Financial performance

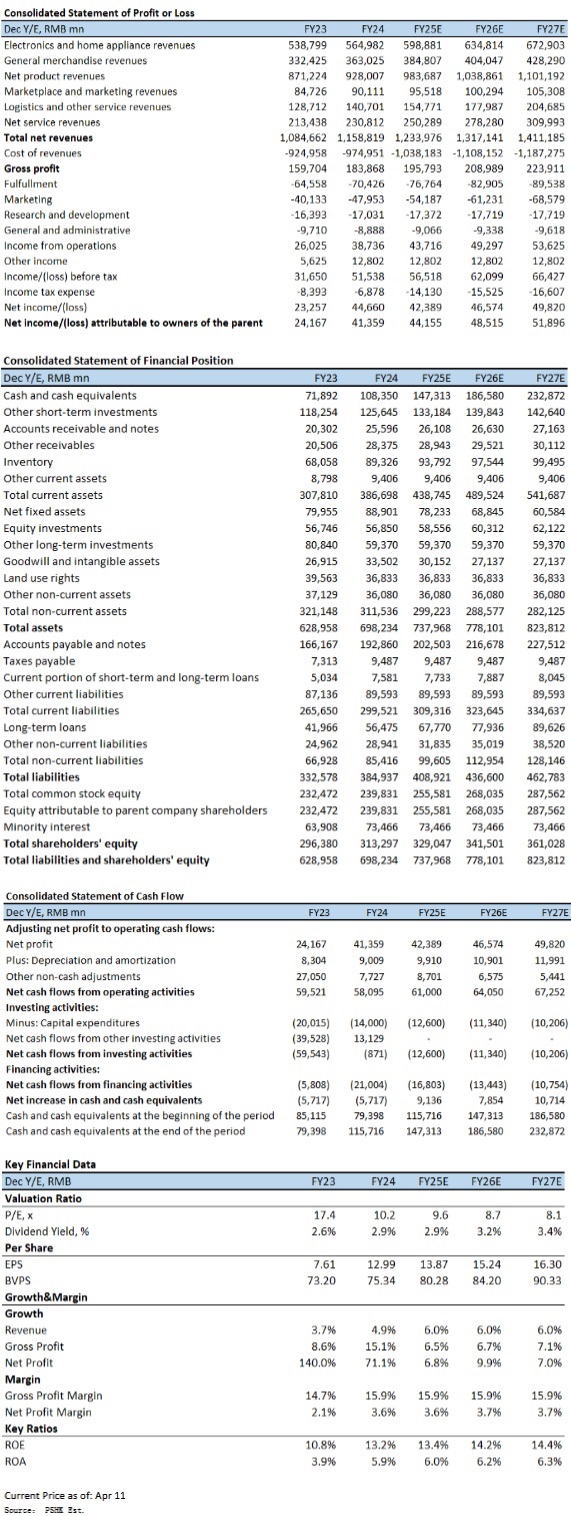

In Q4 2024, the company's revenue rebounded to double-digit growth, rising 13.4% YoY to CNY 347 billion, driven mainly by strong product revenue growth. Product sales (1P) increased 14.0% YoY to CNY 281.0 billion, while service revenue (3P) grew 10.8% to CNY 66.0 billion. By segment, JD Retail revenue climbed 14.7% to CNY 307.1 billion, JD Logistics revenue rose 10.4% to CNY 52.1 billion, and New Business revenue declined 31.0% to CNY 4.7 billion. Operating profit surged 319.3% YoY to CNY 8.5 billion, with a 2.4% margin, while Non-GAAP net profit attributable to shareholders jumped 34.2% to CNY 11.3 billion.

For full-year 2024, total revenue reached CNY 1,158.8 billion (+6.8% YoY), operating profit grew 48.8% to CNY 38.7 billion (3.3% margin), and Non-GAAP net profit rose 35.9% to CNY 47.8 billion. The company enhanced shareholder returns, raising dividends to 1.5 billion and 3.6 billion in shares, achieving a record 7.6% total shareholder return ratio.

Performance summary

JD Retail

In Q4 2024, JD Retail (including JD Health, JD Industry, and other components) reported revenue of CNY 307.1 billion, up 14.7% YoY, with an operating profit of CNY 10.0 billion and an operating profit margin (excluding unallocated items) of 3.3%, an increase of 2.6 percentage points YoY. Product revenue rose 14.0% YoY to CNY 281.0 billion, with both electronics & home appliances and general merchandise categories achieving double-digit growth. Electronics and home appliance sales reached CNY 174.1 billion (+15.8% YoY), while daily necessities revenue grew 11.1%. Service revenue increased 10.8% to CNY 66.0 billion, with platform and advertising service revenue up 12.7%.

On the product revenue (1P) side, according to China's National Bureau of Statistics, total retail sales of consumer goods in 2024 reached CNY 48.8 trillion (+3.5% YoY), while online retail sales grew 7.2% to CNY 15.5 trillion. Within this, online sales of physical goods rose 6.5% to CNY 13.08 trillion, accounting for 26.8% of total retail sales¡Xoutpacing overall consumption growth and reflecting steady recovery.

For service revenue (3P), JD continued to enhance its third-party merchant ecosystem and strengthen user engagement, with both quarterly active users and purchase frequency maintaining double-digit YoY growth in Q4 2024. The company also expanded its 3P ecosystem¡Xin January 2025, JD announced a major upgrade to its PLUS membership program, introducing a "Lifestyle Services Package" (allowing members to redeem seven premium services with points), a new Á¡-Day No-Questions-Asked Replacement" policy (covering appliances and 3C products), and an expanded "Unlimited Free Shipping" benefit (now including instant-delivery services).

On the user experience front, JD has revamped its search and recommendation systems using AI, improving search satisfaction and traffic distribution efficiency. For consumers, the company introduced an AI shopping assistant and AI digital avatars to provide comprehensive product information and professional advice, reducing the time and effort required to find and select products. For merchants, JD rolled out a suite of AI-powered tools covering product listings, order management, after-sales service, customer support, and data analytics to enhance operational efficiency and reduce costs.

Given that JD Retail's business adjustments have shown initial success and continue to benefit from China's "trade-in" policy, but factoring in the high base effect in the second half of 2024, we estimate JD Retail's segment valuation at CNY 444.0 billion based on a 12.0x forward 2025 P/E ratio.

JD Logistics

In 2024, JD Logistics reported revenue of CNY 182.8 billion, up 9.7% YoY. Revenue from external clients reached CNY 127.8 billion (+9.6% YoY), accounting for nearly 70% of total revenue, with over 80,000 external integrated supply chain customers served. Thanks to continuous operational refinement, JD Logistics achieved an adjusted net profit of CNY 7.9 billion, surging 186.8% YoY.

JD Health

JD Health's 2024 revenue grew 8.6% YoY to CNY 58.2 billion, with gross profit up 12.2% to CNY 13.3 billion. Operating profit jumped 132.9% YoY to CNY 1.47 billion, while adjusted operating profit rose 4.9% to CNY 2.6 billion.

New Business

In Q4 2024, revenue from new businesses declined 31.0% YoY, mainly due to JD Xi's transition from a self-operated to a semi-hosted model. Dada's net revenue fell 11.6% YoY to CNY 2.4 billion, with JD Instant Delivery revenue plunging 52.4% to CNY 700 million. However, Dada Now's revenue surged 40.8% to CNY 1.7 billion, driven by increased orders from chain merchants for intra-city delivery services. The segment reported a net loss of CNY 1.2 billion, slightly narrower than the previous year.

Company valuation

In 2025, JD.com will further enhance supply chain efficiency across its core product categories to unlock additional profit growth potential. Based on the industry-average 12.0x forward 2025 P/E ratio, we have raised our revenue forecasts to CNY 1,234bn/1,317.1bn/1,411.2bn for 2025-2027, with projected net profits of CNY 44.2bn/48.5bn/51.9bn and corresponding EPS of CNY 13.9/15.2/16.3, implying current P/E multiples of 10.7x/9.8x/9.1x. Our sum-of-the-parts valuation, incorporating a 30% holding discount to JD's subsidiaries and investments, yields a target market cap of CNY 585.1bn for JD Group in 2025, equivalent to a target price of CNY 183.8 (HKD200.3) per share, and we maintain our "Buy" rating on the stock.

Risk factors

1) The monetization capabilities of the platform ecosystem may not meet expectations; 2) increased competition in the retail and logistics industries; 3) consumer demand may recover weaker than expected.

Financials

Click Here for PDF format...