|

HIGHTIDE-B(2511)

Analysis¡G

Hightide Theuapeutics is an innovative biopharmaceutical company focused on researching and developing breakthrough treatments for metabolic diseases. Its core product, HTD1801, is a global first-in-class new molecular entity (NME) designed to address cardiovascular-kidney-metabolic (CKM) diseases. HTD1801 is an oral anti-inflammatory and metabolic regulator targeting the gut-liver axis with a unique dual mechanism. It activates AMPK to regulate energy homeostasis and inhibits the NLRP3 inflammasome to reduce systemic inflammation. These complementary mechanisms effectively alleviate metabolic chronic diseases and cardiovascular conditions. Supported by robust clinical data, HTD1801 demonstrates multi-efficacy, delivering metabolic benefits such as improved blood glucose control, weight reduction, and lower lipid levels (including atherosclerosis-causing lipoproteins Lp(a) and ApoB), as well as renal benefits, reduced systemic inflammation markers (e.g., hs-CRP), and liver-specific benefits (e.g., lower ALT/AST, liver fat content, and fibrosis biomarkers). Preclinical studies further reveal HTD1801¡¦s potential in cancer prevention, anti-aging, and neuroprotection. The company believes HTD1801 could become a unique broad-spectrum metabolic regulator, used as a standalone therapy or in combination with approved treatments to optimize outcomes and meet patient needs.CKM refers to a complex health condition involving heart disease, kidney disease, and metabolic disorders (e.g., diabetes, obesity). Despite progress in standard therapies, significant unmet needs remain in CKM-related diseases, as current treatments struggle to reverse kidney function decline, fully control metabolic abnormalities, or adequately address multi-system complications. With CKM-related diseases affecting nearly 90% of U.S. adults and 80% of Chinese adults, and a global diabetic population of nearly 590 million, the CKM treatment market is vast but currently underserved, urgently requiring innovative therapies. CKM¡¦s development is closely tied to chronic inflammation and metabolic imbalance, and HTD1801¡¦s dual mechanism shows exceptional therapeutic potential. Clinical studies confirm its benefits across metabolism, kidney function, obesity, and cardiovascular complications, positioning it as a foundational treatment for CKM.Currently, HTD1801 is under global development and expected to move toward commercialization this year for CKM-related conditions, including type 2 diabetes (T2DM), metabolic dysfunction-associated steatohepatitis (MASH), chronic kidney disease (CKD), obesity, primary sclerosing cholangitis (PSC), and severe hypertriglyceridemia (SHTG). Beyond HTD1801, the company is developing a pipeline of equally innovative drug candidates targeting ten potential indications. (I do not hold the aforementioned stock.)

Strategy¡G

Buy-in Price: $3.68, Target Price: $4.00, Cut Loss Price: $3.50

|

UBTECH ROBOTICS(9880)

Analysis¡G

Since 2025, Ubtech Robotics has achieved a series of critical breakthroughs in the commercialization of humanoid robots:In July, it won an RMB 90.51 million procurement project from MiYi Auto (the largest single order for humanoid robots globally). In September, it secured an additional industrial order worth RMB 250 million, raising its annual delivery target to 500 units.The company obtained a USD 1 billion credit line from Infini Capital to support market expansion in the Middle East (via joint ventures and super factories) and industrial chain integration.The Walker S series has commenced trial operations in factories of BYD, Geely, and Foxconn, validating its practicality in industrial scenarios.

The National Development and Reform Commission (NDRC) and the National Energy Administration (NEA) issued the ¡§Implementation Opinions on Promoting High-Quality Development of "AI + Energy"¡¨. The document proposes that by 2027, an integrated innovation system for energy and artificial intelligence will be initially established, the foundation for synergistic development of computing power and electricity will be strengthened, breakthroughs in AI-enabled core energy technologies will be achieved, and applications will become more extensive and in-depth.

We believe that Ubtech Robotics, as a global pioneer in humanoid robot technology, with its full-stack R&D capabilities and progress in commercialization (breakthroughs in industrial orders and strategic financing support), stands to benefit from national policies and possesses long-term growth potential. It is suitable for investors seeking long-term exposure to the technological growth trajectory.

Strategy¡G

Buy-in Price: $110.00, Target Price: $122.50, Cut Loss Price: $105.00

|

|

Meituan (3690.HK) - Intensified competition may continue to put pressure on the profitability

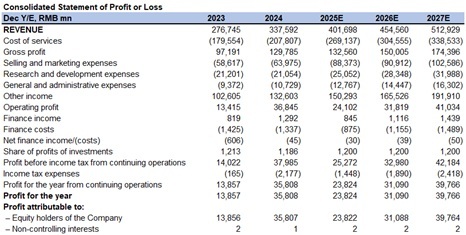

Company ProfileMeituan is a leading e-commerce platform for lifestyle services in China, providing services including food delivery, in-store, hotel and travel, and new initiatives. Its Core Local Commerce segment includes food delivery, Meituan Instashopping, in-store, hotel and travel, etc. New Initiatives include Meituan Select, Meituan Grocery, ride-hailing, shared bikes, chargingûÒ, and restaurant management systems. Financial summaryIn the second quarter of 2025, Meituan reported total revenue of 91.8 billion yuan (RMB, same below), a year-on-year increase of 11.7% and a quarter-on-quarter increase of 6.1%. In terms of profitability, operating profit was 200 million yuan, down 98.0% year-on-year and 97.9% quarter-on-quarter. Adjusted net profit was 1.5 billion yuan, down 89.0% year-on-year and 86.3% quarter-on-quarter. By segment, Core Local Commerce revenue in Q2 2025 was 65.3 billion yuan, up 7.7% year-on-year. Operating profit was 3.7 billion yuan, down 75.6% year-on-year, with an operating profit margin decreasing by 19.4 percentage points year-on-year to 5.7%, primarily due to intense competition in the food delivery industry. New Initiatives revenue was 26.5 billion yuan, up 22.8% year-on-year. Operating loss was 1.9 billion yuan, broadening by 43.1% year-on-year, mainly due to expanded overseas expansion. The operating loss ratio improved by 3.1 percentage points quarter-on-quarter to 7.1%, primarily due to improved operational efficiency. In terms of expenses, sales costs in Q2 2025 were 61.4 billion yuan, up 27.0% year-on-year, accounting for 66.9% of revenue, up from 62.6% in the previous quarter, mainly due to rider subsidies and the expansion of instant retail business. Sales and marketing expenses were 22.5 billion yuan, up 51.8% year-on-year, accounting for 24.5% of revenue, up from 18.0% in the previous quarter, primarily due to increased user incentive spending. R&D expenses were 6.3 billion yuan, up 17.2% year-on-year, accounting for 6.8% of revenue, remaining stable quarter-on-quarter. General and administrative expenses were 2.7 billion yuan, accounting for 2.9% of revenue, also stable quarter-on-quarter. Financial performanceFood Delivery & Instashopping Business

The food delivery industry is becoming increasingly competitive. In April, competitor JD Delivery rapidly increased order volumes through its 'Billion-Dollar Subsidy' program, and competition intensified further in May when Taobao Flash Purchase joined the subsidy war. In response, the company employed strategies such as 'Shen Qiang Shou', 'Pin Hao Fan', and subsidies for both consumers and merchants to tackle the competition. This drove overall expansion in the food delivery market order volume. We estimate that Meituan's food delivery order volume growth accelerated to 10.0% year-on-year in Q2 2025, boosted by competition, while delivery service revenue grew by only 2.8% year-on-year, slower than the order volume growth. Meanwhile, the AOV for food delivery declined more significantly due to subsidies, coupled with higher per-order subsidies year-on-year and increased costs from improved social security systems. We expect the per-order UE for food delivery to turn negative in Q2 2025. Looking ahead to the second half of the year, intensified competition is expected to continue driving order volume growth, but profitability may remain under pressure. In Q3, Taobao Flash Purchase launched a 50-billion-yuan subsidy plan and initiated the 'Super Saturday' campaign. The company quickly responded by matching subsidies, leading to record-high order volumes in instant retail. As of July 12, peak order volume reached 150 million orders, with 'Shen Qiang Shou' contributing over 50 million orders and 'Pin Hao Fan' contributing over 35 million orders. Due to the increased intensity and prolonged duration of competition in food delivery and flash purchase, we expect year-on-year order volume growth for both segments in Q3 and Q4 to further accelerate compared to Q2. However, profitability is likely to remain under pressure. Considering management's guidance that the Core Local Commerce segment may turn from profit to loss in Q3, we expect the operating profit margin for Meituan's food delivery and flash purchase businesses to turn negative in 2025. New Business

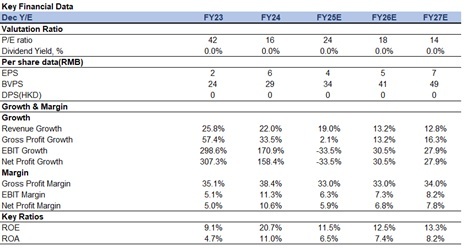

The company has restructured its fresh grocery business, significantly scaling back 'Meituan Select' and fully committing to 'Xiaoxiang Supermarket', with plans to cover all first- and second-tier cities. For overseas operations, Keeta has entered the Qatar market, setting a long-term goal of achieving $100 billion in GMV over the next decade. While the company is not rushing this process, it remains optimistic about the long-term growth potential. According to management, due to restructuring costs associated with business adjustments and the expansion of Keeta in the Middle East, the loss for the New Initiatives segment is expected to widen to 2.3-2.4 billion yuan in the third quarter. Company valuationThe company's financial resources are more limited compared to Alibaba, which may put it at a disadvantage in a prolonged cash-burning competition and pose a risk of market share loss. However, considering the potential for profit recovery between 2026 and 2027, we have adjusted our revenue forecasts for 2025-2027 to 401.7/454.6/512.9 billion yuan, with net profit attributable to shareholders at 23.8/31.1/39.8 billion yuan, corresponding to EPS of 4/5/7 yuan. Based on the SOTP valuation method, we estimate Meituan's total target market capitalization for 2025 to be 664.7 billion yuan. We have lowered the target price to HK$118.3. The current stock price corresponds to a PE ratio of 24x/18x/14x for 2025-2027. We downgrade our rating to 'Accumulate'. The segment valuation includes the following parts: 1) Core Local Commerce is valued at 526.8 billion yuan, using an 8% weighted average cost of capital and 5% perpetual growth rate;

2) New Initiatives are valued at 81.8 billion yuan, applying a 0.8x 2025 P/S multiple;

3) Net cash amounts to 56.1 billion yuan. Risk factors1) New business performance below expectations;

2) Intensified competition in the food delivery and travel industries;

3) Weaker than expected recovery in consumer demand. Financials

(Closing price as of 3 Sep 2025)

Exchange rate: RMB/HKD = 1.09

Source¡G PSHK Est. Download PDF version...

| Recommendation on 9-9-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 100.500 | | Suggested purchase price | N/A | | Target Price | $ 118.300 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|