Company profile

GEM was founded in 2001, initially focusing on the processing and recycling of waste metals, electronic waste, and other materials. This business now also covers power batteries and end-of-life vehicles, and has expanded into the new energy battery materials sector. The main products in this sector include ternary precursors, cobalt tetroxide, cathode materials, and nickel smelting. In 2023, the Company's ternary precursor shipments reached 180 thousand tons, ranking third in the domestic market.

Investment Summary

Steady Growth in Performance and Continuous Improvement in Profitability

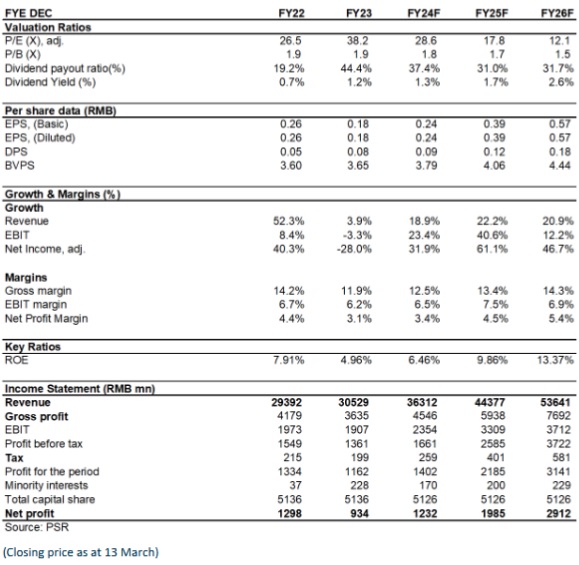

From January to September 2024, the Company reported revenue of RMB24,872 million, a year-on-year increase of 22.96%. Net profit reached RMB904 million, an increase of 65.06% yoy, and operating cash flow amounted to RMB2,052 million, up 282.19% yoy. From 2020 to 2023, the compound annual growth rate (CAGR) of revenue was 34.8%, and net profit CAGR was 31.3%, reflecting good business quality.

Ternary Precursor Business Grows Against the Trend, with the Industry Expected to Improve in the Future

According to ICCSINO Data on Lithium Battery, China's ternary precursor production in 2024 is expected to reach 851 thousand tons, a 0.7% increase yoy. Globally, ternary precursor production will be 963 thousand tons, a 1.7% decrease yoy. In the first three quarters of 2024, GEM's ternary precursor shipments reached 143 thousand tons, a year-on-year increase of 18.94%. Regarding product types, high-nickel products accounted for 55% of global production and 52% of Chinese production in 2024, with year-on-year increases of 3 and 5 percentage points, respectively. GEM focuses on high-end products such as ultra-high-nickel precursors, with a capacity utilization rate of over 95%. Currently, ternary lithium batteries account for more than 90% of the market share in the electric vehicle sector in Europe and the United States. It is expected that demand for electric vehicles in these markets will rebound after 2025. In the domestic market, as the cost gap between ternary and lithium iron phosphate batteries continues to narrow, and with the demand driven by popular domestic models, shipments of high-performance, high-safety ternary batteries are also expected to recover.

Overseas Business Expansion Lays the Foundation for Growth Potential

According to the Company's announcement, as of the end of June 2024, GEM has already put into production 40 thousand tons of nickel smelting capacity in Indonesia. With the gradual commissioning of new capacity, the Company expects to reach a total of 150 thousand tons of nickel smelting capacity by the end of 2024, adding 110 thousand tons of capacity within the year. We expect GEM's MHP (Mixed Hydroxide Precipitate) production to grow by 122% year-on-year, with a target shipment of 60 thousand tons. Compared to the RMB2 billion sales revenue from MHP in 2023, with a gross margin of 32.85%, GEM's profitability will significantly improve as MHP production ramps up further. Additionally, GEM has completed the construction of 50 thousand tons of ternary precursor capacity in Indonesia, providing precursor support for Chinese enterprises` overseas industrial chains and the European and American markets. This capacity has already been fully booked by customers.

Recycling Business Benefiting from the ¡§Trade-in for New¡¨ Subsidy Policy

In the first half of 2024, GEM recycled 16,300 tons of power batteries (1.84 GWh), representing a year-on-year increase of 36.72%. The tungsten resources business recycled 3,458 tons, achieving sales of RMB768,927,600, a 60.18% yoy increase in revenue. The end-of-life vehicle recycling business handled over 150 thousand tons, generating sales of RMB414,157,300, a 99.42% yoy increase in revenue. The cobalt recycling business shipped 8,987 tons, with sales reaching RMB1,579,363,200, a 124.57% year-on-year revenue increase.

Investment Thesis

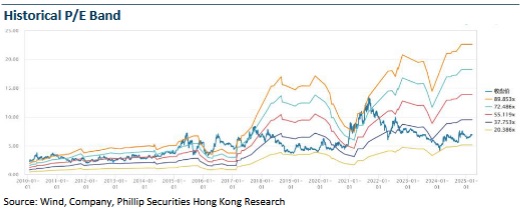

As for valuation, we expected diluted EPS of GEM to RMB 0.24/0.39/0.57 of 2024/2025/2026, considering the orderly release of production capacity and steady growth of recycling business. And we accordingly gave the target price to RMB 8.42, respectively 35/21.7/14.8x P/E for 2024/2025/2026. "BUY" rating. (Closing price as at 13 March)

Risk

Progress of new production line is below expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

Click Here for PDF format...