|

LEADS BIOLABS-B(9887)

Analysis¡G

Leads Biolabs primarily engages in biopharmaceutical business, focusing on advancing breakthrough cancer therapies to improve patient outcomes. The group deploys a variety of combination treatment strategies, including bispecific antibodies, T-cell engagers (TCE), and antibody-drug conjugates (ADC), while seeking new targets and mechanisms. Since its establishment, the group has adopted a core scientific strategy of converting ¡§cold tumors¡¨ into ¡§hot tumors¡¨ to address the limitations of PD-1/PD-L1 inhibitors. This approach helps restore T-cell function and increase their numbers, transforming a small, inactive cell population into a large, active immune cell population. Unlike PD-1/PD-L1 inhibitors (which do not increase T-cell numbers), this method aims to massively activate and enhance anti-tumor immunity. Over the past decade, the group has established a proprietary technology platform based on this core logic to address significant unmet medical needs and achieve outstanding clinical results.

Leveraging its proprietary technology platform, the group has developed a well-designed and differentiated pipeline. Among the six projects that have entered clinical stages, three have shown first-in-class or best-in-class potential, indicating a high likelihood of R&D success. As of June 30, 2025, the group has one core product, Opamtistomig (LBL-024, PD-L1/4-1BB BsAb) , and 13 other drug candidates. Of these 14 candidates, six have successfully entered clinical stages, while eight are in preclinical stages. The group is currently evaluating the efficacy of its core product LBL-024 (as a monotherapy and part of combination therapies) for treating extrapulmonary neuroendocrine carcinoma, small cell lung cancer, biliary tract cancer, non-small cell lung cancer, hepatocellular carcinoma, melanoma, ovarian cancer, triple-negative breast cancer, esophageal squamous cell carcinoma, gastric cancer, and other solid tumors. Notably, LBL-024 entered a single-arm pivotal clinical trial for extrapulmonary neuroendocrine carcinoma in July 2024, becoming the world¡¦s first 4-1BB-targeted candidate to reach the pivotal clinical stage, with patient enrollment completed in August 2025. LBL-024 may also become the first approved drug for treating extrapulmonary neuroendocrine carcinoma, a cancer type with a high unmet medical need. Additionally, in October 2024, LBL-024 received Breakthrough Therapy Designation (BTD) from the NMPA for second-line treatment of extrapulmonary neuroendocrine carcinoma, and in November 2024, it received Orphan Drug Designation (ODD) from the FDA for treating neuroendocrine carcinoma.

In terms of operational business model, the group continues to adhere to a light-asset strategy while developing manufacturing and commercialization capabilities, providing significant advantages in economic feasibility and operational efficiency. To date, the group has established its own GMP-compliant pilot production facility for early clinical development of selected drug candidates. The pilot plant has an annual production capacity of up to 20 batches using single 200L or 500L disposable bioreactors.

Strategy¡G

Buy-in Price: $66.50, Target Price: $73.50, Cut Loss Price: $63.50

|

JD LOGISTICS(2618)

Analysis¡G

In recent years, JD Logistics has demonstrated accelerated growth in both revenue and profit. From 2022 to 2024, its revenue increased from CNY 137.402 billion to CNY 182.838 billion, with a compound annual growth rate (CAGR) of 16.3%. Net profit attributable to owners turned from a loss of CNY 1.397 billion in 2022 to a profit of CNY 6.198 billion in 2024. This growth trend continued into the first half of 2025, with net profit attributable to owners reaching CNY 2.580 billion. The gross profit margin improved from 7.35% in 2022 to 10.23% in 2024. Although it dipped slightly to 9.00% in H1 2025, it remained higher than the levels seen in 2022 and 2023, reflecting the benefits of economies of scale and effective cost control. In the first half of 2025, R&D expenses amounted to CNY 1.898 billion (accounting for 1.9% of revenue), with a team of 4,700 professional R&D personnel. The company¡¦s technological patents cover areas such as warehouse automation and unmanned delivery. JD Logistics has independently developed the "JD Logistics Hyperbrain," which enables dynamic optimization of the supply chain.

As of June 2025, the company operates over 1,600 warehouses and 19,000 delivery stations, with nearly 60,000 self-operated transport vehicles. JD Airlines maintains a fleet of 10 dedicated cargo aircraft operating regularly, forming an integrated "warehousing-linehaul-distribution" network capable of achieving same-day or next-day delivery in 90% of districts and counties across China.

JD Logistics¡¦ integrated supply chain services span multiple industries, including fast-moving consumer goods, home appliances, and automobiles. Its investments in technology and infrastructure have created a differentiated competitive advantage, and we are optimistic about its future development.

Strategy¡G

Buy-in Price: $13.66, Target Price: $15.00, Cut Loss Price: $13.03

|

|

Tencent (00700.HK) - AI-powered growth drives robust performance across all business segments

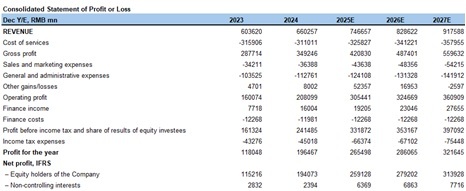

Financial performanceIn the second quarter of 2025, the company reported total revenue of CNY 184.5 billion, representing a year-on-year increase of 14.5%. In terms of profitability, operating profit reached CNY 60.1 billion, up 18.5% year-on-year, with the operating profit margin rising from 31.5% in the same period last year to 32.6%. Net profit attributable to equity holders of the company was CNY 55.6 billion, reflecting a year-on-year growth of 16.8%. By segment, Value-added Services revenue in 2Q25 saw robust growth, increasing by 15.9% year-on-year to CNY 91.4 billion, primarily driven by the sustained stability of top games. Online Marketing Services revenue grew by 19.7% year-on-year to CNY 35.8 billion, benefiting from improved user engagement, continuous AI upgrades to the advertising platform, and optimizations in the WeChat transaction ecosystem. FinTech and Business Services revenue increased by 10.1% year-on-year to CNY 55.5 billion, mainly due to growth in consumer loan services, wealth management services, as well as increased cloud services revenue and merchant service fees. Performance SummaryGaming Business

In the second quarter of 2025, the company's game revenue increased by 22.1% year-on-year to CNY 59.2 billion, accounting for 32.0% of total revenue, up from 30.1% in the same period last year. Among this, international market game revenue reached CNY 18.8 billion, a year-on-year increase of 35.3%, primarily driven by revenue growth from PUBG MOBILE and contributions from newly launched games. Domestic market game revenue grew by 16.8% year-on-year to CNY 40.4 billion, benefiting from sustained revenue growth of evergreen titles and the strong performance of the new game Delta Action, which achieved an average DAU of over 20 million in July, ranking among the top five in the industry by daily active users and top three by revenue. With a broader and more platform-diversified game portfolio, management expects reduced volatility in overall game revenue growth. Social Networks Business

In the second quarter of 2025, the company's Social Networks revenue increased by 6.3% year-on-year to CNY 32.2 billion, primarily driven by growth in game virtual item sales, live streaming services from Channels, and music subscription revenue. WeChat's user traffic continued to grow in 2Q25, with combined MAU reaching 1.411 billion, up 2.9% year-on-year. Meanwhile, monthly active accounts on QQ's smart terminal saw a slight decline compared to the same period last year. The number of registered paid value-added service subscriptions remained stable at 264 million year-on-year. Tencent Music's paid members recorded healthy growth, while Tencent Video's subscription count experienced a decline. Marketing Services Business

In the second quarter of 2025, the company's online marketing services revenue increased by 19.7% year-on-year to CNY 35.8 billion, primarily driven by AI-powered upgrades in advertising technology and new ad inventory from the Channels transaction ecosystem. According to management, the company enhanced its AI capabilities across advertising creation, placement, recommendation, and performance analysis, significantly improving ad click-through rates, conversion rates, and return on investment. This was achieved by deploying an upgraded foundational model to revamp the advertising platform architecture, which comprehensively analyzes cross-application/service ad click-through rates, transaction data, and user interactions with text, images, and videos to determine user interests in real time and optimize ad performance. Management noted that the company's short-form video ad load rate remains in the low single digits, compared to the industry average of 10%-15%. With continued AI-driven microtargeting, growing user traffic, and increasing advertiser demand, management expects advertising revenue to maintain healthy growth. FinTech and Business Services Business

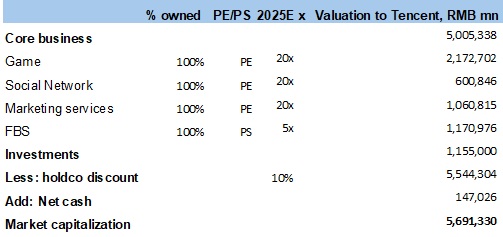

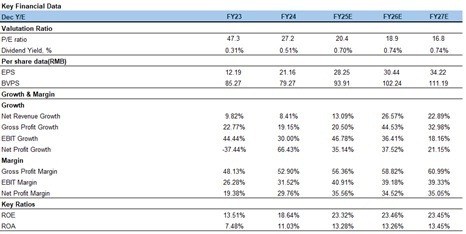

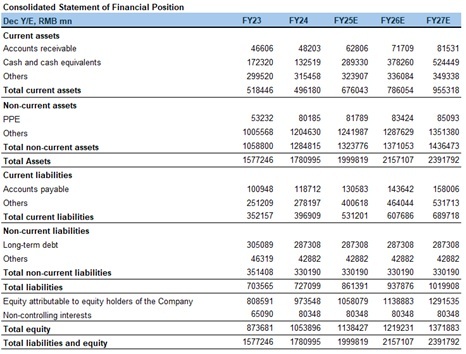

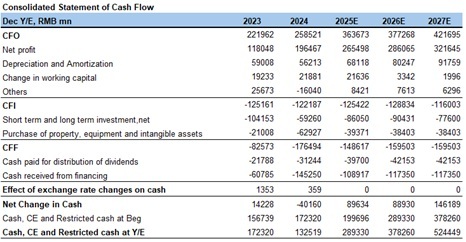

In the second quarter of 2025, the company's FinTech and Business Services revenue reached CNY 55.5 billion, representing a year-on-year increase of 10.1%. Revenue growth from FinTech services accelerated to mid-to-high single digits, primarily driven by commercial payment services and consumer credit offerings. Business Services revenue achieved double-digit year-on-year growth. Cloud services revenue growth accelerated compared to recent quarters, mainly due to increased demand for GPU leasing to support AI workloads and growth in API token revenue. Company valuationGiven the company's better-than-expected growth in gaming and advertising businesses, sustained operating leverage effects, and the empowering role of AI technology across its ecosystem, we have accordingly raised our profit forecasts. Consequently, we upwardly revise our revenue estimates for 2025-2027 to CNY 746.7/828.6/917.6 billion, with adjusted net profit attributable to equity holders projected at CNY 259.1/279.2/313.9 billion. Corresponding EPS estimates are CNY 28/30/34, implying P/E ratios of 20/18/16x at the current share price. Based on SOTP valuation methodology, applying a 10% holding discount to the latest market values or valuations of subsidiaries and invested companies, we derive a total target market capitalization of CNY 5.6 trillion for Tencent in 2025. This corresponds to a target price of HKD 682 per share. We maintain our rating as 'Accumulate'.

Risk factors1) Strict gaming regulations;

2) Weak macroeconomic environment;

3) Potential competitive threats from existing and emerging social platforms. Financials

(Current Price as of: Sep 10 2025)

Exchange rate: HKD/RMB = 0.91

Source¡G PSHK Est. Download PDF version...

| Recommendation on 17-9-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 633.500 | | Suggested purchase price | N/A | | Target Price | $ 682.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|