|

ZENERGY(3677)

Analysis¡G

Zenergy primarily engages in lithium-ion battery manufacturing, providing integrated solutions including cells, modules, battery packs, battery clusters, and battery management systems. Its diverse product portfolio includes EV batteries, ESS battery, and aviation battery. Its EV battery products can be used in BEV, PHEV, EREV, and HEV models, catering to sedans, SUVs, MPVs, and other multi-purpose vehicles. Its ESS batteries serve household, large-scale, and commercial-industrial energy storage. Its aviation batteries are used in electric manned fixed-wing aircraft and eVTOL applications.

The group focuses on the passenger vehicle power battery market and aims to expand electrochemical product applications across land, sea, and air interconnectivity (LISA).In the first half of 2025, the group¡¦s power battery business recorded sales revenue of RMB 2.985 billion and shipments of 7.63 GWh, with both revenue and shipment volume growing over 80% year-on-year. The group¡¦s ranking and market share in new energy passenger vehicle battery installations improved, reaching 7th place nationally from January to June 2025, with June alone ranking 6th, according to the China Automotive Power Battery Industry Innovation Alliance.

The energy storage business benefits from strong overseas demand, with its 104Ah standardized cell becoming a leading product for global household energy storage. Through partnerships, its products are sold in markets across Asia, Africa, and Latin America. In aviation batteries, the group achieved progress with its batteries for manned fixed-wing aircraft, securing airworthiness certification with Liaoning General Aviation¡¦s RX1E electric aircraft. It is set to achieve mass production this year, becoming the first battery supplier for mass-produced manned fixed-wing aircraft. The group¡¦s second-generation ¡§Three Highs, One Fast¡¨ aviation power battery, utilizing dual semi-solid-state technology, builds on its 2023 industry-first metrics of high safety, high energy density, high power, and fast charging.

Looking ahead, the group will expand capacity based on customer commitments to maximize efficiency. Current capacity is 25.5 GWh, with plans to add 10 GWh in Q4 2025 and 15 GWh by the end of 2026, reaching a total of 50.5 GWh. The group will deepen strategies for cell standardization, platformed battery packs, and diversified electrochemistries, while exploring technologies to produce multiple products on a single production line to enhance flexibility.(I do not shares in the mentioned stock.)

Strategy¡G

Buy-in Price: $11.60, Target Price: $13.00, Cut Loss Price: $11.00

|

FOURTH PARADIGM(6682)

Analysis¡G

FOURTH PARADIGM is a leader in China's enterprise-level artificial intelligence platform. Leveraging its technological barriers, deep industry expertise, and scalability, the company has achieved sustained high revenue growth while significantly narrowing its losses, continuously optimizing its financial structure. In the first half of 2025, the company's total revenue reached RMB 2.626 billion with a year-on-year increase of 40.7%. The adjusted net loss attributable to shareholders substantially narrowed by 71.2% to RMB 43.7 million, reflecting improved profitability. The debt-to-asset ratio dramatically decreased from insolvency (121.74%) in 2022 to 19.29% in the first half of 2025, indicating significantly reduced financial risks.

In August, the State Council issued the "Guidelines on Deepening the 'Artificial Intelligence+' Initiative," a favorable policy expected to have a profound impact on the AI industry. We believe that, benefiting from the release of enterprise AI transformation demands and the successful implementation of its "AI Agent + World Model" strategy, FOURTH PARADIGM is poised to become a key beneficiary of AI industrialization.

Strategy¡G

Buy-in Price: $60.00, Target Price: $66.00, Cut Loss Price: $57.25

|

|

Tencent (00700.HK) - AI-powered growth drives robust performance across all business segments

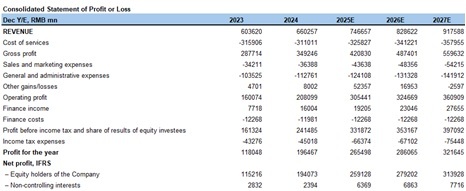

Financial performanceIn the second quarter of 2025, the company reported total revenue of CNY 184.5 billion, representing a year-on-year increase of 14.5%. In terms of profitability, operating profit reached CNY 60.1 billion, up 18.5% year-on-year, with the operating profit margin rising from 31.5% in the same period last year to 32.6%. Net profit attributable to equity holders of the company was CNY 55.6 billion, reflecting a year-on-year growth of 16.8%. By segment, Value-added Services revenue in 2Q25 saw robust growth, increasing by 15.9% year-on-year to CNY 91.4 billion, primarily driven by the sustained stability of top games. Online Marketing Services revenue grew by 19.7% year-on-year to CNY 35.8 billion, benefiting from improved user engagement, continuous AI upgrades to the advertising platform, and optimizations in the WeChat transaction ecosystem. FinTech and Business Services revenue increased by 10.1% year-on-year to CNY 55.5 billion, mainly due to growth in consumer loan services, wealth management services, as well as increased cloud services revenue and merchant service fees. Performance SummaryGaming Business

In the second quarter of 2025, the company's game revenue increased by 22.1% year-on-year to CNY 59.2 billion, accounting for 32.0% of total revenue, up from 30.1% in the same period last year. Among this, international market game revenue reached CNY 18.8 billion, a year-on-year increase of 35.3%, primarily driven by revenue growth from PUBG MOBILE and contributions from newly launched games. Domestic market game revenue grew by 16.8% year-on-year to CNY 40.4 billion, benefiting from sustained revenue growth of evergreen titles and the strong performance of the new game Delta Action, which achieved an average DAU of over 20 million in July, ranking among the top five in the industry by daily active users and top three by revenue. With a broader and more platform-diversified game portfolio, management expects reduced volatility in overall game revenue growth. Social Networks Business

In the second quarter of 2025, the company's Social Networks revenue increased by 6.3% year-on-year to CNY 32.2 billion, primarily driven by growth in game virtual item sales, live streaming services from Channels, and music subscription revenue. WeChat's user traffic continued to grow in 2Q25, with combined MAU reaching 1.411 billion, up 2.9% year-on-year. Meanwhile, monthly active accounts on QQ's smart terminal saw a slight decline compared to the same period last year. The number of registered paid value-added service subscriptions remained stable at 264 million year-on-year. Tencent Music's paid members recorded healthy growth, while Tencent Video's subscription count experienced a decline. Marketing Services Business

In the second quarter of 2025, the company's online marketing services revenue increased by 19.7% year-on-year to CNY 35.8 billion, primarily driven by AI-powered upgrades in advertising technology and new ad inventory from the Channels transaction ecosystem. According to management, the company enhanced its AI capabilities across advertising creation, placement, recommendation, and performance analysis, significantly improving ad click-through rates, conversion rates, and return on investment. This was achieved by deploying an upgraded foundational model to revamp the advertising platform architecture, which comprehensively analyzes cross-application/service ad click-through rates, transaction data, and user interactions with text, images, and videos to determine user interests in real time and optimize ad performance. Management noted that the company's short-form video ad load rate remains in the low single digits, compared to the industry average of 10%-15%. With continued AI-driven microtargeting, growing user traffic, and increasing advertiser demand, management expects advertising revenue to maintain healthy growth. FinTech and Business Services Business

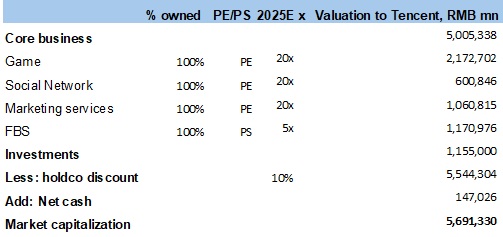

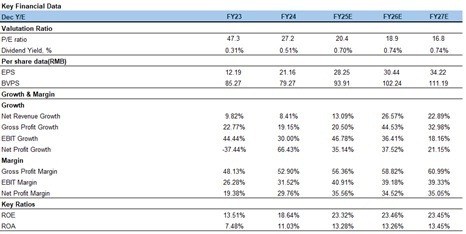

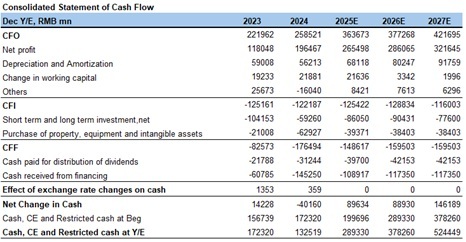

In the second quarter of 2025, the company's FinTech and Business Services revenue reached CNY 55.5 billion, representing a year-on-year increase of 10.1%. Revenue growth from FinTech services accelerated to mid-to-high single digits, primarily driven by commercial payment services and consumer credit offerings. Business Services revenue achieved double-digit year-on-year growth. Cloud services revenue growth accelerated compared to recent quarters, mainly due to increased demand for GPU leasing to support AI workloads and growth in API token revenue. Company valuationGiven the company's better-than-expected growth in gaming and advertising businesses, sustained operating leverage effects, and the empowering role of AI technology across its ecosystem, we have accordingly raised our profit forecasts. Consequently, we upwardly revise our revenue estimates for 2025-2027 to CNY 746.7/828.6/917.6 billion, with adjusted net profit attributable to equity holders projected at CNY 259.1/279.2/313.9 billion. Corresponding EPS estimates are CNY 28/30/34, implying P/E ratios of 20/18/16x at the current share price. Based on SOTP valuation methodology, applying a 10% holding discount to the latest market values or valuations of subsidiaries and invested companies, we derive a total target market capitalization of CNY 5.6 trillion for Tencent in 2025. This corresponds to a target price of HKD 682 per share. We maintain our rating as 'Accumulate'.

Risk factors1) Strict gaming regulations;

2) Weak macroeconomic environment;

3) Potential competitive threats from existing and emerging social platforms. Financials

(Current Price as of: Sep 10 2025)

Exchange rate: HKD/RMB = 0.91

Source¡G PSHK Est. Download PDF version...

| Recommendation on 12-9-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 633.500 | | Suggested purchase price | N/A | | Target Price | $ 682.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|