|

CHIFENG GOLD(6693)

Analysis¡G

In the first half of 2025, Chifeng Jilong Gold Mining achieved strong financial performance, with operating revenue of RMB 5.272 billion, up 25.64% year-on-year. Net profit attributable to shareholders reached RMB 1.107 billion, a 55.79% increase. Net cash flow from operating activities was RMB 16.13, growing 12.39% year-on-year. As of June 30, 2025, the debt-to-asset ratio was 37.19%, down 10.06 percentage points from the start of the year.

The significant growth in interim results was driven by rising gold prices and the company¡¦s focus on cost reduction, including strict control of non-production expenses and effective production cost management.

Internationally, Chifeng Gold made progress at key projects like the Sepon Mine in Laos. In June 2025, Lane Xiang Mining¡¦s first-phase exploration at the SND Project uncovered a large-scale porphyry gold-copper deposit, with proven resources of 131.5 million tonnes at a gold equivalent grade of 0.81 tonnes/tonne, totaling 106.9 tonnes of gold equivalent metal, setting the stage for large-scale development.

Domestically, Jilong Mining completed 9,143 meters of underground drilling and 11,597 meters of surface drilling, totaling 20,740 meters. Wulong Mining advanced exploration with 12,560 meters of underground work and 8,360 meters of deep drilling. The company also expanded its mining rights by securing new exploration permits covering 1.0705 square kilometers. (I do not hold the aforementioned stock)

Strategy¡G

Buy-in Price: $26.70, Target Price: $29.80, Cut Loss Price: $25.40

|

ESTUN AUTOMATION(002747.CH)

Analysis¡G

The company is a leading enterprise in China's industrial robot industry, building a full industry chain ecosystem of "core components+ontology+robot integrated applications" for robots. In Q1 2025, its market share in the domestic industrial robot market reached 10.3%, ranking first. The company was founded in 1993, starting with CNC systems for metal forming machine tools, and gradually expanding its business to electro-hydraulic servo systems and AC servo systems. In 2011, it began developing robot bodies. In the first half of 2025, the company achieved a revenue of 2.55 billion yuan, a year-on-year increase of 17.5%; Realize a net profit attributable to the parent company of 7 million yuan, turning losses around year-on-year. Starting from the second quarter, with the recovery of downstream market demand and the acceleration of domestic substitution process, the company's industrial robot sales have grown rapidly. The company plans to accelerate the capture of the high-end robot market through AI integration and domestic substitution.

Strategy¡G

Buy-in Price: RMB23.08, Target Price: RMB25.90, Cut Loss Price: RMB21.50

|

|

CHICMAX (2145.HK) - Multi-brand layout strategy brings continuous revenue growth

OverviewCHICMAX is a research-driven, multi-brand leader in the cosmetics industry. Founded in 2002, the company owns three core brands---KANS, ONE LEAF, and Baby Elephant---and has successfully established new growth drivers such as newpage and ARMIYO. It operates across four major segments: skincare, hair care, maternal and infant products, and cosmetics, with two self-built R&D centers and two supply chains worldwide. Performance reviewIn H1 2025, the company's revenue reached RMB 4.108 billion (RMB, same below), representing a year-on-year increase of 17.3%. Net profit attributable to owners of the parent company was RMB 556 million, up 34.7% year-on-year. The growth in the company's revenue and profit was primarily driven by sustained revenue increase from the comprehensive multi-category, omni-channel strategy of the science-driven anti-aging skincare brand KANS, alongside a significant year-on-year revenue growth from the Chinese infant and child efficacy skincare brand newpage. Basic earnings per share were RMB 1.32, an increase of 30.7% year-on-year. An interim dividend of RMB 0.5 per share was declared, with cumulative dividend distributions exceeding RMB 1.2 billion since listing, reflecting the company's sustained high dividend payout ratio. Implementing a multi-brand strategy, Baby Elephant has entered the children's cosmetics marketThe flagship brand KANS maintained steady growth.

Launched in 2003, KANS is positioned as a "science-driven anti-aging" skincare brand, dedicated to meeting the evolving anti-aging needs of Asian women across all age groups, with a broad target customer base. In H1 2025, its revenue reached RMB 3.344 billion, representing a year-on-year increase of 14.3%. This growth was primarily driven by the overall upgrade of the KANS brand and expanded product categories, as well as sustained revenue growth across all channels. KANS accounted for 81.4% of the company's total revenue. The brand achieved widespread success across multiple platforms, with monthly GMV consistently ranking No. 1 among beauty brands on Douyin. It also secured the top spot on Douyin E-commerce's H1 2025 skincare brand overall rankings. The bestselling product, KANS Red Waist Series, remained highly popular, with cumulative sales exceeding 15 million sets across all channels. The KANS X-Peptide Ultra-Frequency Series generated cumulative sales of over RMB 200 million across all channels. The KANS brand is actively expanding into multiple categories, including men's series, haircare series, and makeup series, to meet diverse consumer needs.

ONE LEAF's Contribution to revenue continued to decline

Launched in 2004, ONE LEAF targets younger users. It employs advanced technology blended with natural ingredients to create effective and natural skincare products. In H1 2025, ONE LEAF was repositioned as a "science-backed skincare brand specializing in botanical extracts" and launched the Brightening Radiance Series and Black Tea Purifying Cleansing Cream. Its revenue for H1 2025 was RMB 89 million, a year-on-year decrease of 29%, accounting for 2.2% of total revenue. We believe that ONELEAF's brand revitalization is expected to attract more young consumers, which should help restore its revenue.

Baby Elephant pioneers the children's makeup Market

The company launched Baby Elephant in 2015, positioning it as a professional maternal and infant care brand tailored for Chinese children's skin, with the core philosophy of "minimalist ingredients, safe and effective," aiming to accompany every baby's healthy and happy growth. In 2024, it sold 400,000 units of children's makeup products and was certified by Frost & Sullivan as the top seller in China's online children's makeup market for that year. According to the 2024-2030 China Children's Makeup Industry Market In-Depth Assessment and Investment Profit Forecast Report released by Boyan Consulting and market research online, the market size of China's children's makeup industry has grown significantly in recent years and is expected to reach RMB 44 billion by 2025. Meanwhile, data from Magic Mirror Insights showed that the GMV of children's makeup products on Taobao and Tmall platforms increased by over 80% year-on-year in 2024. We believe the Chinese children's makeup market holds immense growth potential. With the widespread availability of internet access, many children now have their own mobile devices and can easily learn about makeup through platforms like WeChat, Douyin, and Rednote. The parenting attitudes of post-80s and post-90s generations have evolved (reflected in the extension of the "appearance economy" and the awakening of children's aesthetic education awareness), while innovations in product safety and fun, coupled with the two-child and three-child policies expanding the consumer base, have collectively driven the development of the children's makeup industry. CHICMAX has demonstrated keen insight by strategically entering the children's makeup market early, expanding its brand portfolio, and differentiating itself from other cosmetics companies to gain a competitive edge. In H1 2025, Baby Elephant generated revenue of RMB 159 million, a year-on-year decrease of 8.7%, primarily due to the initial effects of the brand's transformation and adjustment, which narrowed the decline. This revenue accounted for 3.9% of the company's total revenue.

Newpage Achieved Exponential Growth

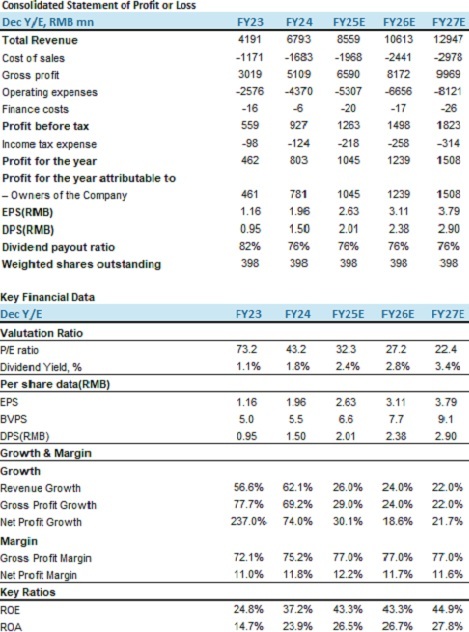

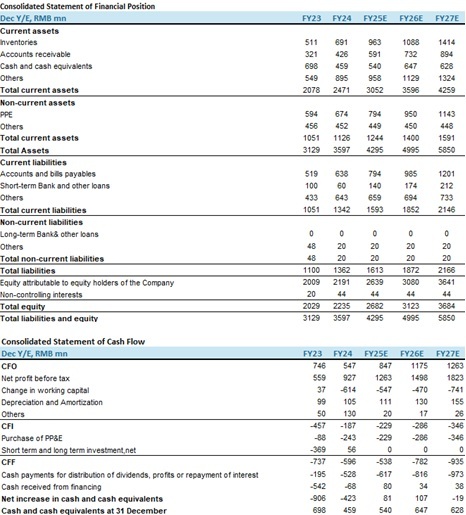

Launched in 2022, Newpage is a pediatric efficacy skincare brand focused on babies with sensitive skin, positioned as "co-developed with medical professionals." In terms of product offerings, Newpage has expanded into three main categories: skincare, cleansing and bathing, and hygiene products. It caters to different age groups with segmented product lines, including infant series, school-age series, and adolescent series, comprehensively covering the children's skincare market. The hero product, Newpage Baby Soothing Cream, sold explosively during the 2025 618 shopping festival, with over 330,000 bottles sold, ranking No. 1 on Tmall in sales, positive reviews, and repurchase rate for children's face creams. In H1 2025, revenue reached RMB 397 million, a significant year-on-year increase of 146.5%. This growth was primarily driven by the rapid sales expansion of Newpage's star products, with online channel sales in the first half alone matching the full-year 2024 performance. Newpage accounted for 9.6% of the company's total revenue. We believe that Newpage has achieved substantial growth in both reputation and sales, and we are optimistic about its long-term growth potential. Valuation and Investment RecommendationAccording to data from the National Bureau of Statistics, China's total retail sales of consumer goods in H1 2025 reached RMB 24.5458 trillion, a year-on-year increase of 5%. Retail sales of cosmetics amounted to RMB 229.1 billion, up 2.9% year-on-year, exceeding the growth rate of H1 2024, demonstrating resilience in cosmetics consumption and a sustained upward trend.Data from Qingyan Intelligence shows that in July, the beauty and skincare category dominated Douyin's platform, accounting for 60.64% of GMV, with a year-on-year increase of 28.48% but a month-on-month decrease of 24.45%.The company's core brand, KANS, targets the mass skincare market, while Newpage exemplifies strong capabilities in incubating emerging brands. We expect further revenue growth from these two brands in the second half of the year. The company has achieved high growth in revenue and net profit attributable to parents for three consecutive years, supported by robust cash flow, providing a solid foundation for brand marketing and R&D investments. We forecast the company's operating revenue for 2025-2027 to be RMB 8.559 billion, RMB 10.613 billion, and RMB 12.947 billion, respectively, with EPS of RMB 2.63, RMB 3.11, and RMB 3.79. The corresponding P/E ratios are 32.3x, 27.2x, and 22.4x. We set a target price of HKD 100 for the company, corresponding to a 2025 expected P/E of 35x, and assign an "Accumulate" rating. (Current price as of Sep 1) Risk factors1) Downward macroeconomic situation;

2) Intensified industry competition;

3) Management changes;

4) New product promotion failing to meet expectations. Financial Data

Current Price as of: 1 Sep 2025

Source: PSHK Est. Download PDF Version...

| Recommendation on 3-9-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 92.200 | | Suggested purchase price | N/A | | Target Price | $ 100.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|