Company profile

SMIC is one of the world's leading semiconductor foundries, as well as a leader in the semiconductor manufacturing industry in mainland China. It possesses advanced process manufacturing capabilities, production capacity advantages, and comprehensive service support, providing 8-inch and 12-inch wafer foundry and technical services to global customers. SMIC is headquartered in Shanghai, China, and has a global manufacturing and service base with multiple 8-inch and 12-inch wafer fabs in Shanghai, Beijing, Tianjin, and Shenzhen.

3Q24 performance exceeded previous guidance

In the third quarter, the company's revenue increased by 14% QoQ to $2.2 billion, reaching a single-quarter milestone of $2 billion for the first time, hitting a historic high. This growth was mainly driven by the release of 12-inch production capacity, which promoted further optimization of the product structure. At the same time, accelerated localization demand led to an increase in average selling prices. The company's overall capacity utilization rate increased to 90.4%, a 5.2% QoQ increase, effectively diluting unit depreciation costs. The gross profit margin rose to 20.5%, an increase of 6.6 percentage points QoQ. The company's net profit in the third quarter reached $149 million, a 58.3% YoY increase but a 9.6% QoQ decrease. Looking at the application areas, management indicated that the proportions for smartphones, computers and tablets, consumer electronics, IoT and wearables, industrial and automotive were 25.0%, 16.0%, 43.0%, 8.0%, and 8.0%, respectively. Demand in the consumer market is gradually recovering, with upgraded features being implemented in consumer products and strong demand for exports. In terms of customer regions, the revenue share of some overseas customers decreased by 6.0% QoQ in the third quarter, mainly due to a certain level of pull-in during the second quarter. Revenue in China increased by 6.0% QoQ, primarily driven by the acceleration of local demand and the overall good export demand, enabling Chinese customers to gradually enter the mid-to-high-end product markets.

4Q24 Outlook

The company forecasts that revenue in the fourth quarter will remain flat to grow by 2% QoQ, with a gross profit margin ranging from 18% to 20%. Considering that the fourth quarter is traditionally a slow season, the overall capacity utilization rate and shipments are expected to decrease slightly. Management states that by optimizing the product mix to increase the average selling price, they aim to ensure that fourth-quarter revenue is not significantly affected, leading to stable to slight QoQ growth, with the gross profit margin also staying relatively steady. The company expects to release approximately 30,000 additional 12-inch wafer capacity in the fourth quarter, but the validation of the new capacity will take time.

Favorable policies for smartphones and consumer electronics drive rapid capacity recovery

According to Canalys, global smartphone shipments reached 330 million units in the fourth quarter of 2024, a 3.0% YoY increase. Driven by the recovery on both the supply and demand sides, Canalys predicts a 3.0% recovery in global smartphone shipments to 1.2 billion units in 2024. Influenced by the growth in terminal sales of smartphones and the increasing willingness of mobile phone manufacturers to replenish stock, the prices of storage chips and memory chips may rise. At the same time, the government has introduced a series of policies to promote smartphone consumption.

In January 2025, the National Development and Reform Commission announced that it will implement subsidies for the purchase of digital products such as mobile phones, tablets, smartwatches, and smart wristbands, encouraging personal consumers to buy these digital products by providing subsidies. In terms of consumer electronics, in March 2024, the State Council issued the "Promotion of Large-Scale Equipment Updates and Consumer Goods Trade-in Action Plan", which provides subsidies for the purchase of green smart home appliances through the trade-in of old products.

In January 2025, the National Development and Reform Commission and the Ministry of Finance announced that they will implement subsidies for the purchase of digital products such as mobile phones. The subsidy for exchanging old mobile phones for new ones will not exceed 500 yuan per device, while for household appliances, the subsidy will be extended from 4 categories to 12 categories, with a maximum subsidy limit of 2000 yuan per device. Therefore, we expect a further increase in wafer shipments.

The foundry industry is expected to enter a period where capital expenditure transforms into effective capacity gains

Recently, there has been a frontloading of semiconductor equipment spending in the industry, mainly due to data from the Semiconductor Equipment and Materials International (SEMI) showing that the global semiconductor manufacturing equipment sales reached a total of $106.3 billion in 2023, with mainland China accounting for 34.4% of this amount. SEMI predicts that China's semiconductor equipment procurement expenditure is expected to surpass $40 billion in 2024. However, as demand returns to normal in 2025, there will be a decline in demand in the Chinese semiconductor equipment market.

According to the third-quarter 2024 financial report of the Dutch semiconductor equipment giant ASML, mainland China remained ASML's largest market in that quarter, accounting for 47% of net system sales. However, ASML's management expects that the sales amount in the Chinese market in 2025 may return to around 20% of the normal level. Considering the company's two capital expenditure increases in 2022 and 2023 and the management's expectation of stable capital expenditure in 2024 compared to 2023, we believe that the company's capital expenditure growth will be smaller in 2025 and will translate into effective capacity. The management stated that in the current situation of excess capacity, orders are tied to corresponding customers, and industry capacity growth in 2025 is expected to be minimal.

Company valuation

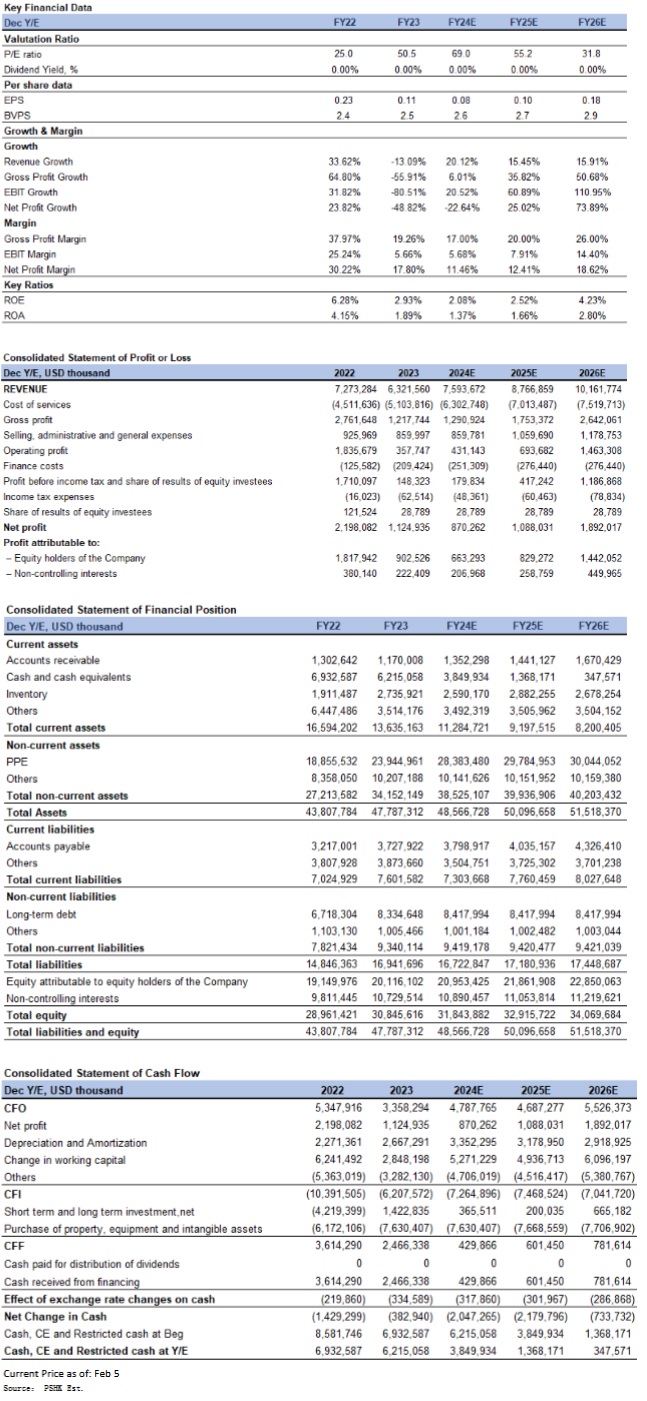

Taking into account the recovery in consumer electronics terminal demand, the management expects to drive revenue growth through the optimization of the product mix. We expect the company's revenue for the years 2024, 2025, and 2026 to be $7.6 billion, $8.8 billion, and $10.2 billion respectively. The net profit attributable to shareholders is estimated to be $66.3 million, $82.9 million, and $144.2 million respectively, corresponding to diluted EPS of $0.08, $0.10, and $0.18 respectively. Overall, as a leading company in the wafer foundry segment, we believe that the company's fair valuation slightly exceeds one standard deviation above the historical average NTM P/B ratio, at 2.1x 2025 PB, corresponding to a target price of HK$44.8 per share. We are initiating coverage with a "Neutral" rating.

Exchange rate: HKD/USD=7.79

Risk factors

1) Tightening of U.S. export controls; 2) Lower-than-expected ramp-up of capacity at the Wuxi wafer fab; 3) Weaker-than-expected increase in ASP.

Financials

Click Here for PDF format...