually been implemented, and the performance has entered a period of high-speed growth. In the first half of 2025, the Company recorded a revenue of RMB 18.15 billion, a yoy increase of 66.8%, and a net profit attributable to the parent company of RMB 1.43 billion, a yoy increase of 143.0%. With the steady release of production capacity from the HPAL project, the Company has further deepened its strategic cooperation with mainstream global precursor and cathode material companies, signed multiple long-term agreements, and provided strong support for future performance growth.

Strategy¡G

Buy-in Price: $16.47, Target Price: $19.10 Cut Loss Price: $15.10

|

|

GIANT BIOGENE (2367.HK) - Revenue and Profit Both Grow in H1 2025, Highlighting Long-Term Competitiveness

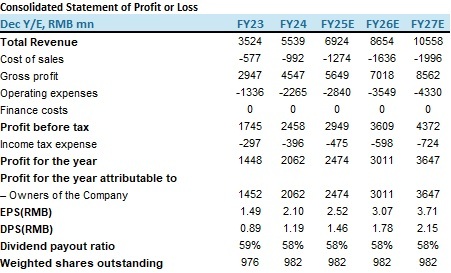

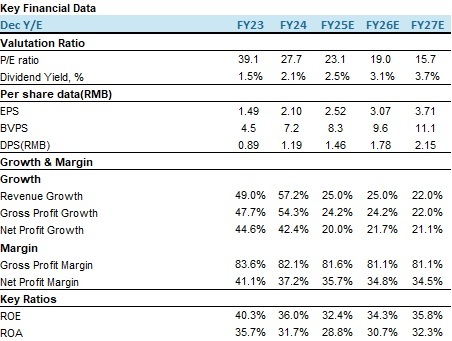

OverviewGIANT BIOGENE (2367.HK), founded in 2000, is a high-tech enterprise rooted in scientific aesthetics and a pioneer and leader in China's professional skincare industry based on bioactive ingredients. Leveraging its proprietary synthetic biology technology platform, the company independently researches, develops, and produces various types of recombinant collagen and rare ginsenosides. It focuses on three major business directions: functional skincare products, medical devices, functional foods, and foods for special medical purposes. Performance reviewIn H1 2025, the company's revenue reached RMB 3.113 billion, representing a year-on-year increase of 22.5%. However, this growth slowed significantly compared to the full-year 2024 growth rate. We believe this was mainly influenced by the following factors: 1)Public opinion incident: In May of this year, the company's flagship brand, Comfy, was involved in a controversy regarding the ingredients of its recombinant collagen essence, which negatively impacted product sales. 2)Natural slowdown in growth of star products: The growth rate of Comfy Collagen Stick naturally decelerated. 3)Underwhelming performance of new products: New products such as Comfy Focus Cream and anti-aging series faced challenges. On one hand, market penetration for new products takes time, and the incremental revenue they generate may not immediately offset the slowdown in star products. On the other hand, the market performance of new products remains uncertain. 4)Erosion of market share due to industry competition: The recombinant collagen segment offers significant profits, attracting numerous players, including traditional skincare giants, emerging brands, and biotechnology companies. Competitors such as Bloomage Biotech and Jinbo Biotech have also intensified their efforts by launching similar products, further exacerbating market competition.The gross profit margin stood at 81.7%, demonstrating strong profitability, though it decreased by 0.7 percentage points year-on-year, primarily due to changes in the product mix. Selling expenses amounted to RMB 1.059 billion with a year-on-year increase of 18.7%, mainly driven by increased investment in brand building, including brand promotion, marketing, and channel expansion to drive business expansion and category development. At the same time, the company continued to optimize operational efficiency to solidify its long-term growth foundation. Over the past five years, the company's selling expense ratio has consistently increased, reaching 36.3% in 2024. We expect the selling expense ratio to remain above 30% over the next three years. The R&D expense ratio was 1.3%, down 0.6 percentage points year-on-year, primarily due to some R&D projects entering the commercialization phase and a reduction in share-based compensation expenses. Compared with peers such as Proya and Marubi Biotech, the company's R&D expense ratio is relatively low. As of the end of the reporting period, the company had over 140 ongoing R&D projects and 186 authorized and pending patents. Net profit attributable to shareholders was RMB 1.182 billion with a year-on-year increase of 20.2%, and EPS was RMB 1.14 with a year-on-year increase of 15.2%. Online Direct Sales More Than Doubled Year-on-Year, with Revenue Share Expected to Continue RisingBy sales channel, the company's direct sales revenue in H1 2025 was RMB 2.325 billion, up 26.5% year-on-year, while sales to distributors reached RMB 787 million, up 12.1% year-on-year. Among these, online direct sales revenue through e-commerce platforms amounted to RMB 391 million, surging 133.6% year-on-year, accounting for 12.6% of total revenue. This growth was mainly driven by JD.com's self-operated channel, which focused on meticulous operations targeting beauty consumers to rapidly expand its beauty category, and leveraged the platform's healthcare ecosystem resources to consolidate its advantage in the health category. Currently, online direct sales account for a relatively small portion of revenue. We believe the share is expected to increase significantly as the company continues to intensify its marketing efforts on e-commerce platforms. Star Products Shined During 618, Product Portfolio Continues to ExpandBy brand, Comfy's revenue in H1 2025 was RMB 2.541 billion, up 22.7% year-on-year, accounting for 81.7% of total revenue. Collgene's revenue was RMB 503 million, up 26.9% year-on-year, accounting for 16.1% of total revenue. Revenue from other brands was RMB 58 million, down 10.5% year-on-year, accounting for 1.9% of total revenue. Revenue from health foods and others was RMB 10 million, up 16.3% year-on-year, accounting for 0.3% of total revenue. During the 618 shopping festival, the star product Comfy Recombinant Collagen Dressing ranked first on Tmall's list of most highly rated medical dressings, while Comfy Collagen Stick 2.0 ranked first among domestic products on Tmall's list of best-selling liquid essences, demonstrating outstanding performance. During the reporting period, the company launched the Comfy Precise and Intensive Repair Series, further enriching its product portfolio. New Exclusive Patent for Recombinant Type IV CollagenIn August, the company's R&D team conducted in-depth research that not only validated the mechanism of recombinant Type IV collagen in maintaining endothelial barrier homeostasis and soothing redness but also firstly discovered that collagen nonapeptide (GAAGLPGPK) had the efficacy of repairing the basement membrane barrier and soothing redness. Moreover, a specific ratio of recombinant Type IV collagen combined with collagen nonapeptide showed significant synergistic effects in repairing the skin barrier and soothing redness. This breakthrough is expected to bring major advancements to the company's product updates. Deepening Expertise in Rare Ginsenosides, with Potential for Industrial Application in Functional FoodsThe company's research team discovered that rare ginsenosides Rg3, Rk1, and Rg5 had efficacy in alleviating cognitive impairment and improving memory, while Rk1 and Rg5 also possess functions related to inhibiting neural excitement and aiding sleep. The implementation of this patent offers innovative solutions for populations with high incidence rates of cognitive impairment (e.g., the elderly) and those experiencing memory decline (e.g., middle-aged and young adults). The patent is easy to industrialize and can be extensively applied in the broad health area, such as functional foods, with wide-ranging prospects. The company's health food revenue may further contribute incremental growth. Valuation and Investment RecommendationAs a leader in China's recombinant collagen sector, GIANT BIOGENE is well-positioned to maintain its leading role in the functional skincare and medical aesthetics markets, thanks to its technological barriers, brand matrix, and channel advantages. In July of this year, Focustar Capital and GIANT BIOGENE established a joint venture focused on developing the Southeast Asian market. In June 2025, Comfy, under GIANT BIOGENE, became the first Chinese functional skincare brand to enter Watsons in Malaysia. We are optimistic about its overseas growth prospects. We believe the collagen skincare market still has significant room for development, and GIANT BIOGENE is poised to continue benefiting from it. Previous short-term impacts have been fully digested by the market, and growth in the second half of the year is highly certain. We forecast the company's revenue for 2025-2027 to be RMB 6.924 billion, RMB 8.654 billion, and RMB 10.558 billion, respectively, with EPS of RMB 2.52, RMB 3.07, and RMB 3.71. The current share price corresponds to a P/E ratio of 23.1x, 19x, and 15.7x for 2025-2027. Based on a target 2026 P/E of 22x, we give the target price to HKD 73.72 and initiate coverage with an "Accumulate" rating. (Current price as of September 22) Risk factors1) The macro-economy is in a downward trend;

2) Industry competition is intensifying;

3) New product promotion is not as good as expected. Financial Data

(Current Price as of: 22 Sep 2025)

Source: PSHK Est. Download PDF Version...

| Recommendation on 24-9-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 63.200 | | Suggested purchase price | N/A | | Target Price | $ 73.720 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|