Sectors:

TMT, Semiconductors, Consumer & Healthcare (Eric Li)

Automobile & Air (Zhang Jing)

TMT, Semiconductors (Megan Tao)

Utilities, Commodity, Shipping& Banking (Margaret Li)

TMT, Semiconductors, Consumer & Healthcare (Eric Li)

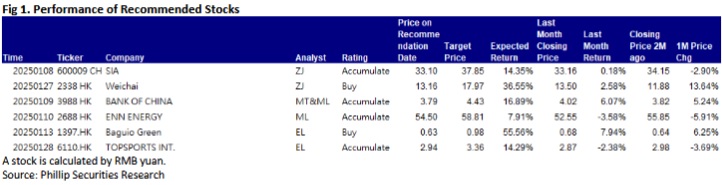

This month I released reports of Baguio Green (1397.HK) & TOPSPORTS INT. (6110.HK)

During the first half of 2024, Baguio delivered strong financial results, supported by growth across its major business segments. Revenue increased by 16.6% yoy to HK$1.291 billion, underpinned by a 20.1% surge in cleaning services revenue, which contributed 80.2% of total revenue, reaching HK$1.035 billion. This solid growth reflects the Company's success in securing new government contracts and expanding its service coverage. Additionally, the waste management and recycling segment recorded a 7.4% increase in revenue to HK$147.3 million, with its gross margin improving significantly by 4.2 percentage points to 12.9%, driven by the maturity of the "Plastic Recycling Pilot Scheme" and the addition of new recycling points under government contracts.

Gross profit rose by 12.4% to HK$97.07 million, despite a slight decline in the overall gross margin from 7.8% to 7.5%, mainly due to higher labor costs in the cleaning segment. This impact was mitigated by the improved profitability of the waste management and pest control segments, highlighting Baguio's ability to balance risks through its diversified business portfolio.

On cost management, administrative expenses remained well-controlled, with their share of total revenue decreasing to 4.8%. The Company also exhibited a healthy financial position, with its current ratio improving from 1.2x at the end of 2023 to 1.3x as of June 30, 2024. Bank borrowings decreased significantly by 47.5% year-on-year, and cash and bank balances surged by 84.3% to HK$76.3 million, reflecting improved liquidity and reduced financial leverage.

Financially, Baguio's contracts on hand as of June 30, 2024, reached HK$4.6 billion, with HK$1302 million scheduled for recognition by the end of 2024 and HK$3297 million to be recognised over the next two years.

Automobile & Air (Zhang Jing)

This month I released reports of SIA.( 600009 CH) & Weichai (2338 HK).

In the first three quarters of 2024, Shanghai International Airport reported operating revenue of RMB9.19 billion, up 16% yoy, and net profit attributable to the parent company of RMB1.2 billion, up 142% yoy. The growth in operating revenue was mainly driven by the low base effect resulting from the pandemic overpeak in the first quarter of last year, and the increase in the Company's aviation revenue, benefiting from the ongoing restoration of operational performance, which, however, was partially offset by a decline in non-aviation revenue due to a cut in the sales commission rate for duty-free goods. Compared with the pre-pandemic level, the Company's revenue restored to 112% of the same period in 2019, but the net profit attributable to the parent company lagged far behind at only 30%.

In the first three quarters, the Company's air passenger markets experienced a rapid recovery and sustained strong growth. Owing to the sharp rebound of international routes, the aircraft movements, passenger throughput and cargo and mail throughput of Shanghai Pudong International Airport ("Pudong Airport") increased by 27.1%, 48.8% and 11%, respectively, reaching 103%, 99.6% and 105% of the same period in 2019. Specifically, domestic routes saw the sharpest rebound, with aircraft movements, passenger throughput and cargo and mail throughput up by 9.4%, 22.5% and 25.6% yoy, respectively, reaching 117.7%, 119.8% and 101.7% of the same period in 2019; international routes recorded higher growth rates, with aircraft movements, passenger throughput and cargo and mail throughput up by 85.6%, 150% and 10.2% yoy, respectively, reaching 88.6%, 81.6% and 106.7% of the same period in 2019. Shanghai Hongqiao International Airport ("Hongqiao Airport") maintained rapid growth on last year's high base, with aircraft movements, passenger throughput and cargo and mail throughput up by 3.2%, 14.5% and 22.3% yoy, respectively. In the first three quarters, the total passenger throughput of the two airports reached 93.43 million, with international routes contributing 22.3% (34.7% at Pudong Airport and 6.5% at Hongqiao Airport).

In Q3 2024, the Company saw only RMB267 million of revenue from duty-free contracts, down 49.62% yoy, mainly because revisions to the duty-free agreement with China Duty Free ("CDF") made at the end of 2023, which adjusted the calculation method and lowered the proportion of the minimum monthly sales commission from 42.5% to 18% to 36% according to the status quo of sales of duty-free goods at airports. In Q1 and Q2, revenue from duty-free goods totaled RMB347 million and RMB301 million, respectively, showing a quarterly decline. The downturn in the consumption environment was the primary cause.

In the new winter-spring flight season in 2024, Pudong Airport's domestic passenger flight volume is expected to remain stable, while international, Hong Kong, Macao and Taiwan flights are anticipated to grow by approximately 5.2% yoy. 35 new intercontinental passenger destinations and more frequent flights to Los Angeles, London, Sydney, Melbourne, Brisbane, Egypt and Cairo are scheduled. The Company expects international traffic to continue growing, driving further improvements in business results through the growth of both aviation and non-aviation revenue. In the medium and long run, the Company will gain leverage in price negotiations for duty-free goods and eventually restore its valuation through the growth of international traffic, supported by the economic advantages of being located at the heart of the Yangtze River Delta and capacity expansion following the completion of Phase IV Pudong Airport Scale-up Project. However, it shall wait for and observe the recovery of consuming capacity in the short run.

We expect the net profit attributable to the parent company for 2024-2026 to be RMB 17.8/24.4/29.12 billion, EPS to be RMB 0.72/0.98/1.17yuan, and EBITDA per share to be RMB 2.36/2.71/2.96yuan. Correspondingly adjust the target price to RMB 37.85 (originally RMB 64.5), corresponding to P/EBITDA per share multiples of 16/14/12.8 x, and the "Accumulate" rating is given.

In accordance with the reports of Weichai Power for the first three quarters: The Company's revenue grew by 1.0% year on year to RMB161.95 billion from January to September 2024. The net profit attributable to the parent company stood at RMB8.4 billion with a yoy growth of 29.2%. The basic earnings per share was RMB0.97, compared to RMB0.75 in the same period of the previous year. By quarter, the Company's revenue was RMB56.38 billion (up 5.5% yoy) in Q1, RMB56.11 billion (up 6.5% yoy) in Q2, and RMB49.46 billion (down 8.8% yoy) in Q3, and the net profit attributable to the parent company was RMB2.6 billion (up 40.1% yoy), RMB3.3 billion (up 61.7% yoy) and RMB2.5 billion (down 4.0% yoy), respectively. The strong performance in Q1 and Q2 was largely driven by high demand for heavy-duty CNG vehicles, which significantly boosted the Company's sale of natural gas engines. However, in Q3, performance declined, primarily due to the volatility in the heavy-duty CNG vehicle sector, which impacted the sale of high-margin natural gas engines. Additionally, consumers` hesitation ahead of the release of the specific trade-in policy also contributed to the decline.

According to the statistics from the China Association of Automobile Manufacturers (CAAM), domestic sales of heavy-duty trucks totaled 683,000 units in the first three quarters of 2024, representing a yoy decrease of 3.3%. In Q3 alone, sales reached 178 thousand units, marking a yoy decrease of 18.2%. Accordingly, the Company's revenue growth rates in Q1 and Q2 were +1.0% and -8.8%, respectively, with a net profit growth rate of +29.2% and -4.0%, respectively, all outpacing the industry performance. This was largely driven by the Company's strategic focus on off-road engines, particularly large-cylinder models, which, alongside its involvement in the heavy-duty truck industry chain, helped cushion the cyclical fluctuations in the heavy-duty truck sector.In terms of profitability, the Company's gross margin and net profit margin in the first three quarters of 2024 were 21.9% and 6.4%, respectively, representing a yoy increase of 1.6ppts and 1.4ppts, showing a steady upward trend with improvements. This was primarily driven by the enhanced profitability of the Company's subsidiaries, Shaanxi Heavy Duty Automobile and KION, as well as the successful implementation of supply chain optimization and cost reduction and efficiency improvement across various processes.

At the policy level, the new trade-in policy introduced at the beginning of 2025 further expands its coverage and scale compared to its 2024 version. It extends the scope of the scrapping and renewal subsidy to include commercial trucks that meet or fall below the China IV vehicle emission standard. For a new energy heavy-duty truck, the sum of the scrapping subsidy and the new purchase subsidy may be up to RMB140,000, and for a heavy-duty truck meeting the China VI vehicle emission standard, it may reach up to RMB110,000. We expect that, with the support of the said policy, the potential demand for vehicle replacements will drive a rebound in heavy-duty truck sales, and the Company will benefit directly as a leader in heavy-duty truck engines. In the mid-run, the positive fiscal and monetary policy stimulus, alongside the upcoming upgrade of emission standards in the industry, is expected to boost heavy-duty truck sales.

Meanwhile, fueled by the soaring demand for backup power engines in large data centers, large-cylinder engines are experiencing a period of rapid growth. The Company's large-cylinder engine business has begun to take shape. In an on-site acceptance test by a renowned Internet company in October 2024, the Weichai 2,000kW high-voltage generator set successfully ran for 242 hours with zero faults. It is expected to become the Company's another key growth driver in the future. We forecast the EPS of the Company to be RMB 1.29/1.54/1.73yuan in 2024/2025/2026. We will also revise target price to 17.97 HKD (13.1/11.0/9.8x P/E and 1.7/1.6/1.4x P/B for2024/2025/2026) and BUY rating.

TMT, Semiconductors (Megan Tao)

This month I released 1 initiation reports of BANK OF CHINA¡]3988.HK¡^jointly with Margaret Li.

In the first three quarters of 2024, the company achieved operating income of 479.1 billion yuan, a year-on-year increase of 1.74%; the after-tax profit was 187.5 billion yuan, a year-on-year growth of 0.53%; the net profit attributable to the parent company reached 175.8 billion yuan, a year-on-year increase of 0.52%; and the basic earnings per share were 0.55 yuan.

In the first three quarters of 2024, the company's net interest income was 336.0 billion yuan, a year-on-year decrease of 4.81%, mainly due to a slight decrease in net interest margin to 1.41% compared to the first half of the year. This was because the Federal Reserve entered a rate-cutting cycle, reducing the contribution of foreign currencies to the net interest margin. Factors such as the future reduction of mortgage rates and the Loan Prime Rate (LPR) will continue to exert pressure on domestic asset yields, but the slowdown in the Fed's rate cuts may improve the pressure on overseas asset yields. The company's non-interest income was 143.1 billion yuan, a year-on-year increase of 21.32%, indicating strong growth in non-interest businesses. Among them, the net fee and commission income was 60.7 billion yuan, a year-on-year decrease of 3.93%, narrowing the decline compared to the first half of 2024, mainly affected by capital market fluctuations; other non-interest income (mainly including net trading gains, net gains on financial asset transfers, and other operating income) totaled 82.4 billion yuan, a year-on-year increase of 50.43%, mainly due to a 114.2% increase in investment income. The company's operating expenses were 172.7 billion yuan, a year-on-year increase of 10.13%. The company's asset impairment losses were 85.8 billion yuan, a year-on-year decrease of 5.78%, with credit impairment losses amounting to 85.7 billion yuan, a year-on-year decrease of 5.86%.

The company's dividend yield over the past 12 months was 6.84%, indicating a high dividend feature. The company maintains a leading global advantage, with overall stable fundamentals. Considering that non-interest income growth is slightly better than previous expectations, we are optimistic about the company's medium to long-term growth. However, considering the significant impact of RMB depreciation risk on Hong Kong stocks and the fact that the company's main customers are real economy enterprises, performance may be affected by U.S. tariffs. Therefore, we predict that the company's net profit attributable to the parent company for 2024-2026 will be 236.8/240.8/249.4 billion yuan, with forecasted EPS of 0.75/0.77/0.80 yuan respectively. The current stock price corresponds to PB ratios of 0.44/0.41/0.38x. Overall, we give the company a PB ratio of 0.5 for 2024, corresponding to a target price of 4.43 Hong Kong dollars per share, and rate it as "Hold."

Utilities, Commodity, Shipping& Banking (Margaret Li)

This month I released 2 initiation reports of ENN ENERGY (2688.HK).& BANK OF CHINA¡]3988.HK¡^.

ENN ENERGY (2688.HK) is one of the largest clean energy distributors in China. Its main business includes investing, constructing, operating and managing gas pipeline infrastructure in China, selling and distributing pipeline gas, liquefied natural gas and other multi-category clean energy products and providing customers with digital intelligence services related to low-carbon overall solutions and the development of diversified value-added business based on customer needs. As of June 30, 2024, the company operated 260 urban gas projects which covered a population of 140 million.

The company had made full-year guidance for each business. Retail gas volume will increase by 5%, new industrial and commercial opening gas volume will be 12-14 million cubic meters per day, retail gas business gross profit will increase by 10%+; integrated energy sales volume will increase by 20%-30% and gross profit will increase by 20%-30%; gross profit of value-added business will increase by 20%-30%. On December 25,2024, the National Development and Reform Commission released the National Natural Gas Operation Express Report for November 2024. According to the statistics, in November 2024, the apparent consumption of natural gas nationwide was 34.86 billion cubic meters with a year-on-year decrease of 0.5%. From January to November 2024, the apparent consumption of natural gas nationwide was 388.57 billion cubic meters with a year-on-year increase of 8.9%. China Petroleum Economics and Technology Research Institute predicts that China's natural gas demand will continue to grow in the future, and China's natural gas demand will be 610 billion cubic meters in 2035. In 2023, the National Development and Reform Commission issued the "Guiding Opinions on Establishing and Improving the Upstream and Downstream Price Linkage Mechanism for Natural Gas." Under this guidance, different cities have continuously introduced and improved local natural gas upstream and downstream price linkage mechanisms based on the development of the local natural gas industry and economic conditions and have launched or accelerated price linkage reforms. The company has actively followed the reform trend and promoted price adjustments for residents. As of the end of July 2024, the company's cumulative completion rate for gas price adjustment was approximately 59% of residential gas volume. As the gas price gradually rationalizes, the company's performance will gradually improve. Since 2024, the Ministry of Commerce has taken the lead in the implementation of the trade-in of old consumer goods, and various regions have also launched detailed implementation plans based on local conditions, which have achieved good results and greatly promoted consumer demand. The company has continuously improved core products and services, improved the operation system of its own brand Gratle, and standardized the process of serving households. In addition, it also upgraded its products through intelligentisation for scenarios such as safety, kitchen and community. With the further implementation of the old-for-new policy, the company's value-added business revenue is expected to continue to grow.

We predict that the company's operating income will be 118.09 billion yuan, 127.14 billion yuan and 136.98 billion yuan respectively in 2024-2026. EPS will be 6.16/6.44/6.91 yuan, corresponding to the P/E of 8.3x/8.0x/7.4x. It has now entered the peak winter natural gas demand season, which may make up for the impact of the company's summer sales decline. The company is given a P/E of 9 times in 2024, with a target price of HK$58.81, and our investment rating is " Accumulate ". (Current price as of Jan 6)

Click Here for PDF format...