Company profile:

Bethel is a tier-one supplier of auto parts. The Company's major products are divided into three categories, namely mechanical brake products, mechanical steering products, and intelligent electrical control products. Specifically, mechanical brake products mainly include disc brakes, hydraulic calipers, lightweight parts, and vacuum boosters; mechanical steering products mainly include steering columns and steering gears; intelligent electrical control products mainly include EPB, ABS, ESC, WCBS, PLG, the advanced driver-assistance system (ADAS) based on the front-view camera system, and electronic power steering (EPS) columns.

Investment Summary

30% Increase in Profit for the First Three Quarters

According to Bethel's financial report of Q3 2024, the Company reported revenues, net profits attributable to the parent, and net profits excluding non-recurring gains of RMB2,607 million, RMB321 million, and RMB287 million, respectively. These figures represent year-on-year (YoY) increases of 29.66%, 33.96%, and 33.04%, respectively, and quarter-on-quarter (QoQ) increases of 23.52%, 29.51%, and 24.97%, respectively.

For the first three quarters of 2024, the Company recorded total revenue of RMB6,578 million (up 28.85% YoY), net profit attributable to the parent of RMB778 million (up 30.79% YoY), and net profit excluding non-recurring gains of RMB709 million (up 30.85% YoY).

Rapid Growth in Smart Electrical Control and Lightweight Braking Product Sales, and Strong Performance of Core Customers, as the Key Driving Factors

By product category, in Q3 2024, Bethel's sales of smart electrical control products, disc brakes, lightweight braking components, and mechanical steering products were 1,350 thousand, 870 thousand, 3,530 thousand, and 730 thousand units, respectively, representing YoY increases of 33%, 12%, 55%, and 17%. On a QoQ basis, sales grew by 25%, 23%, 6%, and 24%, respectively.

For the first three quarters of 2024, sales of smart electrical control products, disc brakes, lightweight braking components, and mechanical steering products were 3,340 thousand, 2,270 thousand, 9,660 thousand, and 2,060 thousand units, respectively, with YoY growth rates of 32.53%, 13.70%, 58.99%, and 19.86%. The strong growth of smart electrical control and lightweight braking products was mainly driven by the ramp-up of steer-by-wire and EPB products, as well as the gradual increase in capacity at the Company's Mexican factory.

In Q3 2024, sales of passenger vehicles by Bethel's core customers-Chery, Changan, Geely, and Li Auto-grew by 22%, dropped by 19%, grew by 20%, and grew by 45% YoY, respectively, and on a QoQ basis grew by 19%, dropped by 11%, grew by 13%, and grew by 41%, respectively, showing overall strong performance.

Improvement in Profitability QoQ

Due to intensified competition among downstream automakers, component manufacturers have faced margin pressures. In Q3, Bethel's gross margin was 21.6%, a decrease of 1.0 percentage point YoY, but an increase of 0.1 percentage points QoQ. This marks the second consecutive quarter of QoQ improvement, likely benefiting from the increased share of high-margin lightweight business and positive economies of scale. The Company's net profit margin stood at 12.57%, reflecting YoY and QoQ increases of 0.4 and 0.7 percentage points, respectively, with a one-off income of RMB30 million from a penalty fee boosting the results.

For the first three quarters of 2024, Bethel's gross margin was 21.29%, down 1.04 ppts YoY, and its net profit margin was 11.99%, up 0.08 percentage points YoY. The Company has maintained solid cost control, with sales, management, R&D, and finance expense ratios at 0.99%, 2.46%, 5.84%, and -0.44%, respectively, showing changes YoY of -0.10, -0.12, -0.16, and +0.07 ppts, respectively.

Ongoing Expansion of New Capacity and Sufficient New Project and Order Reserves

Bethel is continuously expanding its production capacity. The domestic lightweight production base is undergoing its Phase III project, primarily for the production of lightweight products such as automotive subframes and hollow control arms. The Company has added new annual capacities of 300 thousand sets for EPS and 300 thousand units for EPS-ECU production lines. The Phase II project in Mexico is progressing smoothly. The Company plans to issue RMB2.8 billion in convertible bonds to accelerate the expansion of its competitive business capacities. The investment will primarily focus on five strategic projects, including the annual production of 600 thousand sets of electronic mechanical brakes (EMB) and their R&D and industrialisation.

The Company's ongoing and new mass production projects are expanding rapidly. From January to September 2024, Bethel had 432 ongoing projects (up 12% YoY), 235 new mass production projects (up 19% YoY), and 301 new projects under contract (up 65% YoY). Among these, the number of the ongoing, new mass production, and new contracted projects for disc brakes, lightweight products, electronic control products, and steer-by-wire systems were 89/38/58, 48/43/30, 253/131/181, and 69/24/50, respectively. These include the appointment of a North American electric vehicle company for a lightweight project with an expected total sales revenue of approximately USD122 million over its five-year lifecycle, with a peak annual sales of around USD31.46 million. Additionally, an EPB project for a German joint venture automaker is expected to generate approximately RMB600 million in total sales over its eight-year lifecycle, with a peak annual revenue of about RMB96 million.

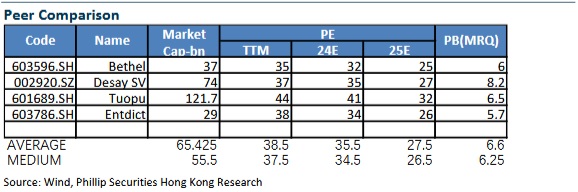

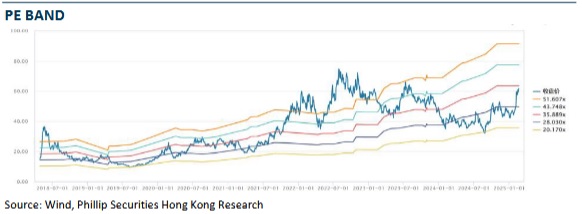

Investment Thesis & Valuation

Automotive intelligence is a long-term trend in the industry, in which the intelligent electrical control brake field plays an important role. As one of a few local enterprises that own independent intellectual property rights and can realize the mass production of EPB, ESC, ABS, and WCBS products, the Company is expected to achieve domestic substitution by expanding customer groups.

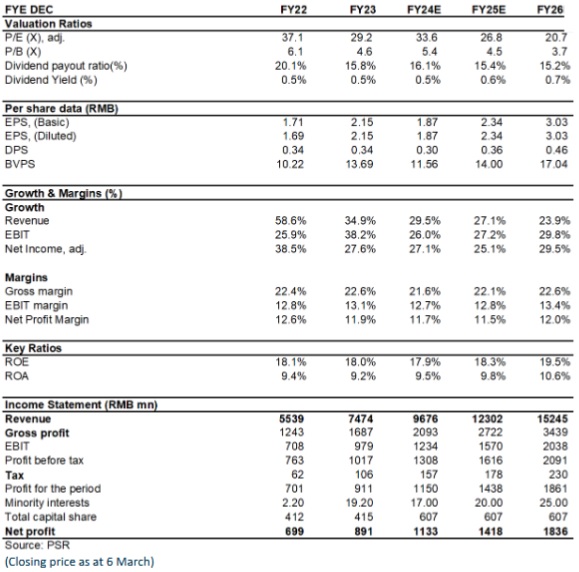

Bethel has clear independent capabilities for wire-controlled product integration and technology iterations. In the short run, the Company benefits from the rapid mass production in the lightweight and EPB business. In the medium and long run, its intelligent electrical control business is expected to create a second growth curve. Therefore, with resilient results in the future, the Company should enjoy a certain valuation premium. We expected diluted EPS of the Company to RMB 1.87/2.34/3.03 of 2024/2025/2026. And we accordingly gave the target price to 67.7, respectively 36.2/29/22.4x P/E for 2024/2025/2026. "Accumulate" rating. (Closing price as at 6 March)

Financials

Click Here for PDF format...