Overview

Hong Kong and China Gas (0003.HK) was established in 1862. The company is the only gas supplier in Hong Kong and one of the largest energy suppliers locally. The company started its gas business in mainland China in 1994. Currently, it has more than 900 projects in mainland China, including renewable energy solutions (such as solar photovoltaic systems), urban pipeline gas, upstream, midstream, water supply, urban waste resource utilization, emerging environmentally friendly energy, etc., and its business covers 29 provincial regions across the country. The company is actively developing clean energy covering sea, land and air, including hydrogen for vehicles, green methanol for ships, and sustainable aviation fuel. Henderson Land Development Group is the company's major shareholder, and real estate tycoon Li Shau-kee is the actual controller. The company's subsidiary, TOWNGAS SMART ENERGY COMPANY LIMITED, was listed on the Hong Kong Stock Exchange in 2005 with the stock code 1083.HK.

Company performance review

In the first half of 2024, the company's revenue was HK$27.49 billion with a year-on-year decrease of 5.8%. The operating profit after tax was HK$3.89 billion with a year-on-year increase of 1.6%, of which: Hong Kong, China business was HK$2.01 billion with a year-on-year decrease of HK$100 million; Mainland Utility business was HK$1.53 billion, similar to the same period of last year; Renewable business was HK$110 million, achieving strong growth; Extended business was HK$190 million; Other business was HK$50 million, achieving profitability. Core operating profit was HK$3.19 billion with a year-on-year increase of 2.2%. Profits attributable to shareholders were HK$3.04 billion with a year-on-year decrease of 15.9%. EPS was HK$16.3 cents, with a year-on-year decrease of 16.0%. The Board of Directors announced a 2024 interim dividend of HK$0.12 per share. The main reason for the decline in the company's revenue is that the economic recovery in the Mainland and Hong Kong in the first half of 2024 did not meet expectations. The consumption enthusiasm of Hong Kong local citizens to the north of mainland led to a decrease in gas consumption in Hong Kong's catering and hotel industries, which in turn led to the failure to increase the sales of industrial and commercial gas. In addition, there were many high temperature days in the first half of the year and the strong exchange rate of Hong Kong dollar against RMB, which brought challenges to the company's business.

Company business

1.Hong Kong, China business

Hong Kong Utility business remained robust

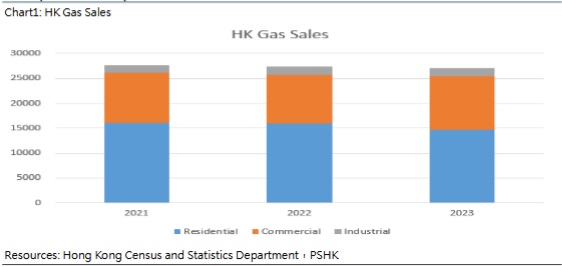

Hong Kong's gas sales volume in the first half of 2024 was 14,932 TJ, roughly the same as the same period of last year.

It can be seen from Chart 1 that local gas consumption in Hong Kong is mainly residential gas and commercial gas. In 2023, the company's gas sales volume in Hong Kong was 27,125 TJ, of which residential gas accounts for 54.0%, commercial gas accounts for 39.6%, and industrial gas accounts for 6.4%. As of June 30, 2024, the numbers of customers were approximately 2.03 million with an increase of 7,678 from the end of 2023. As of the end of 2023, the company's customer numbers were approximately 2.02 million, and the numbers of the company's customers had been growing steadily over the years. As the time goes, the numbers of residential users in Hong Kong will gradually increase. As the economy gradually recovers, Hong Kong's tourism industry is expected to regain its vitality, driving the growth of commercial gas consumption in hotels, restaurants, etc., and in turn driving the company's gas sales growth.

Gas charges increased, profitability is expected to increase

The company raised its basic tariff by HK1.3 cents per MJ from 1 August 2024. The 4.8% increase is equivalent to a 4.2% increase in the average effective gas tariff (including basic tariff and fuel cost variation charge) in 2023. Following a 26-year freeze, the fixed monthly maintenance charge is to be increased by HK$0.5, bringing it to HK$10. Concurrently, Towngas announced that the basic tariff and the monthly maintenance charge will not be subject to further adjustments for the next two years. After the tariff adjustment, it is estimated that around 70% of Towngas` residential customers will pay no more than HK$10 extra for their gas consumption each month, and about 50% of its commercial and industrial customers will pay less than HK$330 extra for their gas consumption each month. Hong Kong gas pricing includes a basic monthly fee of HK$20, a monthly maintenance fee, a basic pricing fee and a fuel adjustment fee (adjusted according to the actual raw material cost of naphtha). The increase in monthly maintenance charge and basic tariff has led to an increase in the company's gas sales price in Hong Kong.

Continuing to promote smart high-quality products and services

In recent years, the company has continued to launch a series of smart stoves and appliances. Among them, the TGC Little Twin Stars stove series, the first of its kind in Hong Kong, has been very popular among young users and has received enthusiastic responses on social media. In the first half of 2024, the company's stove sales volume increased by 1.4% compared with the same period last year.

Actively deploying hydrogen energy business and promoting Hong Kong to become a hydrogen energy industry center

In the first half of 2024, the company developed Hong Kong's first "green hydrogen" pilot project using biogas at the Tseung Kwan O landfill. It is expected to produce about 330 kilograms of hydrogen per day after it goes into production in 2025. In addition, the company is developing a waste-to-hydrogen project and is cooperating with a national engineering company in the mainland to bid for it, with an expected annual production of 1,500 tons of hydrogen. The parking lot hydrogen power generation charging pile project includes 48 sets of 7kW charging piles, with an expected annual consumption of 30 tons. The relevant projects are expected to build Hong Kong into a hydrogen energy industry center and bring more business opportunities to the company. On 7 Jan 2025, Towngas and Chi Shing New Energy Technology Company Limited, a subsidiary of Chi Shing (Hong Kong) Group, signed a memorandum of understanding for technical cooperation in developing low-carbon and renewable energy utilization, including hydrogen power generation business, to promote green construction sites and green buildings in Hong Kong. Through this partnership, both parties will provide integrated new energy power generation solutions, including hydrogen energy, for construction sites and other applications in Hong Kong.

2. Mainland Utility business

Apparent consumption of natural gas in the mainland continues to grow

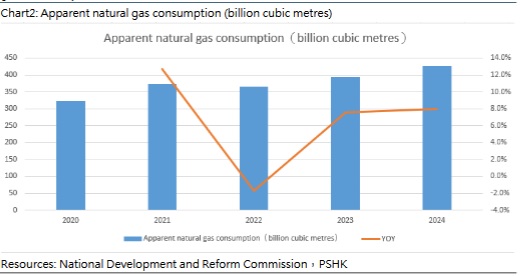

Except for the impact of the epidemic in 2022, mainland natural gas consumption has continued to grow. Starting from 2023, China's apparent natural gas consumption turned from decline to growth and the growth trend continued in 2024. China's annual natural gas consumption exceeded 400 billion cubic meters for the first time, reaching 426.05 billion cubic meters with a year-on-year increase of 8%. According to ¡§the Opinions on Accelerating the Promotion of Natural Gas Utilization¡¨, issued by the National Development and Reform Commission, the proportion of natural gas in primary energy consumption will be increased to about 15% by 2030. There is still a lot of room for growth in the domestic natural gas market in the future.

Gas consumption for power generation drives growth in natural gas consumption

China's natural gas consumption has shown a recovery growth since 2023, mainly driven by urban gas and gas for power generation. The increase in urban gas mainly comes from commercial services, transportation (hot sales of LNG heavy trucks) and heating; the increase in gas for power generation mainly comes from the growth of regional gas power installed generation capacity and the power generation demand during the hot summer period; industrial gas consumption is mainly driven by the continued improvement of the economy, and it shows a rapid growth trend. Data from China Energy News shows that by the end of 2023, China's natural gas power generation installed capacity was 126 million kilowatts with a year-on-year increase of 8.6%. In the past decade, the average annual growth rate of natural gas power generation installed capacity was around 9.5%, higher than the average annual growth rate of the country's total power installed capacity. However, compared with the world average standard, China's natural gas power generation installed capacity accounts for only 4.5%, while the natural gas power generation installed capacity of the United States, Britain, Japan and other countries accounts for more than 40%. In 2023, China's natural gas power generation accounted for 3.2% of the total power generation, while the global natural gas power generation accounted for 23%¡A which shows that there is still much room for the development of natural gas power generation in China, and it is expected to significantly promote the growth of natural gas consumption in the future.

Mainland gas business performed well in the first half of 2024

Although the real estate industry continues to be sluggish, gas consumption in areas such as electric vehicles, lithium batteries, and photovoltaic products has grown rapidly. In the first half of 2024, the company's gas sales volume of urban gas business was approximately 18.6 billion cubic meters with a year-on-year increase of 7%. The number of gas customers exceeded 41.39 million with a year-on-year increase of 7.3%. Together with its subsidiary TOWNGAS SMART ENERGY COMPANY LIMITED, as of the end of June 2024, the Group's total numbers of city gas projects in Mainland China reached 321. The company's share of the mainland city gas market continues to grow, with gas sales volume accounting for 8.9% of mainland natural gas sales in 2023, and the proportion has remained above 8% since 2016.

Gas price spread continues to improve

Benefiting from the decline in upstream natural gas prices, price-adjusting work and refined management, the average price difference of urban gas increased to RMB 0.5 per cubic meter with a year-on-year increase of RMB 0.05 per cubic meter. In 2023, the National Development and Reform Commission issued the "Guiding Opinions on Establishing and Improving the Upstream and Downstream Natural Gas Price Linkage Mechanism". Based on the development of the local natural gas industry and economic conditions, various places of the country have continuously issued policies to improve the local upstream and downstream natural gas price linkage mechanism and have launched or accelerated price linkage reforms. After the policy was promulgated, many regions supplemented the price-adjusting policy. We believe that with the continuous improvement of the natural gas price-adjusting mechanism, the company's gas price difference is expected to continue to rise, effectively improving the company's profitability.

Integrating the gas supply chain and securing ensurance of gas supply

The company actively negotiated with the ¡§Three Majors¡¨ to optimize supply costs and resource allocation and expanded self-owned LNG import, strengthened gas pipeline interconnection, and secured ensurance of gas supply. In 2023, the company officially established a gas supply chain segment to achieve coordinated benefits. In the first half of 2024, the company used the gas storage facility in Jintan District, Changzhou City, Jiangsu Province to carry out the interchange and linkage of delivery modes of pipeline gas and liquefied natural gas, further improving the resilience of the gas supply chain and improving the efficiency of infrastructure. In May, the company's emergency peak-shaving storage and distribution base (Phase I) project in Weiyuan County, Sichuan Province was officially put into operation, and can be exported to Hubei, Jiangxi and other places to achieve cross-regional sales. The company also signed a "Strategic Cooperation Agreement on Deepening New Energy Projects" with the Weiyuan County Government of Sichuan Province. The two parties will further deepen cooperation in shale gas hydrogen production, helium extraction, distributed energy and other aspects in the future.

Water and sanitation profits grew steadily

In the first half of 2024, the company's water sales and sewage treatment volumes increased by 1.4% and 5.9% respectively compared with the same period last year, and its garbage treatment volume increased by 13.7% compared with the same period last year.

3. Renewable energy business

Core profit of the business increased significantly

The company's renewable energy had gained profitability in 2023 and profits increased significantly in the first half of 2024. The company's photovoltaic projects have attracted a lot of strategic investors. As on 30th June 2024, Towngas Smart Energy signed contracts with an aggregate amount of 3.3 GW photovoltaic capacity and connected 2.1 GW to the grid. Overall revenue increased by 6.3% to HK$10,501 million compared to the same period last year. Core operating profit saw a substantial increase of 57.5% to HK$707 million. In the future, renewable energy business will continue to contribute profits.

4. Extended business

As of the first half of 2024, the company has over 2.03 million and 41.39 million household users in Hong Kong and Mainland China respectively. The company is actively developing extended businesses such as smart kitchens, insurance business, and home safety. In the first half of 2024, the total revenue of the extended business was HK$1.8 billion and the profit was HK$190 million. During the period, Towngas Lifestyle signed a cooperation framework agreement with FSE Nova (China) Company Limited to provide more diversified insurance services to customers. After the State Council issued the "Action Plan to Promote Large-Scale Equipment Updates and Consumer Goods Trade-in" in March last year, many places actively implemented the old-for-new policy. We believe that the company will be able to seize the business opportunities and actively promote the smart kitchen business. In the future, the company's extended business capabilities will continue to upgrade, bringing more profits to the company.

5.Green Energy Business

The Hong Kong SAR Government proposed to vigorously promote airlines to inject SAF in Hong Kong and provide green methanol refueling services for local ships and ocean-going vessels. These two businesses have great development potential, and the company is involved in both, which are expected to become important growth drivers in the future. EcoCeres, Inc., in which the company holds shares, has commercial production capacity for hydrogenated vegetable oil (HVO) and SAF. In the first half of 2024, it successfully increased the production capacity and output proportion of SAF, with SAF production reaching 100,000 tons with a year-on-year increase of three times. Its new factory in Malaysia is expected to be completed by the end of 2025. The company's green methanol production plant in Inner Mongolia Autonomous Region is expected to increase its production capacity to 120,000 tons per year in the next few years and will supply green methanol fuel to more customers. In November 2024, the Company established cooperation with Chimbusco Pan Nation Petro-Chemical Company Limited (CPN), and the Company will supply CPN with green methanol produced by itself and certified by ISCC EU and ISCC PLUS, while CPN will be responsible for selling the relevant green methanol fuel to its customers. In January 2025, Towngas and Global Energy Trading Pte Ltd (Global Energy) in Singapore have signed a memorandum of understanding (MOU) to jointly advance the supply and distribution of green methanol as a marine fuel for the shipping industry.

Company valuation

The company has provided guidance on its full-year business situation in 2024, predicting that gas sales volume in Hong Kong will remain stable, with the number of users increasing by 20,000 households; the company will vigorously develop industrial and commercial customers and accelerate the "gas +" business in mainland, the annual gas volume is expected to increase by 7% to 37 billion cubic meters, and the number of users will increase by 2 million households. The industrial and commercial gas prices will be adjusted in a timely manner, and the residential prices will continue to be improved. The annual price difference is expected to increase by RMB 0.05/cubic meter; the cumulative grid-connected renewable energy will reach 2.3GW, and the power generation will reach 1.65 billion kWh; the total number of customers covered by the extended business in the Mainland and Hong Kong will reach 44.23 million households, and the number of kitchen appliances sold will reach 940,000 units; EcoCeres production will reach 310,000 tons.

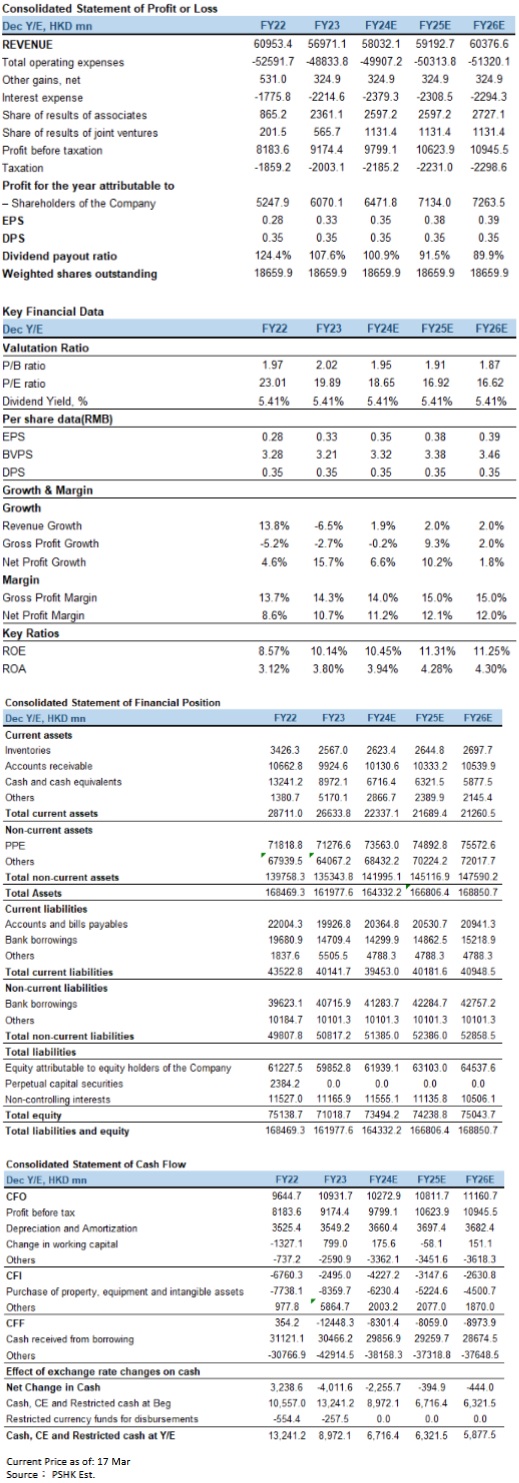

The company has both stability and growth potential, with dividends maintained at HK$0.35 per share for many years. We are optimistic about the growth of the company's mainland gas business and renewable energy business, we predict that the company's revenue will be HK$58.03 billion, HK$59.19 billion and HK$60.38 billion respectively in 2024-2026. EPS will be 0.35/0.38/0.39 HKD. BVPS will be 3.32/3.38/3.46, corresponding to the P/B of 1.95x/1.91x/1.87x. Based on the company's average PB of 2.04 times in the past three years, the company is given a P/B of 2.04 times in 2025, with a target price of HK$6.90, and our investment rating is " Accumulate ". (Current price as of Mar 17)

Risk factors

Hong Kong's gas demand is lower than expected, mainland China's natural gas demand is lower than expected, natural gas prices fluctuation, and national policies.

Financial

Click Here for PDF format...