Sectors:

Air & Automobiles (Zhang Jing),

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

Utilities, Commodity, Shipping (Margaret Li)

TMT, Semiconductors (Megan Tao)

Automobile & Air (Zhang Jing)

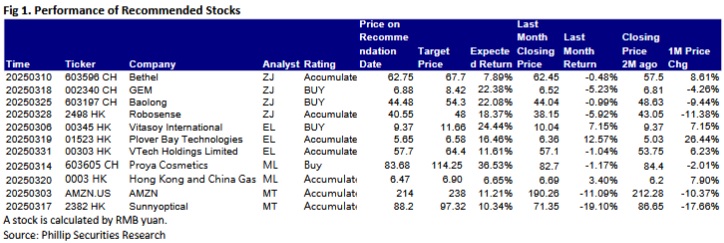

This month I released 2 initiation report of GEM (002340.CH) and RoboSense (2498.HK), and 2 updated reports of Bethel (603596.CH) and Baolong (603197.CH). Among which, we prefer Robosense and Baolong.

RoboSense is a leading global company in the field of LiDAR and perception solutions. Its main products currently include three categories: robot LiDAR, automotive LiDAR, and solutions. Benefiting from the increasing penetration of intelligent vehicles, the market size of automotive LiDAR is expected to continue to grow exponentially, with the industry competition following a "four-player competition" pattern. As the market penetration of LiDAR increases, the Company is seeing the release of scale effects, with its losses significantly narrowing. The Company is currently upgrading its strategy from a "vehicle sensor supplier" to a "robot perception system platform," and breakthroughs in overseas markets are also helping to unlock performance growth potential.

With automakers like BYD, Li Auto, and XPeng Motors integrating LiDAR into vehicles priced between RMB150,000 and RMB200,000, the penetration rate is expanding from the high-end market to the mainstream market, driving robust industry growth.

According to the positive profit warning announcement issued by the Company on February 24, 2025, the total revenue for 2024 is expected to reach RMB1.63 billion to RMB1.67 billion, a yoy increase of 45.5% to 49.1%, with net losses narrowing by 88% to 90%, estimated at RMB430 million to RMB520 million. This performance validates the Company's continuing release of scale effects amid the increased market penetration of LiDAR technology and the significant narrowing of losses.

In January 2025, the Company delivered its 1 millionth LiDAR unit (E1R) to humanoid robot enterprises and held the ¡§Hello Robot¡¨ event, where it launched three new types of robot vision products: EM4 (ultra-long-range digital radar), E1R (robot fully solid-state digital LiDAR), and Airy (hemispherical digital LiDAR). The Company also released robot vision solutions like ActiveCamera and key robot components such as the second-generation dexterous hand, FS-3D force sensor, and DC-G1 domain controller, marking the Company's strategic upgrade from a "vehicle sensor supplier" to a "robot perception system platform." As of November 2024, the Company has established partnerships with over 2,600 robotics companies, and it is expected that robot shipments will surpass 100 thousand units in 2025, potentially becoming the second growth curve after ADAS.

In March 2025, Mercedes-Benz announced plans to equip global vehicle models with RoboSense LiDAR. This marks the first time Chinese LiDAR technology has entered the supply chain of a top international automaker. The Company has already secured agreements with four overseas OEMs (original equipment manufacturers). In the long run, breakthroughs in overseas markets will open up significant growth potential for the Company's performance.

According to a report by China Insights Consultancy, the global robot LiDAR market is expected to grow from RMB8.2 billion in 2022 to RMB216.2 billion by 2030, equivalent to a CAGR of 50.6%. China is projected to become the largest market by 2030, accounting for about 31.8% of the global market, nearing RMB70 billion.

As a leading player in automotive-grade LiDAR, the Company has passed stringent automotive-grade certification, giving it a quality advantage and cost advantages from large-scale production. As the leader in automotive-grade LiDAR, the Company is expected to continue expanding its market share in the robotics sector. Its accelerated entry into the robotics industry will unlock a new growth point for the Company's performance.

As for valuation, we expected diluted SPS (Sales Per Share) of Robosense to RMB 3.61/5.55/8.45 of 2024/2025/2026, considering the explosive potential of its robot business, we gave the target price to HKD 48, respectively 12.5/8/5.2x P/S for 2024/2025/2026.

Shanghai Baolong Automotive Corporation(Baolong or the "Company") started with tire valves. Later, following the automobile development trend, the Company continuously expanded the product line, and successively engaged in wheel weights, exhaust pipes, lightweight structural parts, TPMS (tire pressure monitoring system), as well as the intelligent automotive field of sensors, ADAS (that is, advanced driver assistance systems, mainly based on vision products and millimeter-wave radars), and air suspension. After more than 20 years of development, the Company is at the forefront of the segment in terms of the market share of its traditional business, namely, tire valves, wheel weights, exhaust pipes, and TPMS, which is currently the main source of revenue and profit. The Company's emerging business covers intelligent drive solutions-related parts and hydraulic lightweight structural parts, such as sensors, air suspension, and ADAS. The emerging business is currently the core direction of the Company's vigorous development, and will be an important growth point for future revenue and profit.

From a medium- to long-term perspective, the Company's traditional business is expected to maintain steady growth. The Company's emerging business, benefiting from forward-looking layouts and accumulated competitive advantages, is likely to usher in a new high-growth cycle..

As analyzed above, we expected diluted EPS of the Company to RMB 1.26/1.88/2.44 of 2024/2025/2026. And we accordingly gave the target price to 54.3, respectively 28.8/20/15x P/E for 2024/2025/2026.

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

This month I released reports of Vitasoy International (00345.HK), Plover Bay Technologies (01523.HK) & VTech Holdings Limited (00303.HK).

VTech Holdings Limited (00303.HK) reported revenue of USD 1.09 billion for the first half of the 2025 fiscal year (six months ended September 2024), a yoy decline of 4.5%. Despite an improvement in gross margin to 31.5% (compared to 28.5% in the previous year), net profit attributable to shareholders dropped by 6.6% to USD 87.4 million due to lower revenue and higher operating expenses associated with the Gigaset acquisition. Basic earnings per share (EPS) decreased by 6.5% to USD 0.346. The interim dividend was maintained at USD 0.17 per share, reflecting management's confidence in the company's stable cash flow.

Total revenue for the first half of the fiscal year was USD 1.09 billion, down 4.5% yoy. The decline was primarily driven by weaker demand in the North American, European, and Asia-Pacific markets, where revenues decreased by 7.4%, 1.4%, and 7.1%, respectively. North America's revenue fell to USD 453.1 million, Europe's revenue reached USD 462.1 million, and Asia-Pacific revenue stood at USD 159.4 million. In contrast, revenue from other regions, including Latin America, the Middle East, and Africa, surged by 33.6% to USD 15.1 million, though these regions remain a small portion of overall sales.

Gross margin increased from 28.5% to 31.5%, mainly benefiting from lower material costs, improved product mix, and contributions from the Gigaset acquisition. Despite the margin expansion, the ongoing integration of Gigaset led to higher operating expenses, resulting in a 5.5% decline in operating profit to USD 104.2 million, with an operating margin of 9.6%, down from 9.7% in the previous year. Net profit attributable to shareholders decreased by 6.6% to USD 87.4 million

VTech's profitability has improved, but revenue growth remains a challenge. The integration of Gigaset is progressing well and is expected to provide long-term growth momentum. However, weak demand in CMS and macroeconomic uncertainties pose near-term risks, we forecast the company's earnings per share (EPS) for FY2025 and FY2026 to be 0.77 and 0.81 USD, respectively. Our target price is set at HK$64.40, corresponding to a 10.7x forward P/E ratio for FY2025, which is in line with the company's five-year historical average valuation. Our investment rating is ¡§Accumulate¡¨.

Utilities, Commodity, Shipping (Margaret Li)

This month I released reports of Proya Cosmetics (603605.CH) & Hong Kong and China Gas (0003.HK).

As a leading domestic cosmetics company, Proya Cosmetics primarily engages in R&D, production, and sales of cosmetic products. Its offerings span skincare, makeup, cleansing &personal care, and more. The company owns brands such as Proya, Hapsode, Timage, Off&Relax, CORRECTORS, INSBAHA, UZERO and Anya.

In the first three quarters of 2024, the company achieved revenue of RMB 6.97 billion with a yoy increase of 32.7%, driven by growth in online channel sales and steady expansion of smaller brands. Net profit attributable to shareholders reached RMB 1.00 billion with a yoy increase of 34.0%. Gross profit margin stood at 70.1% with a yoy decrease of 1.1 percentage points, primarily due to rising operating costs from increased promotional activities and full-scale deployment on Douyin. Benefiting from a yoy decline of 57.53% in asset impairment losses, the net profit margin remained stable at 14.7%. Net cash flow from operating activities was RMB 400 million with a sharp yoy decrease of 49.4%, due to earlier payments for major promotions and increased inventory payments. EPS rose to RMB 2.53 with a yoy increase of 35.3%.

The Chinese cosmetics market has continued to grow in recent years. The main driving forces are the increase in cosmetics consumption, the increasing recognition of domestic products among young people, and the expansion of online channels (such as live streaming e-commerce). The Chinese cosmetics market has huge growth potential. With its popular strategies such as "Morning C and Evening A", PROYA has successfully established an image of technological skin care. The main brand "PROYA" contributes nearly 80% of the revenue, and at the same time, it incubates the cosmetics brand "Timage" (with impressive growth rate) and cleansing brand ¡§Off&Relax¡¨. Net operating cash flow matches net profit, and there is no significant debt repayment pressure (the debt-to-asset ratio is maintained below 40%). PROYA has strong product innovation and pipeline operation capabilities in the domestic beauty market, with a high degree of certainty in short-term performance growth. It firmly holds the leading position in the domestic beauty market. We are optimistic about PROYA's overseas opportunities in the future. The company is expected to expand into new markets in Southeast Asia and achieve breakthroughs in revenue. We forecast that the company's operating income will be RMB 10.95 billion, RMB 12.98 billion and RMB 14.83 billion in 2024-2026, with EPS of RMB 3.85/4.57/5.29, corresponding to a price-earnings ratio (P/E) of 21.7x/18.3x/15.8x. We give the company a P/E of 25 times in 2025, a target price of RMB 114.25, and give it a "buy" rating for the first time. (Current price as of March 10)

Hong Kong and China Gas (0003.HK) was established in 1862. The company is the only gas supplier in Hong Kong and one of the largest energy suppliers locally. The company started its gas business in mainland China in 1994. Currently, it has more than 900 projects in mainland China, including renewable energy solutions (such as solar photovoltaic systems), urban pipeline gas, upstream, midstream, water supply, urban waste resource utilization, emerging environmentally friendly energy, etc., and its business covers 29 provincial regions across the country. The company is actively developing clean energy covering sea, land and air, including hydrogen for vehicles, green methanol for ships, and sustainable aviation fuel. Henderson Land Development Group is the company's major shareholder, and real estate tycoon Li Shau-kee is the actual controller. The company's subsidiary, TOWNGAS SMART ENERGY COMPANY LIMITED, was listed on the Hong Kong Stock Exchange in 2005 with the stock code 1083.HK.

In the first half of 2024, the company's revenue was HK$27.49 billion with a year-on-year decrease of 5.8%. The operating profit after tax was HK$3.89 billion with a year-on-year increase of 1.6%, of which: Hong Kong, China business was HK$2.01 billion with a year-on-year decrease of HK$100 million; Mainland Utility business was HK$1.53 billion, similar to the same period of last year; Renewable business was HK$110 million, achieving strong growth; Extended business was HK$190 million; Other business was HK$50 million, achieving profitability. Core operating profit was HK$3.19 billion with a year-on-year increase of 2.2%. Profits attributable to shareholders were HK$3.04 billion with a yoy decrease of 15.9%. EPS was HK$16.3 cents, with a yoy decrease of 16.0%. The Board of Directors announced a 2024 interim dividend of HK$0.12 per share. The main reason for the decline in the company's revenue is that the economic recovery in the Mainland and Hong Kong in the first half of 2024 did not meet expectations. The consumption enthusiasm of Hong Kong local citizens to the north of mainland led to a decrease in gas consumption in Hong Kong's catering and hotel industries, which in turn led to the failure to increase the sales of industrial and commercial gas. In addition, there were many high temperature days in the first half of the year and the strong exchange rate of Hong Kong dollar against RMB, which brought challenges to the company's business.

he company has both stability and growth potential, with dividends maintained at HK$0.35 per share for many years. We are optimistic about the growth of the company's mainland gas business and renewable energy business, we predict that the company's revenue will be HK$58.03 billion, HK$59.19 billion and HK$60.38 billion respectively in 2024-2026. EPS will be 0.35/0.38/0.39 HKD. BVPS will be 3.32/3.38/3.46, corresponding to the P/B of 1.95x/1.91x/1.87x. Based on the company's average PB of 2.04 times in the past three years, the company is given a P/B of 2.04 times in 2025, with a target price of HK$6.90, and our investment rating is " Accumulate ". (Current price as of Mar 17).

TMT, Semiconductors (Megan Tao)

In this month, I published two research reports on Amazon (AMZN.US) and Sunny optical (2382.HK).

Amazon was founded in 1995 and is an American multinational technology company engaged in providing online retail shopping services. It operates through the following segments: North America, International, and Amazon Web Services (AWS). The North America segment involves the retail sale of consumer products, including sales from sellers and subscriptions through online and physical stores focused on North America. It also includes export sales from online stores. The International segment focuses on consumer product retail revenue, including revenue from sellers and subscriptions through international online stores. The AWS segment includes the global sales of computing, storage, databases, and other services for startups, enterprises, government agencies, and academic institutions.

In 2024Q4, the company achieved net revenue of $187.8 billion, representing a 10.0% YoY growth. Operating profit rose to $21.2 billion (up 61.0% YoY), while net profit surged 88.0% YoY to $20.0 billion. By business segment, online stores generated $75.6 billion in net revenue (up 7.1% YoY), physical stores $5.6 billion (up 8.3% YoY), third-party retail $47.5 billion (up 9.0% YoY), advertising $17.3 billion (up 18.0% YoY), subscription services $11.5 billion (up 9.7% YoY), and AWS $28.8 billion (up 19.0% YoY). Regionally, international markets contributed $43.4 billion in net revenue (up 7.9% YoY), while North America accounted for $115.6 billion (up 9.5% YoY), with global paid units increasing 11.0% YoY due to competitive pricing, wide product selection, and fast shipping. Logistics efficiency improved significantly in Q4 due to better inventory management, increased units per package, and shorter shipping distances. Looking ahead to Q1 2025, the company forecasts net revenue between $151.0 billion and $155.5 billion and operating profit between $14.0 billion and $18.0 billion, both falling short of expectations due to unfavorable exchange rate fluctuations. Management also indicated that Q4's capital expenditure of $26.3 billion would be representative of 2025, with total capital expenditures projected to reach $105.0 billion for the year.

Given Amazon's strong position in both e-commerce and public cloud sectors, which are still in the early stages of long-term transformation, the company is well-positioned for future growth. Amazon has provided a significant competitive advantage to its retail business by enhancing the flexibility of its first-party and third-party inventory. Additionally, its first-mover advantage in cloud computing has enabled AWS to capture over 30% of the global market share. As a result, we forecast the company's operating revenue for 2025-2027 to be $698.5 billion, $772.3 billion, and $850.6 billion, respectively, with net profits of $71.9 billion, $85.1 billion, and $106.4 billion. This translates to EPS of $6.64, $7.80, and $9.66, respectively. The current stock price corresponds to a PE ratio of 32.3x, 27.5x, and 22.2x for the respective years.

Based on the DCF valuation method, we apply a 15x EV/EBITDA multiple for 2030 and assume a 10% discount rate, estimating the company's total target market capitalization at $2.58 trillion for 2025. This corresponds to a target price of $238, with a "Accumulate" rating.

Sunny Optical Technology, founded in 1984, is a leading global manufacturer of optical components and products. Specializing in optical and optoelectronic product design, R&D, production, and sales, its key offerings include optical components (mobile phone lenses, automotive lenses, surveillance lenses, etc.), optoelectronic products (mobile phone camera modules, 3D optoelectronic modules, automotive modules), and optical instruments (microscopes, smart inspection equipment).

The company has issued a positive profit alert for 2024, expecting full-year net profit to reach RMB 2.64¡V2.75 billion, marking a YoY growth of 140.0%¡V150.0%, slightly exceeding market expectations. This growth is primarily driven by the recovery of the global smartphone market, with shipments rising to 1.22 billion units, strong demand for high-end models, and AI integration in smartphone hardware, resulting in a 13.1% YoY increase in mobile phone lens shipments and improved product mix, boosting ASP and gross margins. Additionally, the development of intelligent driving assistance systems increased the adoption rate of automotive lenses, with the company's total automotive lens shipments reaching 102 million units, a 12.7% YoY increase, meeting the previous guidance.Considering the recovery in consumer electronics demand and the company's continued push towards high-end smartphone products, which is expected to optimize product portfolio, coupled with the growth in automotive products driven by the penetration of intelligent driving, we anticipate revenue growth. Therefore, we forecast the company's revenue for 2024-2026 to be 36.51/42.54/48.19 billion RMB, with net profits attributable to the parent company of 2.43/3.19/3.94 billion RMB, corresponding to EPS of 2.28/3.02/3.72 RMB. The current stock price corresponds to a PE ratio of 36.0/27.2/22.0x. Overall, given the company's solid leading position, we apply a valuation slightly above the industry average, at 30 times the 2025 PE, resulting in a target price of 97.32 HKD per share. We initiate coverage with an "Accumulate" rating.

Click Here for PDF format...