Company profile:

Shanghai Baolong Automotive Corporation(Baolong or the "Company") started with tire valves. Later, following the automobile development trend, the Company continuously expanded the product line, and successively engaged in wheel weights, exhaust pipes, lightweight structural parts, TPMS (tire pressure monitoring system), as well as the intelligent automotive field of sensors, ADAS (that is, advanced driver assistance systems, mainly based on vision products and millimeter-wave radars), and air suspension. After more than 20 years of development, the Company is at the forefront of the segment in terms of the market share of its traditional business, namely, tire valves, wheel weights, exhaust pipes, and TPMS, which is currently the main source of revenue and profit. The Company's emerging business covers intelligent drive solutions-related parts and hydraulic lightweight structural parts, such as sensors, air suspension, and ADAS. The emerging business is currently the core direction of the Company's vigorous development, and will be an important growth point for future revenue and profit.

Investment Summary

Air Suspension and Sensor Continues to Grow Rapidly, Driving Quick Revenue Growth

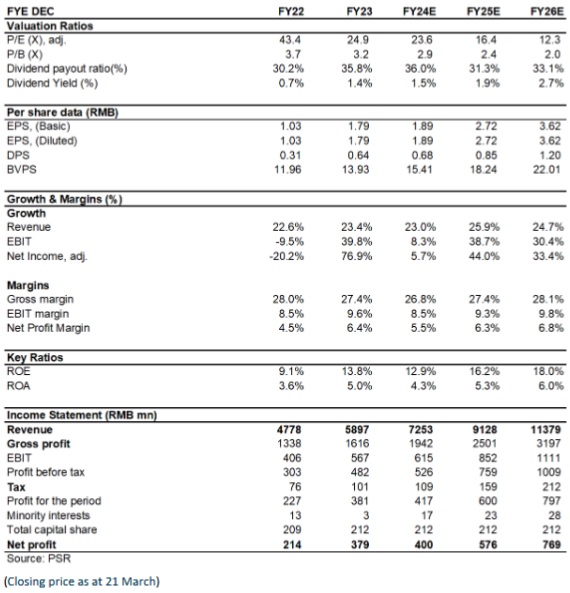

In the first three quarters of 2024, Baolong reported a total revenue of RMB5,026 million, an increase of 20.96% yoy. On a closer look at each quarter, Q1, Q2, and Q3 recorded revenues of RMB1,483 million, RMB1,701 million, and RMB1,843 million, with yoy growth rates of 24.94%, 18.97%, and 19.75%, respectively. The main reason for the sustained high growth of revenue is the rapid ramp-up and expansion of emerging businesses such as air suspension and sensors, while the traditional businesses of Tire Pressure Monitoring Systems (TPMS) also performed well. Major downstream automaker customers, such as BYD, XPENG, LUXEED, and Li Auto, with strong sales, have strongly supported the rapid increase in the Company's product sales.

On a closer look at each business segment, in the first three quarters, the Company's revenues from major segments such as TPMS, automotive metal fittings, valve cores, air suspension, and sensors stood at RMB1,621 million, RMB1,117 million, RMB588 million, RMB628 million, and RMB471 million, up by 21.23%, 6.23%, 6.49%, 28.86%, and 38.03%, respectively. The Company has become one of the global leading suppliers in niche fields such as valve cores, balancing weights, exhaust pipes, and TPMS.

Short-term Profitability Pressured by Equity Incentive Expenses, But Expected to Improve Later

In the first three quarters, the Company's net profit attributable to the parent company was RMB249 million, a decrease of 26.62% yoy. The net profits for Q1, Q2, and Q3 were RMB68 million, RMB80 million, and RMB100 million, with yoy declines of 27.16%, 11.40%, and 35.21%, respectively. The pressure on net profit was mainly due to the implementation of equity incentives, which increased stock-based compensation expenses, a decrease in gross margin, and a high base for equity investment income last year.The Company's gross margins in Q1/Q2/Q3 of 2024 were 29.45%, 25.08%, and 24.6%, with yoy changes of +1.21 ppts, -2.31 ppts, and -3.55 ppts, respectively. The declines were mainly due to the rapid growth of products with lower gross margins, such as air suspension and Advanced Driver Assistance Systems (ADAS), which led to an increase in their proportion. Additionally, the appreciation of the RMB against the USD affected the profitability of export business.

The Company reported a period cost rate of 19.6% in the first three quarters, an increase of 0.86 percentage points yoy. Specifically, the sales, administrative, R&D, and financial cost rates were 3.47%, 6.61%, 8.31%, and 1.23%, with yoy changes of +0.16 ppts, +0.17 ppts, +0.83 ppts, and -0.29 ppts, respectively. The increase in administrative and R&D cost rates primarily resulted from increased stock-based compensation expenses and greater investment in R&D.

According to the Company's announcement, the equity incentive expense recognized in 2024H1 was approximately RMB77.12 million, with RMB34.22 million recognized in Q3. The Q4 equity incentive expense was expected to be RMB13.25 million, with the total annual equity incentive amortization expense estimated to be approximately RMB124 million. In 2025, the equity incentive amortization expense is expected to be approximately RMB38 million. As the equity incentive amortization expense decreases, the Company expects to benefit from the scale effect, and its period cost rate is expected to improve.

Dual-drive of Lightweight and Intelligent Products

According to the Company's WeChat official account, since the beginning of 2024, the Company has obtained multiple designated projects, and orders have exceeded expectations. The products include TPMS, front and rear air spring assemblies for air suspension systems, controllers, digital HD cameras, binocular stereo cameras, and wheel speed sensors, which are lightweight and intelligent products that align with the trend. The customers include independent brand automakers, new energy vehicle companies, global leading car manufacturers, and global high-end brand car manufacturers. It is expected that emerging businesses such as air suspension will accelerate growth, and with the benefits of the scale effect and increased self-manufacturing rates, profitability will continue to improve.

At the end of October 2024, the Company announced its plan to issue convertible bonds to raise no more than RMB1.39 billion, mainly for the expansion of intelligent manufacturing capacity in air suspension systems and the supplement to working capital. This will help the Company expand production capacity and save financial costs. We believe that thanks to the growth in demand for automotive lightweight and intelligent products, the Company's performance is expected to enter a period of rapid growth in the next few years.

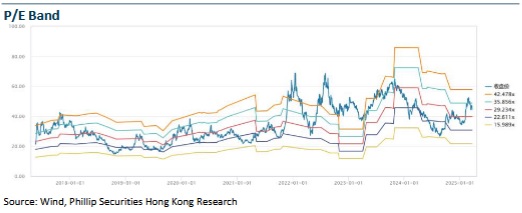

Investment Thesis & Valuation

From a medium- to long-term perspective, the Company's traditional business is expected to maintain steady growth. The Company's emerging business, benefiting from forward-looking layouts and accumulated competitive advantages, is likely to usher in a new high-growth cycle.

As analyzed above, we expected diluted EPS of the Company to RMB 1.26/1.88/2.44 of 2024/2025/2026. And we accordingly gave the target price to 54.3, respectively 28.8/20/15x P/E for 2024/2025/2026. "BUY" rating. (Closing price as at 21 March)

Financials

Click Here for PDF format...