|

TUYA-W(2391)

Analysis¡G

Tuya primarily provides Internet of Things (IoT) Platform-as-a-Service (PaaS), Software-as-a-Service (SaaS), and cloud-based value-added services in China, while also selling smart devices. Despite uncertainties in the global trade environment and ongoing supply chain pressures in the discretionary consumer electronics industry, the group demonstrated robust profitability and solid business growth in the first half of 2025. Total revenue reached USD 80.1 million, up 9.3% year-on-year, while net profit soared 302.4% to USD 12.6 million. Non-GAAP net profit was USD 20.1 million. Net cash from operating activities rose 53.8% to USD 18.2 million. As of June 30, 2025, cash, cash equivalents, and short- and long-term investments (including fixed-term deposits and treasury bonds) totaled USD 1.0063 billion.

By business segment, PaaS revenue was USD 58.1 million, up 7%, driven by growing demand and the group¡¦s strategic focus on customer needs and product enhancements. SaaS and other revenue reached USD 11.1 million, up 15.6%, primarily due to increased revenue from cloud software products and the group¡¦s continued commitment to delivering high-value-added services and diversified software offerings. Smart solutions revenue grew 16.7% to USD 10.9 million, fueled by rising customer demand for smart devices with integrated intelligent software features beyond IoT capabilities.The group¡¦s overall gross margin improved to 48.4%, up 0.4 percentage points year-on-year, with PaaS gross margin rising 1.1 percentage points to 48.7%. Operating profit margin was 1.4%, a significant 15.5 percentage point improvement from a negative 14.1% in Q2 2024. Non-GAAP operating profit margin reached 10.7%, up 0.7 percentage points. Net profit margin was 15.7%, improved by 11.4 percentage points, while non-GAAP net profit margin stood at 25.1%. Looking ahead, as businesses and consumers globally explore and accelerate the adoption of AI technologies and hardware, Tuya plans to continuously iterate and enhance its products and services, strengthen its software and hardware capabilities¡Xparticularly in AI¡Xand expand its core customer base. The group will invest in innovation and new opportunities, diversify revenue streams, and further optimize operational efficiency. (I do hold the mentioned stock.)

Strategy¡G

Buy-in Price: $21.50, Target Price: $24.00, Cut Loss Price: $20.00

|

MARKETINGFORCE(2556)

Analysis¡G

China¡¦s marketing and sales SaaS market is experiencing rapid growth, with Frost & Sullivan forecasting that the market size will reach RMB 74.5 billion by 2027, achieving a five-year compound annual growth rate (CAGR) of nearly 30%. In 2022, the market penetration rate was only 1.3%, indicating significant room for expansion compared to the mature U.S. market. Driven by core corporate demands for digital transformation, cost reduction, and efficiency improvement¡Xcoupled with AI technology lowering the barriers to SaaS adoption¡Xthe industry¡¦s growth prospects remain strong. As a leading domestic player, the company is well-positioned to fully benefit from this industry expansion. Marketingforce delivered a robust performance in the first half of this year, with total revenue increasing by 26% year-on-year to RMB 928 million. This growth was supported by stable artificial intelligence and Software-as-a-Service (SaaS) operations, a 25% rise in precision marketing services, and a contribution of RMB 110 million from new businesses (namely AI agent and integrated equipment).

Strategy¡G

Buy-in Price: $62.00, Target Price: $68.20, Cut Loss Price: $56.00

|

|

Alibaba (09988.HK) - Increased Investment in Flash Sales Weighs on Short-Term Profits

Company backgroundThe company provides technological infrastructure and marketing platforms, operating seven business segments. The China Commerce segment includes retail commerce businesses such as Taobao, Tmall, and Hema, as well as wholesale businesses. The International Commerce segment comprises international retail and wholesale commerce businesses, including Lazada and AliExpress. The Local Services segment includes location-based businesses such as Ele.me, Amap, and Fliggy. The Cainiao segment covers domestic and international end-to-end logistics services and supply chain management solutions. The Cloud segment offers public and hybrid cloud services to enterprises both in China and internationally, including Alibaba Cloud and DingTalk. The Digital Media and Entertainment segment includes platforms such as Youku, Quark, and Alibaba Pictures, along with other content and distribution platforms, as well as online gaming businesses. The Innovation Initiatives and Others segment encompasses Damo Academy, Tmall Genie, and other businesses. Financial performanceFor FY2025Q4, the company achieved total revenue of RMB 236.5 billion, a year-on-year increase of 6.6%; operating profit was RMB 28.5 billion, up 92.8% year-on-year; adjusted EBITA reached RMB 32.6 billion, an increase of 36.1% year-on-year; adjusted net profit was RMB 29.8 billion, rising 22.2% year-on-year.

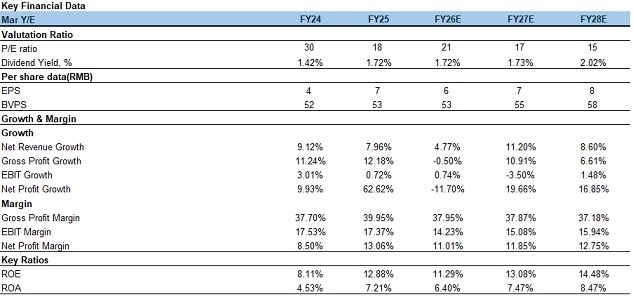

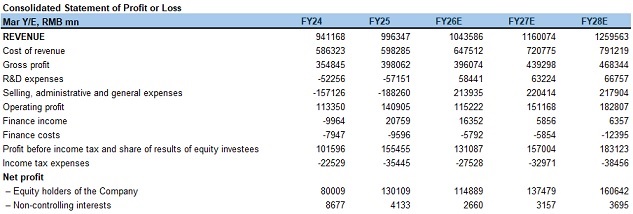

For full Year FY2025, the company reported total revenue of RMB 996.3 billion, a year-on-year increase of 5.9%; operating profit was RMB 140.9 billion, up 24.3% year-on-year; adjusted EBITA amounted to RMB 173.1 billion, growing 4.9% year-on-year, primarily driven by revenue growth and improved operational efficiency, partially offset by increased investments in e-commerce and technology sectors. Adjusted net profit was RMB 158.1 billion, remaining stable year-on-year.

By revenue type, Taotian Group revenue reached RMB 449.8 billion, up 3.4% year-on-year, accounting for 45.1% of total revenue. Alibaba International Digital Commerce Group revenue was RMB 132.3 billion, an increase of 28.9% year-on-year, representing 13.3% of total revenue. Cloud Intelligence Group revenue amounted to RMB 118.0 billion, growing 11.0% year-on-year, accounting for 11.8% of total revenue. Local Services Group revenue reached RMB 66.9 billion, up 12.2% year-on-year, representing 6.7% of total revenue. Taobao and Tmall Group: GMV demonstrated steady growth and monetization rate improved, but increased investment in flash sales weighed on profitsDriven by national policies to expand domestic demand and boost consumption, coupled with the platform's continued efforts to enhance price competitiveness and optimize the consumer experience, we expect Taotian Group's GMV growth in FY2026Q1 to accelerate compared to the previous quarter. The deeper application of site-wide promotion tools, along with the additional 0.6% basic software service fee introduced by Taobao since September 2024, collectively contributed to a year-on-year improvement in Taotian Group's overall monetization rate. As a result, we anticipate that customer management revenue will increase by 7.7% year-on-year in FY2026, reaching RMB 347 billion.

However, substantial investments in flash sales are putting pressure on short-term profits. On July 2, 2025, Taobao Flash Sales announced that it would provide direct subsidies totaling RMB 50 billion to merchants and consumers over the next 12 months. The initiative yielded significant results shortly after its launch¡Xon July 7, daily orders for Taobao Flash Sales combined with Ele.me exceeded 80 million (compared to just over 60 million on June 23 of the same year), with non-food orders surpassing 13 million and daily active users exceeding 200 million.

Despite the rapid growth in daily order volume for Taobao Flash Sales and Ele.me, the overall subsidy level remains high, leading to short-term profit pressure on Taotian Group. We project that Taotian Group's adjusted EBITA will decrease by 14.2% year-on-year to RMB 148.5 billion in FY2026, with the corresponding adjusted EBITA margin declining from 17.4% to 14.2%. Cloud Intelligence Group: AI Continues to Drive Cloud Revenue GrowthWe forecast that Cloud Intelligence Group's revenue will increase by 22.1% year-on-year to RMB 144.1 billion in FY2026. We believe that the trend of AI democratization driven by DeepSeek will continue to boost overall model training and application demand, further accelerating the growth of cloud service demand and revenue. The company's strategic focus is clearly directed toward public cloud, and by proactively scaling back low-margin businesses while continuously optimizing its revenue structure, it has effectively mitigated, to some extent, the profit pressure caused by price reductions in public cloud products. As a result, we expect Cloud Intelligence Group's adjusted EBITA to reach RMB 13.2 billion in FY2026, with an adjusted EBITA margin of 9.2%. Company valuationFlash sales order volume is expected to continue growing and is likely to drive increased traffic to the core e-commerce platform. Going forward, it will be essential to closely monitor the stability of the business's fulfillment capabilities and the growth of merchant supply. Accordingly, we project the company's FY26-28 operating revenue to be RMB 1,044 billion / 1,160 billion / 1,260 billion, with adjusted net profit of RMB 138 billion / 158 billion / 185 billion, corresponding to EPS of RMB 6.02 / 7.21 / 8.42. Given the company's high growth potential, we applied a SOTP valuation method and derived a target price of HKD 144. The current stock price implies FY2026-2028 P/E ratios of 21x / 17x / 15x. We assign an "Accumulate" rating. Risk factors1) Intensifying competition;

2) Intensified trade friction;

3) Deteriorated market demand. Financials

(Current Price as of: Aug 25 2025)

Exchange rate: HKD/RMB = 0.91Source¡G PSHK Est. Download PDF Version Here...

| Recommendation on 28-8-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 124.500 | | Suggested purchase price | N/A | | Target Price | $ 144.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|