Financial performance

In the fourth quarter of 2024, the company achieved total revenue of RMB 12.8 billion, reflecting a 23.4% YoY growth, though it declined sequentially due to seasonal factors. Non-GAAP net profit reached RMB 3.0 billion, up 13.6% YoY, with a net profit margin of 23.8%, down 2 percentage points YoY, mainly due to increased marketing expenses for international brands. Accommodation booking revenue rose 32.7% YoY to RMB 5.2 billion, driven by strong domestic and outbound hotel demand as the decline in ADR narrowed. Transportation ticket revenue increased 16.4% YoY to RMB 4.8 billion, while tourism and vacation revenue grew 23.6% YoY to RMB 900 million, fueled by higher holiday travel demand. Corporate travel management revenue climbed 10.7% YoY to RMB 700 million, supported by rising business travel needs. Total operating expenses reached RMB 7.8 billion, up 4.7% YoY, aligning with revenue fluctuations. Notably, R&D expenses rose 16.4% YoY due to personnel cost changes, and sales expenses surged 44.6% YoY, mainly due to increased overseas marketing investments by the company's international brand, Trip.com.

Performance Summary

Resilient Travel Market and Strong Consumer Desire for Exploration

In 2024, the core OTA platform achieved a GMV of RMB 1.2 trillion. In Q4, outbound travel bookings for hotels and flights rebounded to 120.0% of 2019 levels, driven by simplified visa processes and increased international flights, outpacing the recovery of international flight capacity, which reached 96.6% of 2019 levels. The company's international OTA platform, Trip.com, saw hotel and flight bookings grow by over 70% YoY, contributing 14.0% of Q4 revenue and 10.0% of total 2024 revenue. Meanwhile, inbound travel bookings surged by over 100.0% YoY, supported by further relaxation of transit visa exemptions. Management noted that hotel ADR remained below last year's levels, while supply grew in the high single digits YoY, and they expect hotel prices to stabilize in 2025 as travel infrastructure continues to improve.

New Capital Return Measures: First-Ever Final Dividend

As part of its capital return strategy, the company plans to issue its first-ever final dividend of USD 0.3 per share. Additionally, the board has approved a new capital return program for 2025, authorizing a USD 400 million share repurchase plan.

Investment thesis

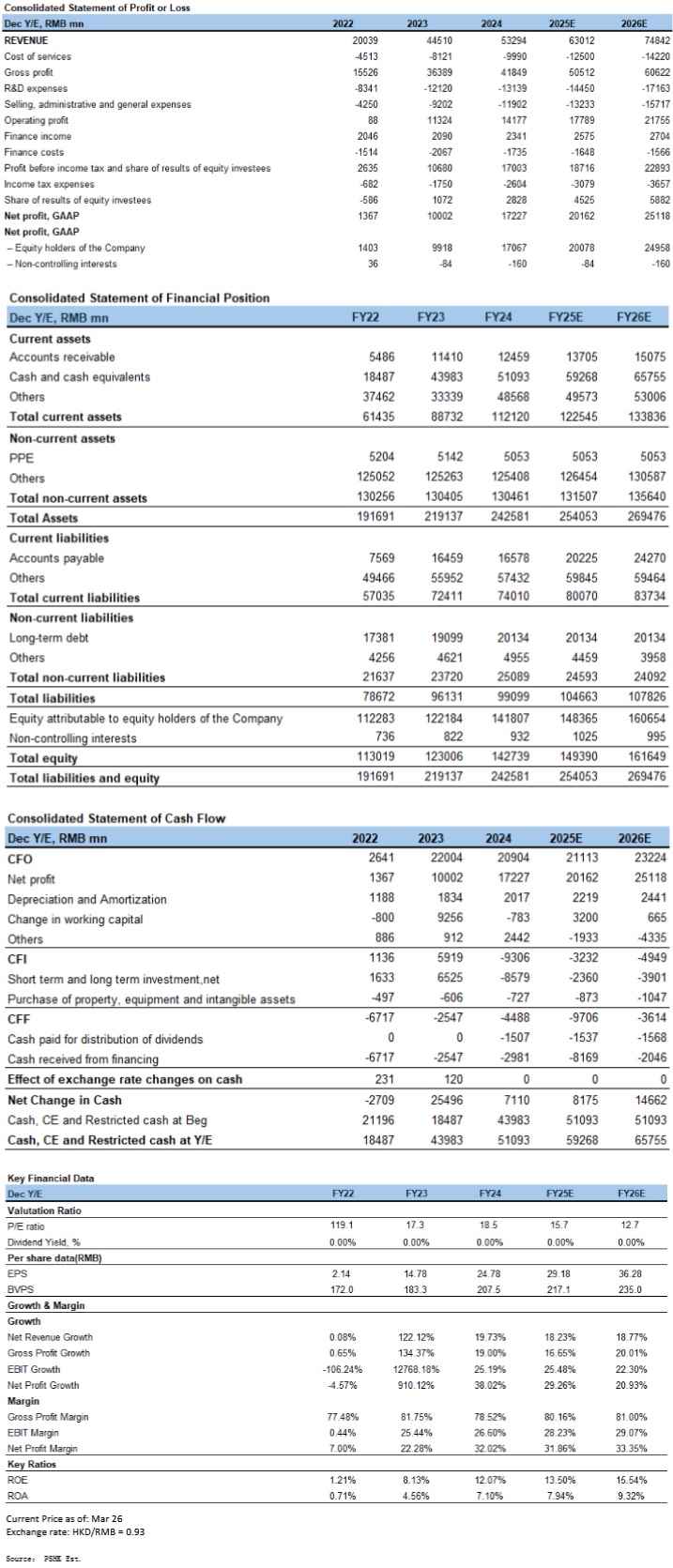

The company has established a comprehensive supply chain and fulfillment system tailored to different customer segments, including the general public and senior travelers, while also expanding its international OTA business. Management is optimistic about AI-driven innovation enhancing user experience, envisioning AI agents replacing traditional search engines as the primary traffic gateway, thereby opening new customer acquisition channels, improving operational efficiency, and gradually alleviating cost pressures. Additionally, the company plans to continue investing in its overseas brand expansion, which may pressure profit margins in the short term but is expected to drive new revenue growth in the long run. As a result, we forecast the company's revenue to reach RMB 63.0 billion in 2025 and RMB 74.8 billion in 2026, with GAAP net profit of RMB 20.1 billion and RMB 25.0 billion, respectively, translating to diluted EPS of RMB 29 and RMB 36. At the current stock price, this implies a PE ratio of 14.3x for 2025 and 11.5x for 2026.

For valuation, we use global OTA peers such as Booking, Expedia, Airbnb, and Tongcheng Travel as comparables. However, given that Trip.com's international expansion is still in its growth phase, leading to near-term margin pressure, we apply a slightly lower PE of 19x compared to the 2025 industry average. Based on this, we revise our target price downward to HKD 584 and maintain a "Accumulate" rating.

Risk factors

1) Domestic consumption demand is weaker than expected; 2) International business expansion is slower than anticipated; 3) Hotel ADR and airfare pricing pressures are greater than expected.

Financials

Click Here for PDF format...