Investment Summary

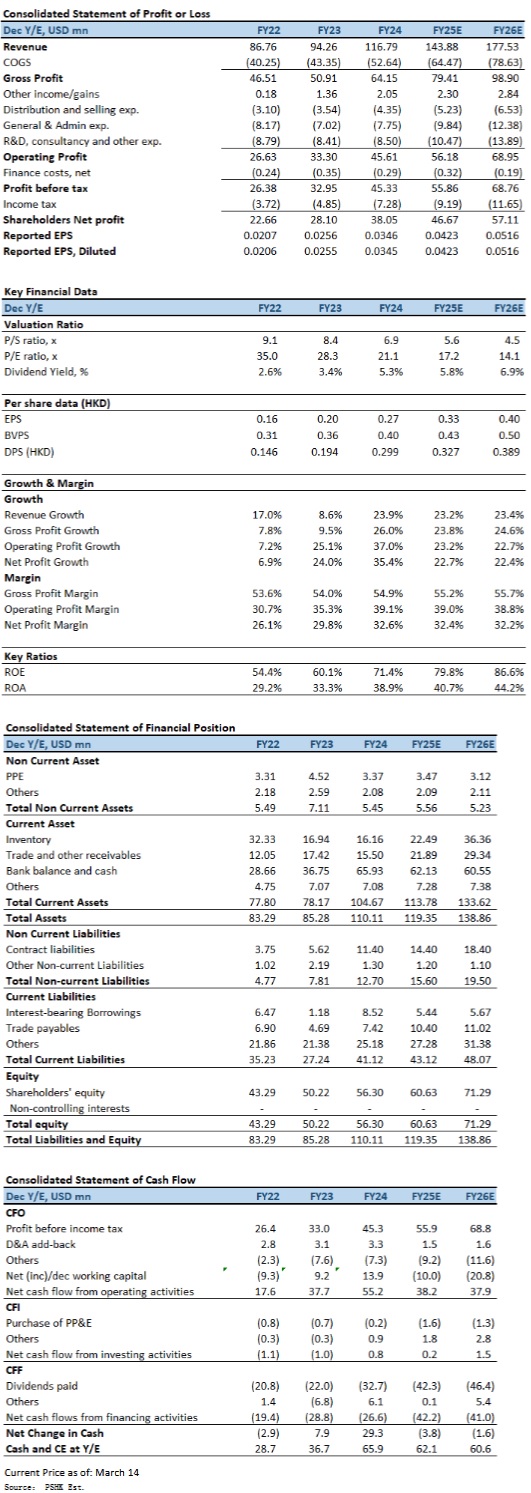

Plover Bay Technologies (01523.HK) recorded solid growth in its financial performance for the fiscal year 2024, with total revenue reaching $116.79 million, representing a 23.9% YoY increase. This growth was primarily driven by the strong sales performance of mobile-first connectivity products, as well as stable expansion in software licensing and warranty support services. Benefiting from an expansion in gross profit margin and operating leverage, profit attributable to equity holders increased by 35.4% to $38.05 million, with diluted earnings per share (EPS) rising to 3.45 cents, reflecting a 35.3% YoY growth. The company declared a second interim dividend of HK13.37 cents per share and a special dividend of HK5.65 cents per share, totaling HK19.02 cents, with a payout ratio of approximately 111.0%.

Revenue Growth Driven by Mobile-First Connectivity Products

As of December 31, 2024, the company recorded $116.79 million in revenue, marking a 23.9% YoY growth compared to 2023. Among its product segments, mobile-first connectivity products exhibited the strongest growth, generating $66.18 million in revenue, a 34.0% increase YoY, driven by the Peplink-Starlink partnership, which significantly boosted demand for SD-WAN routers across various markets. Revenue from fixed network-first connectivity products stood at $17.15 million, up 17.5% YoY, reflecting sustained demand for fixed network solutions from enterprise and government clients. Software licensing revenue reached $8.18 million, growing 25.7%, primarily due to the expansion of InControl2 service subscriptions and other software licensing agreements. While warranty and support services grew at a slower pace, they still contributed $25.28 million, up 6.4% YoY, demonstrating the company's ongoing efforts to expand service-based revenue streams and strengthen its recurring income base.

North American Market Continues to Expand, While Asian Market Faces Short-Term Pressure

The North American market remained the company's primary growth driver, with revenue reaching $74.76 million, reflecting a 37.5% YoY increase. The region's revenue contribution rose from 57.7% in 2023 to 64.0% in 2024. This growth was mainly driven by the increasing adoption of SD-WAN solutions among enterprises, government agencies, and the transportation sector, particularly in applications such as vehicles, railways, and telemedicine.

The Europe, Middle East, and Africa (EMEA) market also showed stable growth, with revenue reaching $29.06 million, up 5.5% YoY. This reflects continued demand for SD-WAN solutions in the region, though growth was slower than in North America, possibly due to longer procurement cycles among enterprises.

The Asian market reported $8.76 million in revenue, marking a 12.2% decline YoY, primarily due to the volatility in government procurement projects, which led to short-term growth constraints. Meanwhile, revenue from other emerging markets surged by 78.4% to $4.21 million, indicating strong market penetration in the maritime, energy, and remote connectivity sectors, showcasing significant growth potential in these industries.

Gross Margin Expansion Enhances Profitability

During the period, gross profit reached $64.15 million, up 26.0% YoY, with the gross margin improving from 54.0% to 54.9%. This was mainly attributed to lower 5G module costs and economies of scale. Among key product segments, mobile-first connectivity product gross margin improved significantly to 37.9%, up 4.2 percentage points from 2023, illustrating the company's effective supply chain management and product mix optimization. Fixed network-first connectivity products also saw their gross margin increase from 42.6% to 45.4%, demonstrating relatively low pricing pressure in this segment. Warranty and support services maintained a high gross margin of 94.3%, while software licensing achieved a gross margin of 91.4%, reflecting the company's successful push toward high-value-added services, further strengthening overall profitability.

The company's revenue growth was primarily driven by the Peplink-Starlink partnership, which expanded SD-WAN product applications across multiple industries. In particular, the North American market saw increased penetration into government agencies, enterprises, and transportation sectors through its distribution channels. Additionally, recurring revenue streams played a crucial role in driving overall growth, with new subscription revenue growing by 36% YoY in 2024, while subscription adoption rates increased from 30.5% at the end of 2023 to 34.1%. This indicates a steady rise in customer demand for warranty and support services.

Moreover, the company benefited from declining 5G module costs and product mix optimization, which significantly improved mobile-first connectivity product margins, further driving overall profitability. Despite the decline in Asian market revenue, this was mainly due to the cyclical nature of government procurement projects and does not affect the company's long-term growth prospects.

Looking ahead, as computing power advances, edge routers are likely to evolve into local computing nodes, reducing reliance on centralized cloud servers. The explosive growth in IoT devices will drive greater integration of local edge computing into connectivity solutions, reducing latency and enabling real-time data processing. Meanwhile, 5G Fixed Wireless Access (FWA) is becoming increasingly prevalent in home and enterprise applications, and the company plans to develop additional multi-WAN-supported products and subscription solutions to meet the market's growing demand for higher bandwidth and reliability. Furthermore, the company is actively enhancing "on-demand" connectivity solutions, enabling enterprise clients to dynamically manage network traffic, and has introduced a mobile application to simplify network management for non-technical users

Investment Thesis and Valuation

Plover Bay Technologies demonstrates strong growth momentum, particularly with the Peplink-Starlink partnership and recurring revenue model driving long-term profitability. Given the company's solid financial position, consistent earnings growth, and stable dividend policy, we forecast the company's earnings per share (EPS) for FY2025 and FY2026 to be 0.0423 and 0.0516 USD, respectively. Our target price is set at HK$6.58, corresponding to a 16.4x forward P/E ratio for FY2026, which is in line with the company's five-year historical average valuation. Our investment rating is ¡§Accumulate¡¨.

Risk factors

1) Global trade policy changes may impact supply chains and market demand; 2) Competitive pressure from new entrants in the SD-WAN market; and 3) Uncertainty in government procurement cycles may affect market performance in Asia.

�Financial

Click Here for PDF format...