|

MAO GEPING(1318)

Analysis¡G

Mao Geoing is positioned in the high-end cosmetics and product market, owning two major brands, ¡§MAOGEPING¡¨ and ¡§Love Keeps¡¨ catering to diverse consumer groups. In the first half of this year, the group continued to advance product innovation and category expansion, launching two new high-end perfume series, ¡§Guoyun Ningxiang¡¨ and ¡§Eastern Whisper Enlightenment¡¨ extending its beauty product offerings into the fragrance market. On the channel side, the group continued to enhance brand image and improve store efficiency, further strengthening its high-end cosmetics brand identity. As of June 30, 2025, its product portfolio included over 400 SKUs across cosmetics, skincare, and fragrances.

For the first half of the year ending June 30, 2025, the group achieved revenue of 2.588 billion RMB, a year-on-year increase of 31.3%, and net profit of 670 million RMB, up 36.1%. By product category, cosmetics sales revenue reached 1.422 billion RMB, growing 31.1%. Among these, base makeup products performed strongly, with retail sales of the Luxury Caviar Cushion and the Luminous Light Veiling Pressed Powder each exceeding 200 million RMB. Meanwhile, the group continued to refine and expand its full-range product layout in cosmetics subcategories, launching a new online product, the Crystal Starry Sky Eyeshadow, in March, which achieved retail sales of over 4 million RMB.

In skincare, the group¡¦s products include face creams, eye care, masks, serums, and cleansers, generating sales revenue of 1.087 billion RMB in the first half, up 33.4%. Two star products, the Luxury Caviar Facial Mask and Luxury Regenerating Black Cream, recorded retail sales exceeding 600 million RMB and 200 million RMB, respectively. A new high-end skincare product, the Premium Nutritive Revitalizing Lotion, launched this year, achieved retail sales of over 16 million RMB.(I do not hold the aforementioned stock.)

Strategy¡G

Buy-in Price: $99.00, Target Price: $108.00, Cut Loss Price: $94.00

|

FOXCONN IND(601138.CH)

Analysis¡G

The Company is a world leading professional design and manufacturing service provider for communication network equipment, cloud service equipment, precision tools and industrial robots, providing customers with intelligent manufacturing services for new forms of electronic equipment products with the industrial Internet platform as the core. The Company released its semi annual report for 2025,with a sales revenue of RMB360.76 billion yuan in 2025H1, hoh+5.16%¡Ayoy+35.58% and a net profit attributable to the parent company of 12.113 billion yuan, hoh-16.33%¡Ayoy+38.61%. In 2025, many large cloud service providers around the world continued to expand their capital expenditures on AI infrastructure construction, and their investment in AI computing power accelerating, driving the Company¡¦s overall server revenue of 2Q25 to increase by more than 50%, cloud service provider server revenue to increase by more than 150% year-on-year, and AI to increase by more than 60% yoy. The MGMT expects the strong momentum to continue in 25H2.

Strategy¡G

Buy-in Price: $54.60, Target Price: $60.20, Cut Loss Price: $51.50

|

|

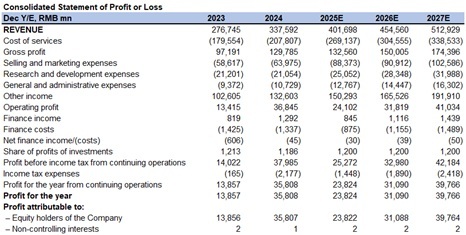

Meituan (03690.HK) - Intensified competition may continue to put pressure on the profitability

Company ProfileMeituan is a leading e-commerce platform for lifestyle services in China, providing services including food delivery, in-store, hotel and travel, and new initiatives. Its Core Local Commerce segment includes food delivery, Meituan Instashopping, in-store, hotel and travel, etc. New Initiatives include Meituan Select, Meituan Grocery, ride-hailing, shared bikes, chargingûÒ, and restaurant management systems. Financial summaryIn the second quarter of 2025, Meituan reported total revenue of 91.8 billion yuan (RMB, same below), a year-on-year increase of 11.7% and a quarter-on-quarter increase of 6.1%. In terms of profitability, operating profit was 200 million yuan, down 98.0% year-on-year and 97.9% quarter-on-quarter. Adjusted net profit was 1.5 billion yuan, down 89.0% year-on-year and 86.3% quarter-on-quarter. By segment, Core Local Commerce revenue in Q2 2025 was 65.3 billion yuan, up 7.7% year-on-year. Operating profit was 3.7 billion yuan, down 75.6% year-on-year, with an operating profit margin decreasing by 19.4 percentage points year-on-year to 5.7%, primarily due to intense competition in the food delivery industry. New Initiatives revenue was 26.5 billion yuan, up 22.8% year-on-year. Operating loss was 1.9 billion yuan, broadening by 43.1% year-on-year, mainly due to expanded overseas expansion. The operating loss ratio improved by 3.1 percentage points quarter-on-quarter to 7.1%, primarily due to improved operational efficiency. In terms of expenses, sales costs in Q2 2025 were 61.4 billion yuan, up 27.0% year-on-year, accounting for 66.9% of revenue, up from 62.6% in the previous quarter, mainly due to rider subsidies and the expansion of instant retail business. Sales and marketing expenses were 22.5 billion yuan, up 51.8% year-on-year, accounting for 24.5% of revenue, up from 18.0% in the previous quarter, primarily due to increased user incentive spending. R&D expenses were 6.3 billion yuan, up 17.2% year-on-year, accounting for 6.8% of revenue, remaining stable quarter-on-quarter. General and administrative expenses were 2.7 billion yuan, accounting for 2.9% of revenue, also stable quarter-on-quarter. Financial performanceFood Delivery & Instashopping Business

The food delivery industry is becoming increasingly competitive. In April, competitor JD Delivery rapidly increased order volumes through its 'Billion-Dollar Subsidy' program, and competition intensified further in May when Taobao Flash Purchase joined the subsidy war. In response, the company employed strategies such as 'Shen Qiang Shou', 'Pin Hao Fan', and subsidies for both consumers and merchants to tackle the competition. This drove overall expansion in the food delivery market order volume. We estimate that Meituan's food delivery order volume growth accelerated to 10.0% year-on-year in Q2 2025, boosted by competition, while delivery service revenue grew by only 2.8% year-on-year, slower than the order volume growth. Meanwhile, the AOV for food delivery declined more significantly due to subsidies, coupled with higher per-order subsidies year-on-year and increased costs from improved social security systems. We expect the per-order UE for food delivery to turn negative in Q2 2025. Looking ahead to the second half of the year, intensified competition is expected to continue driving order volume growth, but profitability may remain under pressure. In Q3, Taobao Flash Purchase launched a 50-billion-yuan subsidy plan and initiated the 'Super Saturday' campaign. The company quickly responded by matching subsidies, leading to record-high order volumes in instant retail. As of July 12, peak order volume reached 150 million orders, with 'Shen Qiang Shou' contributing over 50 million orders and 'Pin Hao Fan' contributing over 35 million orders. Due to the increased intensity and prolonged duration of competition in food delivery and flash purchase, we expect year-on-year order volume growth for both segments in Q3 and Q4 to further accelerate compared to Q2. However, profitability is likely to remain under pressure. Considering management's guidance that the Core Local Commerce segment may turn from profit to loss in Q3, we expect the operating profit margin for Meituan's food delivery and flash purchase businesses to turn negative in 2025. New Business

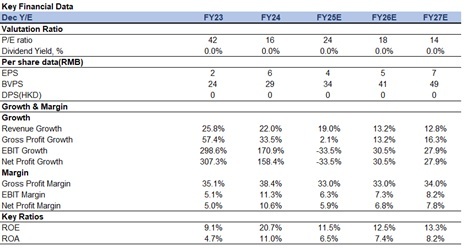

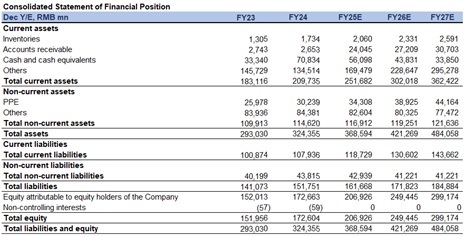

The company has restructured its fresh grocery business, significantly scaling back 'Meituan Select' and fully committing to 'Xiaoxiang Supermarket', with plans to cover all first- and second-tier cities. For overseas operations, Keeta has entered the Qatar market, setting a long-term goal of achieving $100 billion in GMV over the next decade. While the company is not rushing this process, it remains optimistic about the long-term growth potential. According to management, due to restructuring costs associated with business adjustments and the expansion of Keeta in the Middle East, the loss for the New Initiatives segment is expected to widen to 2.3-2.4 billion yuan in the third quarter. Company valuationThe company's financial resources are more limited compared to Alibaba, which may put it at a disadvantage in a prolonged cash-burning competition and pose a risk of market share loss. However, considering the potential for profit recovery between 2026 and 2027, we have adjusted our revenue forecasts for 2025-2027 to 401.7/454.6/512.9 billion yuan, with net profit attributable to shareholders at 23.8/31.1/39.8 billion yuan, corresponding to EPS of 4/5/7 yuan. Based on the SOTP valuation method, we estimate Meituan's total target market capitalization for 2025 to be 664.7 billion yuan. We have lowered the target price to HK$118.3. The current stock price corresponds to a PE ratio of 24x/18x/14x for 2025-2027. We downgrade our rating to 'Accumulate'. The segment valuation includes the following parts: 1) Core Local Commerce is valued at 526.8 billion yuan, using an 8% weighted average cost of capital and 5% perpetual growth rate;

2) New Initiatives are valued at 81.8 billion yuan, applying a 0.8x 2025 P/S multiple;

3) Net cash amounts to 56.1 billion yuan. Risk factors1) New business performance below expectations;

2) Intensified competition in the food delivery and travel industries;

3) Weaker than expected recovery in consumer demand. Financials

(Closing price as of 3 Sep 2025)

Exchange rate: RMB/HKD = 1.09

Source¡G PSHK Est. Download PDF version...

| Recommendation on 8-9-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 100.500 | | Suggested purchase price | N/A | | Target Price | $ 118.300 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|