|

HORIZONROBOT-W(9660)

Analysis¡G

Horizon Robotics primarily focuses on providing advanced driver assistance systems (ADAS) and high-level autonomous driving (AD) solutions for passenger vehicles, holding a leading position in the ADAS market. In the first half of this year, the group maintained the top market share in China for basic and overall ADAS solutions among Chinese automakers, with shares of 45.8% and 32.4%, respectively. Additionally, shipments of the vehicle-grade Journey series processing hardware reached 1.98 million units, doubling year-over-year.In the first half of the year, the group delivered nearly 2 million units of products and solutions, a year-over-year increase of over 100%. Driven by the mass production of the Journey 6 series, shipments of mid-to-high-end product solutions (such as those supporting high-speed NOA functions) reached 980,000 units, accounting for 49.5% of total shipments, a sixfold increase from the previous year, reflecting significant structural optimization. Benefiting from the large-scale rollout of Journey 6 processing hardware, the average selling price (ASP) per vehicle significantly increased, driving product and solution revenue to 778 million yuan, a more than threefold year-over-year increase, with the gross margin rising to 45.6%. In the licensing and services segment, revenue reached 738 million yuan, with a robust gross margin of 89.7%.The group achieved revenue of 1.567 billion yuan in the first half, a significant year-over-year increase of 67.6%; gross profit reached 1.024 billion yuan, up 38.6%, with a comprehensive gross margin of 67.1%. The loss was 5.233 billion yuan, narrowed by 2.6% year-over-year. The group noted that, excluding cloud computing costs for model training, operational efficiency has steadily improved. The group is optimistic about mid-to-high-end ADAS solutions and is advancing the development of its full-scenario urban ADAS solution, Horizon SuperDrive (HSD), which it believes will serve as the technical foundation for future robotaxi autonomous driving. As a result, the group strategically increased R&D spending on cloud services, recording an adjusted operating loss of 1.111 billion yuan.In the first half, Horizon SuperDrive (HSD) secured designated cooperation with multiple domestic automakers for over 10 vehicle models. More notably, it is set to debut globally under Chery¡¦s Xingtu brand in 2025, marking the group¡¦s entry into large-scale commercialization. (I do not hold the aforementioned stock.)

Strategy¡G

Buy-in Price: $9.30, Target Price: $10.30, Cut Loss Price: $8.80

|

INNOVENT BIO(1801)

Analysis¡G

Innovenbio is a leading domestic biopharmaceutical innovation company. Through independent research and development and cooperation, it has created a rich and balanced R&D pipeline, covering major disease fields such as tumors, metabolism, autoimmune diseases, and ophthalmology. It involves major drug forms such as monoclonal antibodies, bispecific antibodies, fusion proteins, small molecules, and cell therapy. The Company recorded a revenue of 5.95 billion yuan (yoy+50.6%) in the first half of the year, including product revenue of 5.23 billion yuan (yoy+37.3%) and authorization fee revenue of 666 million yuan, mainly from Roche's down payment; IFRS profit was RMB 834 million (compared to - RMB 393 million in the same period last year), and Non IFRS profit was RMB 1.213 billion (compared to - RMB 160 million in the same period last year), achieving comprehensive profitability. The Company's development blueprint predicts that EBITDA and net profit will continue to increase by the end of 2025; By 2027, there will be 20 commercial products with corresponding product revenues reaching 20 billion yuan; By 2030, five pipelines will enter the global center Phase III clinical trials and become a world-class biopharmaceutical company.

Strategy¡G

Buy-in Price: $103.28, Target Price: $114.70, Cut Loss Price: $97.50

|

|

Xinyi Glass (868 HK) - Automotive Glass Became a Key Support

Company ProfileXinyi Glass is a leading global glass manufacturer with products including float glass, automotive glass and architectural glass. The company has production bases in China and Southeast Asia and continues to expand its overseas markets. Investment SummaryH1 2025 Results Pressured by Weak Float Glass Market

Xinyi Glass recently released its interim results for 2025. In H1 2025, the Company recorded revenue of RMB9.821 billion (RMB, the same below), down 9.7% yoy and 14% mom; net profit attributable to the parent company was RMB1.01 billion, down 59.6% yoy. Basic EPS was RMB0.2325, and the interim dividend per share was HK$0.125, representing a payout ratio of 49.3%, compared to 47.9% in the same period last year.

The decline in results was mainly due to: 1) insufficient industry demand, which led to a continued fall in the average selling price of float glass products and reduced gross profit from architectural glass products, negatively impacting gross margin; 2) one-off impairment losses arising from production suspension and significant foreign exchange gains in the same period last year; 3) a sharp decrease in the share of profit contributed by Xinyi Solar; 4) reduced income from government subsidies and sales of automated machinery; and 5) a weakened cost dilution effect due to declining revenue, further eroding profit. Sluggish Float Glass Prices Dragged Gross Margin Down by 2.6ppts

In H1 2025, the overall gross margin was 31.6%, down 2.6ppts from 34.2% in the same period last year.

Due to slower-than-expected growth in completed floor space, float glass prices came under pressure. As of end-June 2025, the domestic average price of 5mm float glass was RMB66 per heavy box, down 15.4% yoy, and the industry as a whole remained in a trough. The Company's float glass segment faced considerable pressure, with profitability weighed down by weak demand. In H1, revenue from float glass fell 16.4% yoy to RMB5.38 billion, and segment gross margin narrowed by 10.5ppts yoy to 17.8%. The Company plans to enhance effective float glass capacity through the phased commissioning of two production lines in Indonesia, aiming to achieve some flexibility in future operations. Automotive Glass Became a Key Support to H1 Results

Benefiting from the rapid expansion of the new energy vehicle market and the Company's continued efforts in channel development, revenue from the automotive glass segment reached RMB3.32 billion, up 10.6% yoy. Segment gross margin rose by 4.9ppts yoy to 54.5%, mainly due to ongoing investment in high-value-added products, which lifted both product unit prices and profitability. Meanwhile, the revenue contribution from automotive glass increased from 18% in 2021 to 34% in H1 2025. The higher share of this high-margin business helped ease the pressure from declining profitability in the float glass segment. Currently, automotive glass maintains a capacity utilization rate of over 85%, with a 26% share in the global after-market.

In H1, revenue from the Company's architectural glass business dropped 22.3% yoy to RMB1.12 billion, mainly due to a decrease in newly completed property projects in China. Although revenue declined, the gross margin of architectural glass rose by 1.3ppts yoy to 29.7%, primarily supported by lower float glass input prices. Meanwhile, the Company is also increasing investment in differentiated products such as low-emissivity glass to enhance product value and mitigate business downturn pressure. Expense Ratio Increased, But Financial Stability Improved

In H1, the period expense ratio was 18.5%, up 2.9ppts yoy, mainly due to the weakened dilution effect resulting from revenue decline. At the same time, asset disposal and impairment losses totaled RMB220 million, up RMB210 million yoy, primarily because of production suspension at certain float glass lines in Hainan.

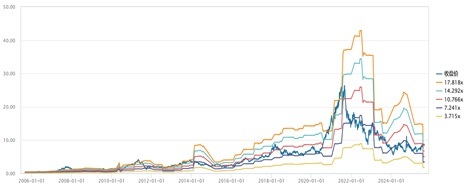

The net gearing ratio decreased by 2ppts from end-2024 to 14.3%, and cash and bank deposits increased to RMB2.033 billion, up 18.9% from end-2024. As of 30 June 2025, the Company's debt-to-asset ratio stood at 28.5%, and its equity multiplier was 128.5%, outperforming other major enterprises in the industry during the same period. Additionally, through adjustments in loan structure, the average loan interest rate further declined to 2.74%. Overall, the Company's financial stability improved during the industry trough, helping to maintain stronger risk resilience amid market fluctuations. Overseas Markets Are the Current FocusRegarding overseas markets, the new automotive glass production line launched in Malaysia last year is still in the ramp-up phase; the new line in Indonesia commenced operation in May this year, targeting the US market. However, the US market currently accounts for less than 10% of revenue, leaving considerable room for future growth. After years of expansion in China and major Southeast Asian economic zones, the Company continues to seek acquisition and greenfield project opportunities to facilitate market entry, reduce labour and raw material costs, and benefit from more favourable tax policies and energy advantages. Valuation and Investment ThesisWe expect that the Company's EPS to be RMB0.51/0.63/0.78 in 2025/2026/2027, we upgrade the target price to HK$9.2, equivalent to 16.8/13.5/10.7x P/E for 2025/2026/2027. Also, the "Accumulate" rating is maintained. P/E Band

Source: Wind, Phillip Securities Hong Kong Research Risk Factors1) Policy and market volatility risks: The glass industry is highly dependent on downstream industry policies such as construction, automobiles, and new energy. If photovoltaic subsidies are reduced, new energy vehicle promotion is not as expected, or real estate regulation is intensified, it may lead to a contraction in demand;

2) Raw material and cost control risks: The prices of key raw materials such as soda ash and natural gas are significantly affected by energy policies and geopolitical factors, and their fluctuations will directly erode the company's gross profit margin;

3) Technological iteration and substitution risk: If the enterprise's R&D investment is insufficient or the technology route is chosen incorrectly, it may lead to the depreciation of existing production capacity. Financial Data

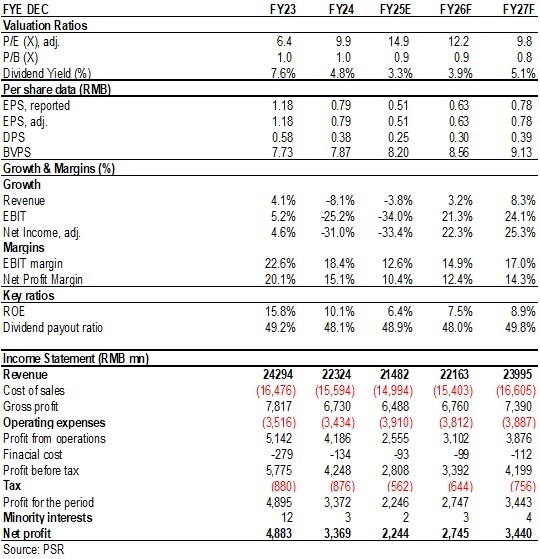

Source: Company reports, Phillip Securities Est.

(Closing price as at 2 September 2025)

Click to download PDF version...

| Recommendation on 4-9-2025 | | Recommendation | Accumulate (Maintain) | | Price on Recommendation Date | $ 8.360 | | Suggested purchase price | N/A | | Target Price | $ 9.200 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|