Company Profile

After nearly 20+ years of organic development and inorganic acquisitions, the Company has established a "dual engine" growth strategy driven by the application of lightweight metal materials in auto parts industry and the general aviation aircraft manufacturing industry, including six major business sectors, namely, 1) aluminum alloy wheels, 2) magnesium alloy automobile die castings, 3) environmentally friendly dacromet coatings, 4) general aviation aircraft. The Company is leading in many sub-industry fields.

Investment Summary

Wuxi Xiongwei's Deconsolidation Affected Revenue, While Impairment in the General Aviation Business Impacted Profitability

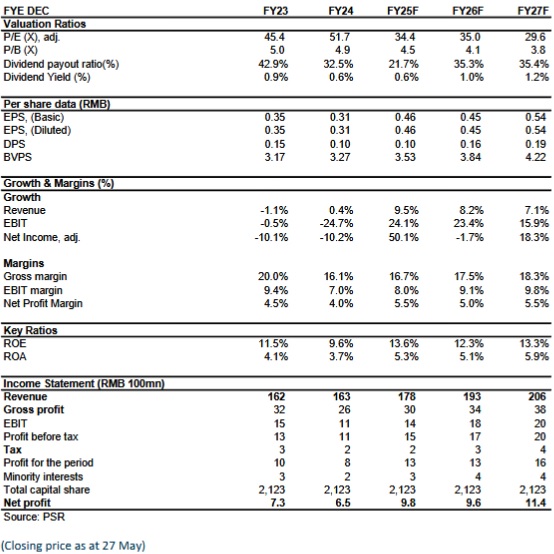

Due to the divestiture of Wuxi Xiongwei (high-strength steel stamping parts and other metal casting businesses), Wanfeng Auto Wheel achieved revenue of RMB16,264 million (RMB, the same below) in 2024, up only 0.35% yoy. Affected by asset impairments and goodwill impairments, net profit attributable to the parent company declined 10.14% yoy to RMB653 million. Earnings per share (EPS) were RMB0.32, down 8.6% yoy. The Company plans to distribute a cash dividend of RMB0.1 per share, with a payout ratio of 31.25%.

By business segment, the automotive metal parts lightweight business generated revenue of RMB13.45 billion, up 0.09% yoy, accounting for 82.7% of total revenue, down slightly by 0.21 percentage points. Revenue from new energy vehicle (NEV) supporting business was RMB3.28 billion. The general aviation aircraft business achieved revenue of RMB2,814 million, up 1.62% yoy. By region, domestic sales reached RMB8.3 billion, up 8.75% yoy, accounting for 51.04% of revenue, an increase of 3.94 percentage points; overseas sales were RMB7.96 billion, down 7.12% yoy, accounting for 48.96%.

Due to intense market competition and changes in the international environment, overall profitability was suppressed. The Company's gross margin in 2024 declined 3.8 percentage points yoy to 16.53%. Specifically, the gross margin of the automotive metal parts lightweight business decreased 3.5 percentage points yoy to 14.82%; the general aviation aircraft business's gross margin dropped 5.34 percentage points yoy to 24.71%. The decline in the general aviation business was mainly caused by supply chain issues affecting aircraft delivery. Based on a conservative principle, the Company made impairment provisions on certain orders, resulting in a 54.29% yoy decline in profit contribution from this segment. Additionally, the magnesium alloy die-casting parts business saw net profit drop 47.91% yoy due to rising raw material and fuel prices. However, the aluminium alloy wheels business performed well, partially offsetting the negative factors. In 2024, the Company's automotive aluminium alloy wheels sales volume was 22,340.1 thousand sets, up 17.27% yoy. The Company maintained good expense control, with the full-year period expense ratio (sales + administration + R&D + finance) reduced by 1.84 percentage points yoy to 8.92%.

In Q1 2025, the Company achieved revenue of RMB3,567 million, up 0.75% yoy; net profit attributable to the parent company was RMB275 million, up 21.3% yoy. Net profit excluding non-recurring items was RMB190 million, down 12.8% yoy. This was mainly due to a RMB125 million gain from the subsidiary's acquisition of certain tangible assets, intellectual property rights, and specific contract rights and obligations from Volocopter GmbH in Q1, which led to RMB140 million yoy increase in non-operating income. Gross margin declined 1.5 percentage points yoy to 18.3%.

Acquisition of Volocopter Accelerates eVTOL Commercialisation, Low-Altitude Economy Growth Expected

In 2024, the low-altitude economy was incorporated into the government work report for the first time, establishing it as an important future growth engine. The Company has abundant orders for general aviation aircraft. The MPP series of special-purpose high value-added aircraft achieved good order delivery in 2024, with continuous optimisation of the customer structure. Breakthroughs were made in orders for MPP special-purpose high value-added aircraft, with sales continuously optimised.To accelerate the global layout in the low-altitude sector and develop advanced eVTOL products, the Company acquired the core assets of German eVTOL renowned enterprise Volocopter in March 2025. It will integrate Volocopter's cutting-edge eVTOL technologies (such as distributed electric propulsion systems and the VoloIQ aviation cloud platform) with Wanfeng's manufacturing expertise in general aviation to build a product matrix of ¡§fixed-wing + vertical takeoff and landing vehicles + drones¡¨. In 2025, the Company will advance the EASA (European Aviation Safety Agency) type certification process for special-purpose DART models, all-electric general aviation aircraft eDA40, and some eVTOL models (such as Volocopter 2X and VoloCity), striving to bring products to market as soon as possible. The VoloCity and Volocopter 2X models will focus on urban air mobility; the compound-wing models VoloRegion and VoloConnect will be used for intercity transport, forming a complementary system. Solutions for drone cargo scenarios will rely on the VoloDrone model, capable of carrying up to 200 kilograms of cargo within a 40-kilometre range.

We believe the current low-altitude economy industry has moved from ¡§concept incubation¡¨ to ¡§scale application¡¨. It is expected that China's low-altitude economy scale will exceed RMB1 trillion by 2026, and the global low-altitude economy scale will exceed USD1 trillion by 2040. As one of the leaders in complete aircraft manufacturing, eVTOL is expected to become a new growth engine for the Company's business.

Investment Thesis:

We expect the Company's automotive metal parts lightweight business to achieve steady growth by leveraging the development dividends of the NEV industry, while general aviation and eVTOL businesses benefit from the rising low-altitude economy trend, offering promising prospects.

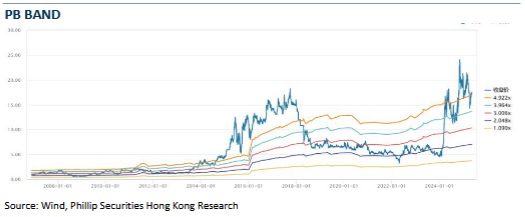

According to the latest financial data, we adjusted the EPS forecast for 2025 and 2027 to RMB 0.46/0.45/0.54, respectively. We give the Company's target price to RMB 18.17, respectively 39.4/40/33.8 x P/E, 5.2/4.7/4.3 x P/B for 2025/2026/2027, a "Accumulate" rating. (Closing price as at 27 May)

Risk

Price war among peers

Raw material price increase

New business risk

Financials

Click Here for PDF format...