Company Profile

Minth Group is a world-renowned supplier engaged in the design, manufacturing and sales of automotive interior and exterior trim and body structure parts. The domestic market share of its core products exceeds 30%. The company has production bases in China, the United States, Mexico, Thailand, Germany, Serbia and other countries, and its customers cover major vehicle companies in the market. Based on a variety of new materials and surface treatment technologies, in recent years the company has developed new electrified and smart product lines such as aluminum power battery boxes and smart front faces, forming a series of competitive terminal products.

Investment Summary

Result Grew Over 20% in 2024, Gross Margin Improved

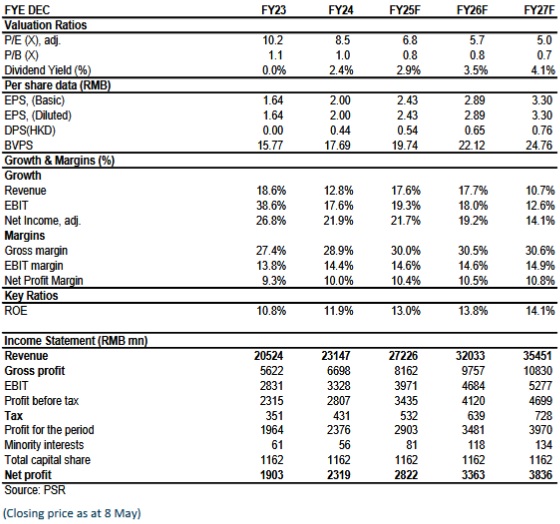

In 2024, Minth Group reported total revenue of RMB23.15 billion (RMB, the same below), up 12.8% yoy; net profit attributable to the parent company was RMB2.32 billion, up 21.9% yoy. This was mainly attributable to the scale effect from increased turnover, the continued improvement in capacity utilisation of the battery house product line, and cost reduction and efficiency enhancement measures across various product lines, which led to a yoy increase in gross profit compared to 2023, enabling the Company to maintain a sound overall level of profitability.

During the period, the gross margin was approximately 28.9%, up 1.5 ppts yoy. It was mainly driven by the increase in segment margin of plastic products and battery house by 1.1 ppts and 2.1 ppts, respectively. Specifically, the segment gross margin of the battery house business reached 21.4%, one step closer to the 25% target.

The Company's selling/administration/R&D expense ratios were up 0.6 ppts, flat, and down 0.5 ppts yoy, respectively, to 4.5%, 7.1%, and 6.3%. This was mainly due to increased transportation costs caused by the Red Sea incident, higher expenses from the growth in international business volume, and continued R&D investment in innovative products and new material technologies, which were diluted by revenue growth. The increase in gross margin offset the rise in period expense ratio, resulting in a 0.7 ppts yoy increase in net profit margin to 10.0%.

International Business Continued to Outpace Domestic Business Growth

Among the regions, revenue from China was approximately RMB9.32 billion, up about 1.3% yoy, mainly driven by the growth in the battery house business and Chinese brand business, but partially offset by sluggish sales of joint-venture brands. International revenue was approximately RMB13.82 billion, up about 22.1% yoy, with its share of total revenue increasing by 4.5 ppts from 55.15% in 2023 to 59.72%. This was primarily attributable to the rapid growth of the battery house business and the improvement in traditional product businesses in North America and the Asia-Pacific region.

The Company continued to optimise the operational efficiency of its global factories, strengthened the vertical integration capabilities of manufacturing processes at each site, and established benchmark factories while promoting their management models. For example, with the comprehensive capabilities of factories in Mexico and Thailand having significantly improved and stabilised, the Company has leveraged the advantageous resources of North America, Thailand, and China to reduce local operating costs in North America. It is worth noting that the Company has continued to improve the localisation rate of production in North America and Europe, thereby keeping the impact and uncertainties arising from tariffs and geopolitical factors within a controllable range and enhancing the competitiveness of its products in those regions.

Battery Box, Body and Chassis Structural Parts, and Smart Exterior Parts Businesses Maintained Rapid Growth

During the review period, the Company's plastic parts, metal and trims, battery house, and aluminium parts businesses recorded revenues of RMB5.86 billion, RMB5.49 billion, RMB5.34 billion, and RMB4.92 billion, respectively, representing yoy changes of +4.3%, 0%, +51%, and +14%. Their respective shares of total revenue changed by -2.1 ppts, -2.9 ppts, +5.8 ppts, and +0.2 ppts yoy, to 25.3%, 23.7%, 23.1%, and 21.1%.

The profit margins of the four major business segments were 25.1%, 27.8%, 21.4%, and 33.1%, representing yoy changes of +1.1 ppts, +1.3 ppts, -2.1 ppts, and -4.2 ppts, respectively. The battery house business secured new orders from Changan and Volkswagen Anhui domestically, and from Hyundai-Kia in Europe, Ford in North America, and Toyota in Japan. In the field of body and chassis structural parts, the Company made its first breakthroughs in the subframe, motor controller housing, and motor housing businesses. In the smart exterior parts business, the Company gained recognition and cooperation from Huawei, Geely, and BYD, further expanding its product portfolio and market share. As several new production lines continue to ramp up rapidly, the gross margin of emerging businesses is expected to continue benefiting from economies of scale, driving Minth's overall gross margin back up to the 30% level.

Exploring New Tracks Expected to Create a Second Growth Curve

The Company is actively exploring new tracks and has made forward-looking deployments in wireless charging for electric vehicles, bionic robots, and low-altitude aircraft (eVTOL), including core components such as electronic skin, smart visors, integrated joints, fuselages, and rotors. Small-batch sample deliveries were completed within the year, and cooperation agreements were reached with several leading enterprises.

1) Humanoid Robots: including smart exterior parts and electronic skin, integrated joint assemblies, robotic limb structural components, and wireless charging for robots. The robot products are currently at the sample delivery stage to customers and are expected to contribute to revenue in 2027.

2) Core Components of Low-Altitude Aircraft: including fuselage systems and rotor systems. Minth Group has established cooperation with several leading low-altitude flight enterprises, including Zhuimeng Kongtian and ZEROG.

3) Wireless Charging Systems for Vehicles: including ground-side modules, vehicle-side modules, and cooling system solutions. With the rapid development of robotaxis and autonomous driving, the wireless charging industry is expected to experience explosive growth in 2026. The cultivation of new tracks and expansion into new markets are expected to create a second growth curve, driving the Company's sustainable development in the medium to long term.

Improved Cash Flow, Share Buyback and Dividend Resumption Reflect Management's Confidence

Capital expenditure this year decreased significantly by 40.9% yoy to RMB1.91 billion. After several years of peak investment in capacity expansion, particularly in the deployment of overseas factories, the Company has largely passed the high-investment phase and is expected to focus future spending mainly on equipment upgrades and flexible transformation. The Company's cash flow also improved, leading to the resumption of dividend payments after a one-year suspension and share buyback, signalling the management's confidence in the Company's future development.

Valuation

We revised the expected EPS for 2025/2026 to 2.43/2.89¡]from 2.35/2.78¡^yuan, and introduce 2027 EPS forecast at 3.30yuan.We believe that it is reasonable to give the Company a valuation of 10.3/8.6/7.6x P/E and 1.3/1.1/1.0x P/B for 2025/2026/2027, equivalent to target price of HK$ 27.8 and BUY rating. (Closing price as at 8 May)

Financials

Click Here for PDF format...