Investment Summary

Strong Result Performance in Q3

In the first three quarters of 2024, Fuyao Glass recorded total revenue of RMB28,314 million, up 18.84% yoy and its net profit attributable to the parent company was RMB5,479 million, up 32.79% yoy, both reaching record highs. In Q3, the operating revenue was RMB9.97 billion (RMB, the same below), up 13.4% yoy; the net profit attributable to the parent company was RMB1.98 billion, up 53.5% yoy.

The Chinese automobile market sold a total of 21.571 million vehicles in the first three quarters of 2024, up 2.4% yoy. The sales volume of new light vehicles in the US increased slightly by 0.7% yoy. In the first three quarters, Fuyao Glass's revenue growth far exceeded the industry average, demonstrating that as a leading company, Fuyao Glass has seen continuous enhancement of its overall competitiveness and siphon effect and further expansion of its market share.

Profitability Improvement

The net profit growth significantly outpaced revenue growth, benefiting from a rapid increase in profitability, and driven primarily by the following factors:

1) The product mix continues to be optimized and upgraded, raising the proportion of high-value-added products. In the first three quarters, the proportion of the Company's high-value-added products reached 58.18%, up 5.25 ppts yoy, with an increase of 8.84% in the ASP.

2) The shipping cost has decreased, and the costs of raw materials such as soda ash and natural gas have experienced a further decline. The Company's gross profit margin for the first three quarters reached 37.82%, up by 2.88 ppts yoy. The gross profit margin for Q3 stood at 38.78%, up 2.47 ppts yoy and 1.05 ppts qoq, respectively.

3) The scale effect has amplified the operating leverage and increased capacity utilization, while advancing the process of automation and informatization, thereby improving operational efficiency and enhancing factory profitability. For example, the net profit margin of the US factory in H1 increased by 4.05 ppts yoy. In the first three quarters, the Company's sales expense ratio was 4.30%, down 0.27 ppts yoy; the administration expense ratio was 7.36%, down 0.06 ppts yoy.

However, the expenses were partially offset by the following factors:

1) The financial expense ratio was -1.59%, up 0.77 ppts yoy, mainly due to changes in exchange gains and losses. This period saw an exchange loss of RMB138 million, compared to an exchange gain of RMB335 million in the same period last year, affecting pre-tax profit by RMB473 million.

2) Due to the termination of the transfer of the remaining 24% equity of Beijing Futong, the investment income decreased by RMB212 million.

As of the end of Q3, the Company's financial position has been good, with cash in hand and bank deposits of RMB19.76 billion, in a net cash position.

CAPEX has increased, German FYSAM has turned profitable, and the high-end trend in automotive glass is expected to drive continued result growth

To meet market development needs, the Company has been in the third round of accelerated capital expenditure in the past two years. Under the guidelines of the management, the capital expenditures for the 2025 plan are RMB7-7.5 billion, slightly lower than the RMB8 billion planned for 2024. The capital expenditure will be mainly used for the capacity expansion of new factories in Fuqing, Fujian and Hefei, Anhui, the expansion project in the second phase of the automotive glass in the US, and the aluminium trim project in Shanghai and Fuqing/Changchun, to further enhance global market share.

From January to September 2024, German FYSAM reported an operating income of -EUR6.65 million, down EUR17.06 million yoy. German FYSAM is on the verge of turning loss into profit.

With the continuous advancement of automotive intelligence, the improvement of assisted driving levels, the application and development of various new technologies and scenarios, and the enhancement of user experience consumption, the trend towards high-end automotive glass is expected to continue. There is room for further increase in the proportion of high-value-added products in the Company's product mix.

Investment Thesis

In the short term, the prices of raw materials and energy in Q4 continue to decline, and the subsequent loss reduction of SAM and the improvement in the efficiency of the US factory are expected to bring more potential profit flexibility. In the medium to long term, we expect the proportion of high-value-added products in automotive glass to continue to increase. The Company is also continuously expanding its product boundaries, opening up space for long-term sustainable growth. As a global leader in the automotive glass industry, the Company is expected to continue benefiting from its competitive advantages and maintain a high dividend payout ratio.

We forecast its EPS to be RMB 2.17/2.41/2.92 in 2024/2025/2026. We give the "Accumulate" rating, with a revised target price to be HK$59.3, equivalent to 19.6/17/14.9x P/E for 2024/2025/2026. (Closing price as at 11 February)

Risks

Demand for automobiles keeps sluggish; cost of raw materials increases; RMB appreciates

Catalyst

Success market development of overseas automobile market; rebound of domestic demand for automobile; depreciation of RMB

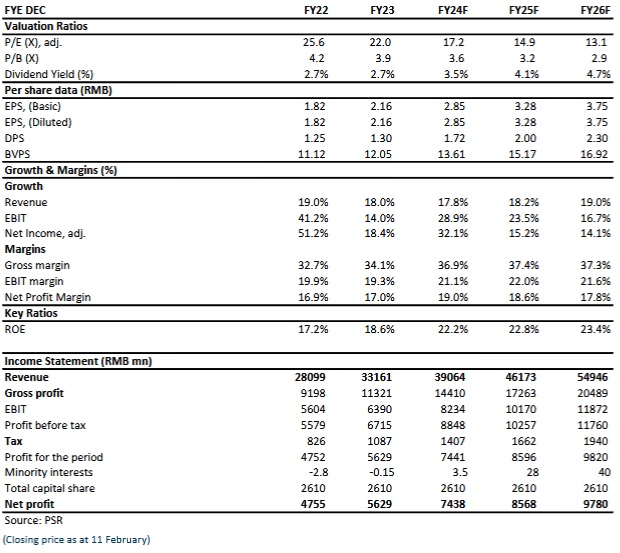

Financials

Click Here for PDF format...