|

HUTCHMED(13)

Analysis¡G

HutchMed announced that it will hold a conference in Shanghai, China, on October 31, 2025 (Friday) to share the latest R&D progress. The company¡¦s Executive Vice President, Head of R&D, and Chief Medical Officer, Dr. Michael Shi, will share the company¡¦s R&D strategy and vision, including an overview of the company¡¦s Antibody-Targeted Targeted Therapy Conjugates (ATTC) platform, with a focus on its first candidate drug HMPL-A251, as well as the latest developments in its late-stage R&D pipeline. According to its interim financial report, candidate drugs from the new ATTC platform have been selected, with plans to initiate Chinese and global clinical trials for the first ATTC candidate drug by the end of 2025, followed by submissions in 2026 for multiple global new drug clinical trial applications for additional ATTC candidates to enter clinical development.

According to the introduction, the next-generation ATTC technology platform fully leverages the company¡¦s accumulated expertise over more than 20 years in targeted therapies and small molecule inhibitors. By connecting a monoclonal antibody at one end with a proprietary targeted small molecule inhibitor (SMI) payload at the other, the ATTC platform has the potential to create a rich pipeline of candidate drugs covering a wide range of tumor indications, including precision therapies for specific disease subtypes. Compared to traditional antibody-drug conjugates and/or small molecule drugs, these ATTC candidates have key potential advantages:

• Enhancing efficacy through synergistic combinations of antibodies and small molecule targeted drugs, which will target specific genetic mutations and overcome resistance to existing treatments.

• Offering higher safety and longer treatment durations. Compared to small molecules, ATTC drugs have lower toxicity to non-tumor tissues or off-target toxicity; compared to traditional cytotoxic conjugates, they have a lower risk of bone marrow suppression, which can improve treatment safety.

• Optimized pharmacokinetic characteristics to address the challenge of difficult drug targets. Compared to oral small molecule inhibitors, antibody-guided targeted delivery improves bioavailability and reduces drug interactions.

• Advantages over existing antibody-drug conjugates (ADCs). Due to the lower toxicity of SMI payloads to non-tumor tissues and their release via lysosomal cleavage within target cells, they can target tumor cell-specific mutation-driven signaling pathways. They can also be combined with existing standard treatments such as chemotherapy and immunotherapy to enhance efficacy.

• Potential for first-line applications. Chemo-free ATTCs are expected to support combinations with other targeted therapies, chemotherapy, and immunotherapy in earlier-line patient populations, offering broad market potential.

The group will prudently and actively allocate resources to accelerate the development of a series of candidate drugs from the innovative ATTC platform, including simultaneous clinical development in China and overseas. This will enrich the company¡¦s product pipeline and create more collaboration opportunities. (I do not hold the aforementioned stock).

Strategy¡G

Buy-in Price: $27.00, Target Price: $30.00, Cut Loss Price: $25.50

|

COMEC(317)

Analysis¡G

COMEC is a major shipbuilding enterprise under China State Shipbuilding Corporation Limited (CSSC). Its core business includes R&D and manufacturing of marine defense equipment, marine transportation equipment, marine development equipment, and marine technology application equipment.

In H1 2025, the company recorded an operating revenue of RMB 10.173 billion, representing a year-on-year increase of 16.54%. This growth was primarily driven by sufficient orders on hand, advantages in the batch construction of main ship types, and deepened lean management, leading to steady improvements in production output and efficiency. Net profit attributable to owners of the parent reached RMB 526 million, surging by 258.46% year-on-year. Basic earnings per share stood at RMB 0.3724, reflecting a year-on-year increase of 258.42%.

The global shipbuilding industry is currently in a new upward cycle, primarily fueled by dual catalysts: the demand for replacing aging vessels and environmental protection policies. We believe that the upward shipbuilding cycle will drive industry development, and the company¡¦s current valuation still has room for further upside.

Strategy¡G

Buy-in Price: $15.58, Target Price: $$17.80, Cut Loss Price: $14.82

|

|

Tencent (00700.HK) - AI-powered growth drives robust performance across all business segments

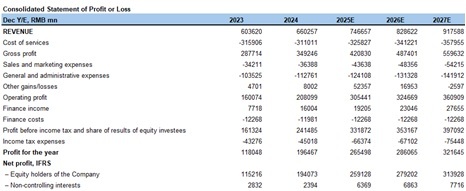

Financial performanceIn the second quarter of 2025, the company reported total revenue of CNY 184.5 billion, representing a year-on-year increase of 14.5%. In terms of profitability, operating profit reached CNY 60.1 billion, up 18.5% year-on-year, with the operating profit margin rising from 31.5% in the same period last year to 32.6%. Net profit attributable to equity holders of the company was CNY 55.6 billion, reflecting a year-on-year growth of 16.8%. By segment, Value-added Services revenue in 2Q25 saw robust growth, increasing by 15.9% year-on-year to CNY 91.4 billion, primarily driven by the sustained stability of top games. Online Marketing Services revenue grew by 19.7% year-on-year to CNY 35.8 billion, benefiting from improved user engagement, continuous AI upgrades to the advertising platform, and optimizations in the WeChat transaction ecosystem. FinTech and Business Services revenue increased by 10.1% year-on-year to CNY 55.5 billion, mainly due to growth in consumer loan services, wealth management services, as well as increased cloud services revenue and merchant service fees. Performance SummaryGaming Business

In the second quarter of 2025, the company's game revenue increased by 22.1% year-on-year to CNY 59.2 billion, accounting for 32.0% of total revenue, up from 30.1% in the same period last year. Among this, international market game revenue reached CNY 18.8 billion, a year-on-year increase of 35.3%, primarily driven by revenue growth from PUBG MOBILE and contributions from newly launched games. Domestic market game revenue grew by 16.8% year-on-year to CNY 40.4 billion, benefiting from sustained revenue growth of evergreen titles and the strong performance of the new game Delta Action, which achieved an average DAU of over 20 million in July, ranking among the top five in the industry by daily active users and top three by revenue. With a broader and more platform-diversified game portfolio, management expects reduced volatility in overall game revenue growth. Social Networks Business

In the second quarter of 2025, the company's Social Networks revenue increased by 6.3% year-on-year to CNY 32.2 billion, primarily driven by growth in game virtual item sales, live streaming services from Channels, and music subscription revenue. WeChat's user traffic continued to grow in 2Q25, with combined MAU reaching 1.411 billion, up 2.9% year-on-year. Meanwhile, monthly active accounts on QQ's smart terminal saw a slight decline compared to the same period last year. The number of registered paid value-added service subscriptions remained stable at 264 million year-on-year. Tencent Music's paid members recorded healthy growth, while Tencent Video's subscription count experienced a decline. Marketing Services Business

In the second quarter of 2025, the company's online marketing services revenue increased by 19.7% year-on-year to CNY 35.8 billion, primarily driven by AI-powered upgrades in advertising technology and new ad inventory from the Channels transaction ecosystem. According to management, the company enhanced its AI capabilities across advertising creation, placement, recommendation, and performance analysis, significantly improving ad click-through rates, conversion rates, and return on investment. This was achieved by deploying an upgraded foundational model to revamp the advertising platform architecture, which comprehensively analyzes cross-application/service ad click-through rates, transaction data, and user interactions with text, images, and videos to determine user interests in real time and optimize ad performance. Management noted that the company's short-form video ad load rate remains in the low single digits, compared to the industry average of 10%-15%. With continued AI-driven microtargeting, growing user traffic, and increasing advertiser demand, management expects advertising revenue to maintain healthy growth. FinTech and Business Services Business

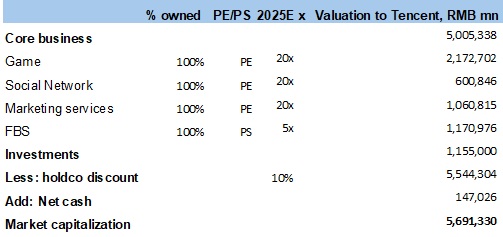

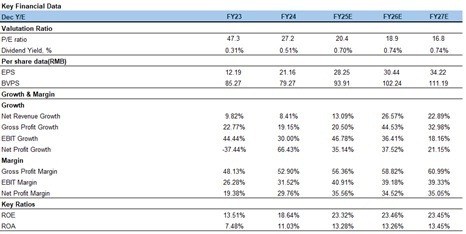

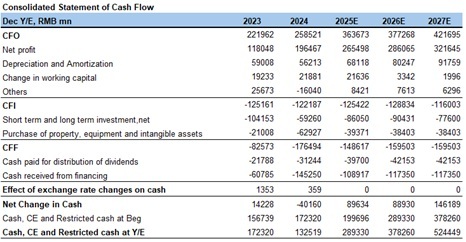

In the second quarter of 2025, the company's FinTech and Business Services revenue reached CNY 55.5 billion, representing a year-on-year increase of 10.1%. Revenue growth from FinTech services accelerated to mid-to-high single digits, primarily driven by commercial payment services and consumer credit offerings. Business Services revenue achieved double-digit year-on-year growth. Cloud services revenue growth accelerated compared to recent quarters, mainly due to increased demand for GPU leasing to support AI workloads and growth in API token revenue. Company valuationGiven the company's better-than-expected growth in gaming and advertising businesses, sustained operating leverage effects, and the empowering role of AI technology across its ecosystem, we have accordingly raised our profit forecasts. Consequently, we upwardly revise our revenue estimates for 2025-2027 to CNY 746.7/828.6/917.6 billion, with adjusted net profit attributable to equity holders projected at CNY 259.1/279.2/313.9 billion. Corresponding EPS estimates are CNY 28/30/34, implying P/E ratios of 20/18/16x at the current share price. Based on SOTP valuation methodology, applying a 10% holding discount to the latest market values or valuations of subsidiaries and invested companies, we derive a total target market capitalization of CNY 5.6 trillion for Tencent in 2025. This corresponds to a target price of HKD 682 per share. We maintain our rating as 'Accumulate'.

Risk factors1) Strict gaming regulations;

2) Weak macroeconomic environment;

3) Potential competitive threats from existing and emerging social platforms. Financials

(Current Price as of: Sep 10 2025)

Exchange rate: HKD/RMB = 0.91

Source¡G PSHK Est. Download PDF version...

| Recommendation on 15-9-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 633.500 | | Suggested purchase price | N/A | | Target Price | $ 682.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|