Investment Summary

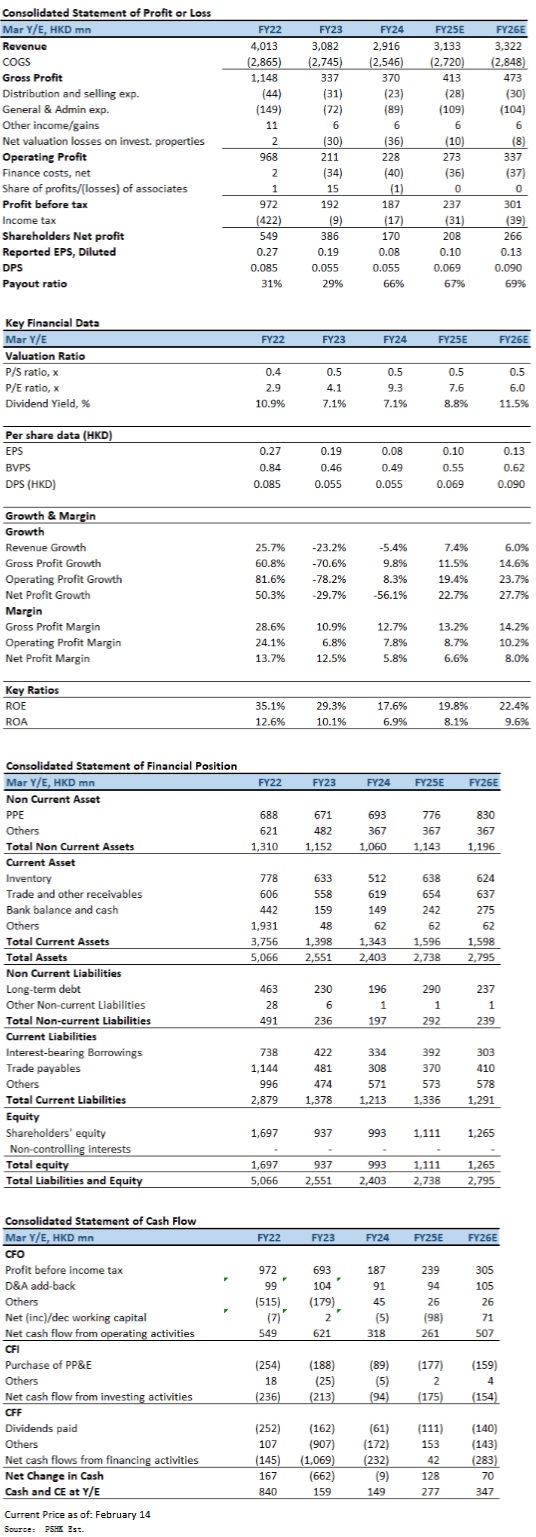

Karrie International delivered solid growth in the 1H2025FY (For the six months ended September 30), with revenue reaching HK$1.53 billion, representing a 6% yoy increase. The company benefited from strong demand in the artificial intelligence (AI) server market, which drove steady growth in sales of server molds and enclosures. As a result, the gross profit margin improved by 0.5 percentage points to 13.2%, enhancing overall profitability. Net profit surged 39% yoy to HK$102 million, with the net profit margin increasing from 5.8% to 6.7%. Earnings per share (EPS) rose to HK5.0 cents (1H2024FY: HK3.6 cents), while an interim dividend of HK2.5 cents per share (1H2024FY: HK1.5 cents) was declared, amounting to a total payout of HK$50.53 million and a payout ratio of 50%.

Financial Performance Highlight

For the six months ended September 30 2024, Karrie International's revenue increased to HK$1.53 billion, up 6% yoy. The metal and plastic business demonstrated exceptional performance, with revenue reaching HK$952 million, representing a 14% yoy growth and accounting for 62% of total revenue. This expansion was primarily driven by robust demand for AI server enclosures and molds. In contrast, the electronic manufacturing services (EMS) business faced headwinds, with revenue declining 5% yoy to HK$574 million due to weaker demand for traditional electronic products.

Gross profit rose to HK$201 million, a 20% increase from HK$167 million in 1H2024FY. The gross profit margin improved from 12.7% to 13.2%, supported by three key factors. First, the increasing contribution from the higher-margin metal and plastic business boosted overall profitability. Second, raw material costs declined, providing a favorable cost advantage. Lastly, enhanced production efficiency through automation upgrades and process optimization helped reduce manufacturing costs.

Operating profit reached HK$135 million, up 31% yoy, with the operating profit margin increasing from 7.2% to 8.9%. Net finance costs decreased 10% yoy to HK$18.15 million, reflecting the company's efforts to optimize its loan portfolio and reduce borrowing costs. Net profit totaled HK$102 million, marking a 39% yoy increase, while the net profit margin expanded from 5.8% to 6.7%, demonstrating improved operational efficiency and a more favorable revenue mix.

Operating cash flow remained positive at HK$88.1 million, though lower than the HK$190 million recorded in the previous year. The decline was primarily attributed to higher inventory levels, as the company invested in expanding production capacity at its Thailand facility to meet rising demand from international markets.

CAPEX for the period amounted to HK$135 million, an 11% decrease from the previous year. Karrie maintained a healthy liquidity position, with cash and bank deposits totaling HK$209 million and unused banking facilities of HK$768 million. The gearing ratio increased to 45% from 39% due to higher bank borrowings.

The interim dividend of HK2.5 cents per share, representing a 67% yoy increase. The payout ratio remained at 50%, reflecting the company's commitment to balancing shareholder returns with future growth investments.

Strong demand in the artificial intelligence (AI) server market

The rapid development of AI is driving the expansion of data centers and cloud computing markets, leading to increased demand for high-performance servers. As a major supplier of server enclosures, Karrie International has benefited from this trend, with significant revenue growth in its metal and plastic business. The company offers comprehensive mechanical engineering solutions, including mold development, rapid prototyping, precision manufacturing, and automated production. Leveraging these technological advantages, Karrie has established a leading position in the market.

In terms of automated production, the company continues to optimize capacity allocation at its Dongguan and Thailand facilities. The Thailand plant has reached optimal production levels, securing certifications from multiple customers and experiencing stable order growth. This expansion not only mitigates geopolitical risks but also enhances supply chain stability. Additionally, Karrie closely monitors international market dynamics and adjusts its supply chain strategies flexibly to ensure sustained business growth.

Although the electronic manufacturing services (EMS) business faces challenges due to weakening market demand, the company is actively restructuring its product portfolio. By focusing on high-value-added data storage devices and emerging market applications, Karrie aims to enhance the profitability of this segment.

Investment Thesis

Driven by strong demand in the AI server market, Karrie International has delivered solid performance, with continuous improvements in gross margin and profitability. The company maintains a competitive edge in automated production and global supply chain management, particularly with the successful operation of its Thailand facility, which helps diversify geographical risks and flexibly meet the diverse needs of customers. However, challenges remain in the electronic manufacturing services (EMS) business, requiring ongoing product portfolio optimization to enhance segment profitability. Karrie's strategic positioning within the AI supply chain is well-defined, and we expect the company's earnings per share (EPS) for FY2025 and FY2026 to be HK$0.10 and HK$0.13, respectively. Our target price is set at HK$0.98, corresponding to a 9.6x forward P/E ratio for FY2025, which is in line with the industry average. Our investment rating is ¡§Buy¡¨.

Risk factors

1) geopolitical risks; 2) demand weakness in the EMS segment; 3) cost pressures and margin risks; and 4) uncertainties in overseas expansion.

Financial

Click Here for PDF format...