Company profile

Hua Hong Semiconductor is currently the second largest semiconductor foundry in mainland China and the sixth largest globally. It provides foundry services on 8-inch and 12-inch wafer platforms, offering embedded/independent non-volatile memory, power devices, analog and power management, logic, and RF on five distinct process platforms. It has become the most comprehensive semiconductor foundry with distinctive process platforms. According to TrendForce data, in the embedded non-volatile memory sector, the company is the world's largest smart card IC manufacturing foundry and the largest MCU manufacturing foundry domestically. In the power device sector, the company is the world's top-ranked power device wafer foundry in terms of capacity and the only enterprise with both 8-inch and 12-inch power device foundry capabilities.

3Q24 performance exceeded previous guidance

The company's revenue for 3Q24 was $530 million, a year-on-year decrease of 7.4%, with a gross margin of 12.2%, down 3.9% year-on-year. This was primarily due to pressure on ASP, partially offset by increased wafer shipments and improved capacity utilization. The net profit attributable to the parent company was $44.8 million, up 222.6% year-on-year. In terms of application areas, management indicated that the consumer electronics sector remained strong as the largest end market, while the industrial and automotive products showed weakness, mainly due to declining average selling prices and demand for IGBT products. From a regional customer perspective, the company's overall demand from overseas customers remains stable. However, revenue in the China region decreased by 1.5% year-on-year, primarily due to declines in demand and average selling prices for IGBT, super junction, and flash memory products. This was partially offset by increased demand for CIS and other power management products.

4Q24 Outlook

The company forecasts revenue for 4Q24 to be around $530-540 million, in line with industry averages. The gross margin for 4Q24 is expected to be approximately 11.0%-13.0%, lower than that of other industry players, primarily due to lower ASP. Given the ongoing challenges in the overall macroeconomic environment in China and no significant improvement in industrial output, it is expected that the industrial and automotive sectors will continue to lag in growth, putting pressure on demand for high-voltage IGBT and ultra-junction products. However, with the continued growth in artificial intelligence demand, the company's CIS, BCD, and logic business in data center applications are performing well. The company anticipates price pressure on the 8-inch business in the fourth quarter, but with the gradual resolution of the technical bottlenecks faced in the expansion of the 12-inch capacity mentioned in the 2Q24 earnings call, there is a trend of increasing capacity utilization rates for 12-inch wafers, with a slight potential increase in ASP.

The capacity ramp-up at the Wuxi Phase II wafer fab is progressing smoothly, and the new factory is expected to be completed and operational by the end of 2024

The construction of the company's second 12-inch production line is progressing rapidly. Trial production and process verification for various technology platforms are expected to fully commence by the end of this year to early next year. Once operational, the company's production capacity and specialized technology platforms will be further expanded and enhanced to meet the growing and emerging demands from downstream markets, unlocking greater potential. Management anticipates that the new line will add 10,000 to 20,000 wafers per month in capacity, with plans to increase total capacity to 83,000 wafers per month within the next two to three years. We expect that Hua Hong will not have significant capital expenditure plans once the production line is fully completed.

Company valuation

Considering the recovery in consumer electronics terminal demand, the expected bottoming out and recovery of ASP, and the gradual release of capacity from the Wuxi Phase II project, it is anticipated that these factors will drive product portfolio optimization and promote revenue growth. We forecast the company's operating income for the years 2024, 2025, and 2026 to be $2.0 billion, $2.4 billion, and $2.5 billion respectively. We also anticipate the net profit attributable to the parent company to be $86 million, $285 million, and $299 million respectively, with corresponding diluted EPS of $0.05, $0.17, and $0.17. Overall, as a semiconductor foundry player with high capital investment, we believe the company's valuation is slightly below the industry average, at 1.0x the 2025E PB, corresponding to a target price of HK$30.30 per share. We are initiating coverage with an `Accumulate` rating.

Exchange rate: HKD/USD=7.79

Risk factors

1) Tightening of U.S. export controls; 2) Lower-than-expected ramp-up of capacity at the Wuxi wafer fab; 3) Weaker-than-expected increase in ASP.

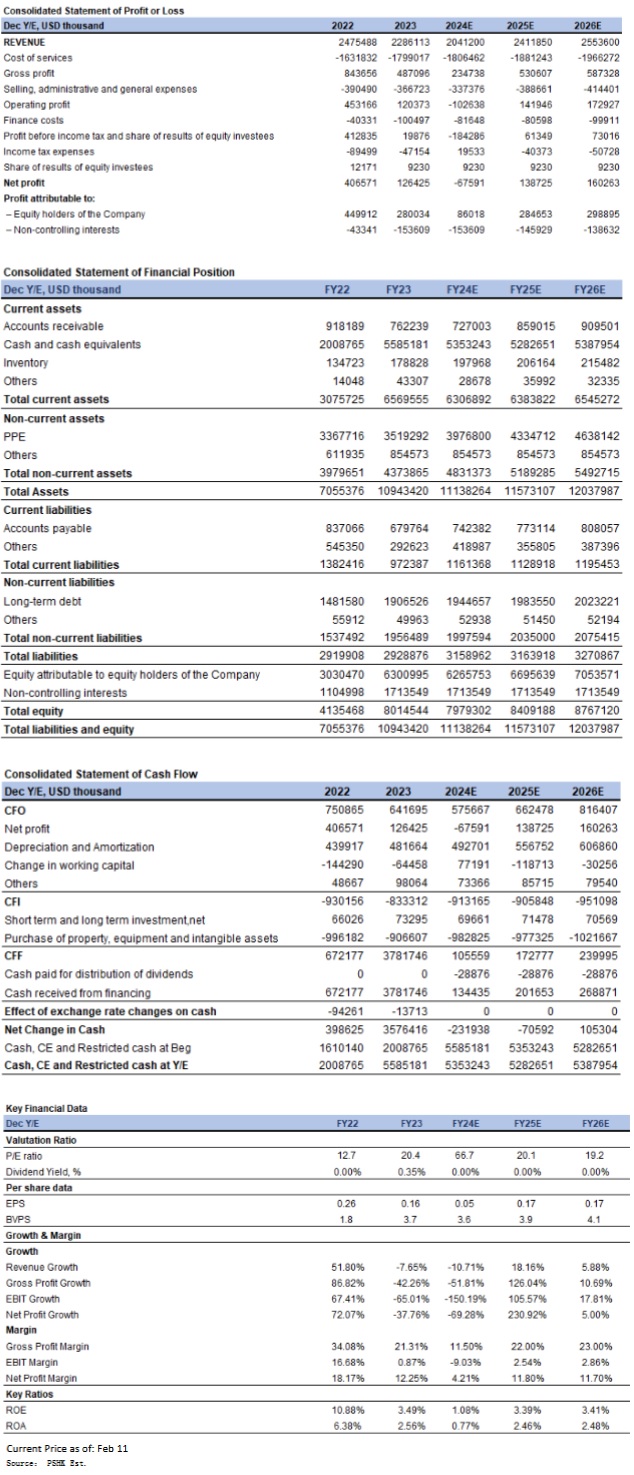

Financials

Click Here for PDF format...