Overview

Zhaojin Mining (1818.HK) is a comprehensive gold producer and gold smelting enterprise that integrates exploration, mining, beneficiation and smelting operations and focuses on developing the gold industry. The company's main products are gold" and gold" standard gold ingots. As of December 31, 2023, the company has a total of approximately 38,10 million ounces of gold mineral resources and approximately 15.18 million ounces of mineable gold reserves. In the first half of 2024, a total of 14.31 tons of new gold was discovered through exploration.

Company performance review

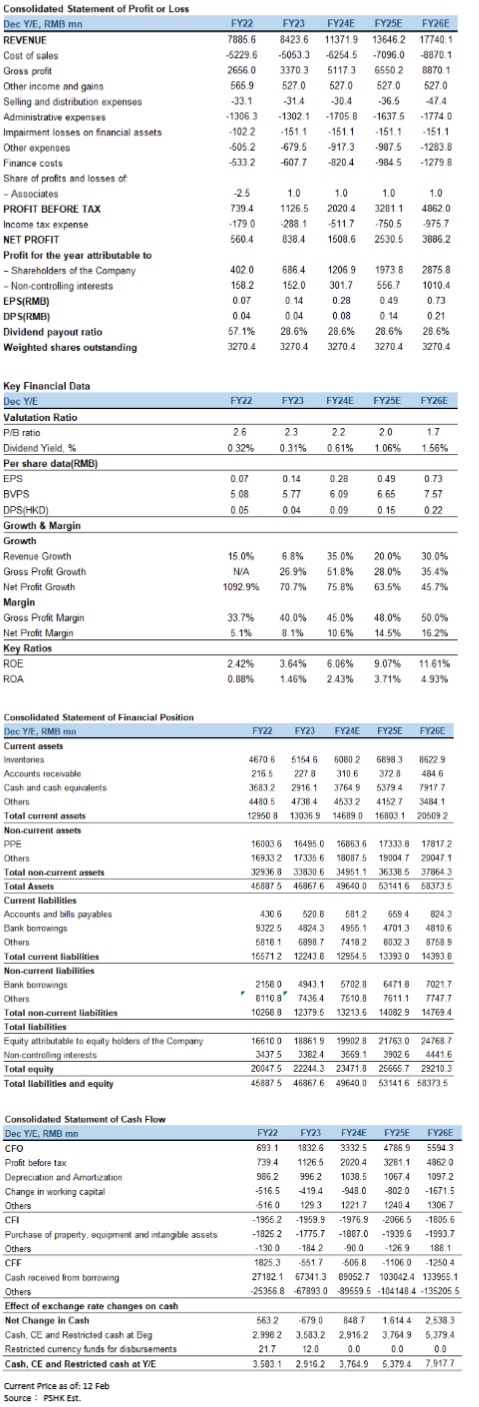

As of September 30, 2024 (January-September), the company's revenue was 8.09 billion yuan (RMB, the same below) with a year-on-year increase of 26.6%. Operating costs were 4.46 billion yuan with a year-on-year increase of 14.2%. Operating profit was 1.66 billion yuan with a significant year-on-year increase of 109.80%. Net profit was 1.23 billion yuan with a significant increase of 128.4%. EPS was 0.26 with a year-on-year increase of 136.4%. The company's performance in the first three quarters achieved significant year-on-year growth, mainly due to the upward trend in gold price caused by safe-haven demand.

Industry Analysis

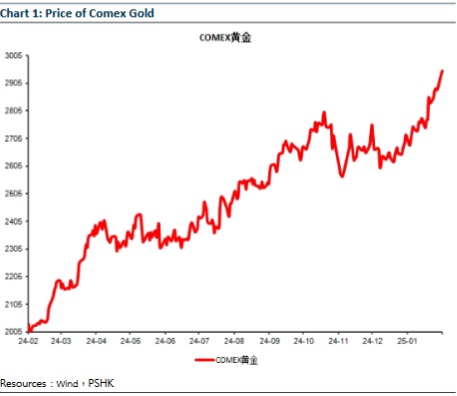

According to statistics from the China Gold Association, on the supply side: in 2024, domestic raw gold production achieved 377.242 tons, an increase of 2.087 tons compared with 2023 with a year-on-year increase of 0.56%, among them, mineral gold production achieved 298.408 tons and non-ferrous by-product gold achieved 78.834 tons. In addition, China's imported raw gold achieved 156.864 tons in 2024 with a year-on-year increase of 8.83%. If the above imported gold is included, China's production of gold achieved 534.106 tons with a year-on-year increase of 2.85%. In 2024, the overseas mines of China large gold companies achieved the gold production of 71,937 tons with a year-on-year increase of 19.14%. In terms of consumption: In 2024, China's gold consumption was 985.31 tons with a year-on-year decrease of 9.58%, among them, gold jewelry consumption was 532.02 tons, with a year-on-year decrease of 24.69%; gold bars and gold coins consumption was 373.13 tons with a year-on-year increase of 24.54%; gold for industry and other purposes consumption was 80.16 ton with a year-on-year decrease of 4.12%. As of the end of December 2024, China's gold reserves reached 2,279.57 tons, ranking sixth in the world, and the gold reserves hit a new historical high. Overall, the supply of gold increased slightly, but the consumption of gold, especially the consumption of gold jewelry declined, mainly because the gold price is prohibitive. Unemployment Insurance Weekly Claims were higher than expected. At the same time, the tariffs and immigration policies implemented by Trump after taking office were weaker than expected. The market expected the Federal Reserve to make a dovish decision. In addition, geopolitical issues remain unresolved, investors` risk aversion demand has increased, and the value of gold has been highlighted. Therefore, we believe that gold price will be strong in the short term.

Important events of the company

In June 2024, Zhaojin Mining's full offer to acquire the Australian TIETTO MINERALS LIMITED project was finalized. TIETTO MINERALS 's flagship asset is the Abuja gold mine, which has a mining area of 1,114 square kilometers, 1.36 million ounces of gold reserves and 3.83 million ounces of resources. Currently, less than 10% of the area has been explored, leaving a lot of room for exploration. The acquisition will help increase Zhaojin Mining's gold resources and self-produced gold production.

In June 2024, Zhaojin Mining announced that its wholly owned subsidiary Starlet Creation Limited completed the acquisition of 60% of the equity of Xijin Mining for a total transaction price of RMB 180 million, thereby indirectly controlling the development of the Komahong gold mine. The gold mine is located in Sierra Africa. The situation in the country is stable and the gold mining development has just started, with good prospects and great room for development. The company's development plan is that in the next stage, based on the project's good profitability, the mining scale will be expanded to 1,500t/d, and the annual output will reach 57,000 ounces (about 1.8 tons). Another reason why the gold mine attracted Zhaojin Mining to acquire it is that it has a good mineralization geological structure environment and great prospecting potential. This acquisition is another strategic move by the company to expand its layout in the African mining market after acquiring the Abuja gold mine in Africa. It will be conducive to forming the circle of scale and synergy, improving market competitiveness, and is expected to bring growth to the company's revenue.

The company and its controlling shareholder Zijin Mining have joined hands to take over ST Zhongrun. This cooperation means the deepening of the company's layout in gold and mineral resources. ST Zhongrun's main assets include its VATUKOULA gold mine in Fiji, which has a mining rights area of 12.55 square kilometers and currently has gold resources of 3.13 million ounces (about 97.2 tons), of which 790,000 ounces (about 24.57 tons) are proven reserves. In the future, the resources and exploration of the VATUKOULA gold mine will have great room for development, which will bring incremental gold production.

The company's Haiyu gold mine construction has been accelerated. By the end of 2024, the two TBMs had been successfully assembled and debugged ahead of schedule and are ready to go. The scale of Haiyu gold mining can reach 12,000 tons/day, and it is expected to be completed and put into production in 2025. After the project is put into production and reaches full capacity, the annual gold output is expected to reach 15-20 tons, which is expected to increase the company's profits.

In December 2024, the Company entered into a finished gold sales framework agreement with its subsidiary Zhaojin Jinye, which will help expand the Company's overseas finished gold sales channels, save sales costs, and thus bring further economic benefits to the company.

Company valuation

Zhaojin Mining has strong competitiveness in the market with its strong industrial resource background and technological innovation capabilities. There is still uncertainty about how Trump will implement the tariff policy after taking office. The rising risk aversion sentiment has caused the gold price to break through the historical high again. The gold price will keep high in the short term and the company's gold production is expected to increase. So the company is expected to realize an increase in both sales and price and achieve revenue growth. We raise our revenue forecast for the company, we predict that the company's revenue will be 11.37 billion yuan, 13.65 billion yuan and 17.74 billion yuan respectively in 2024-2026. EPS will be 0.28/0.49/0.73 yuan. BVPS will be 6.09/6.65/7.57, corresponding to the P/B of 2.18x/1.99x/1.75x. The company is given a P/B of 2.4 times in 2024, with a short-term target price of HK$15.58, and our investment rating is " Accumulate ". (Current price as of Feb 12)

Risk factors

Political factors, monetary policy, gold supply and demand, impact of safety accidents, and changes in gold costs.

�Financial

Click Here for PDF format...