Summary

Topsports International's interim results for 2024 highlight the significant impact of China's weak retail market on its business performance. Revenue declined by 7.9% year-on-year to RMB 13,054.7 million, while gross profit margin dropped from 44.7% to 41.1%. Profit attributable to equity holders fell by 34.7% year-on-year to RMB 873.8 million. Despite the challenges, the company demonstrated robust cash flow management, with operating cash inflows increasing by 2.5% year-on-year and cash and cash equivalents rising to RMB 2,839.6 million. The board declared an interim dividend of RMB 14.00 cents per share, representing a payout ratio of 99.4%, significantly higher than the 74.2% recorded in the prior year.

In response to market headwinds, Topsports actively implemented an omnichannel retail strategy by optimizing its offline store network, enhancing online operations, and improving inventory management. During the period, online sales accounted for 30% of total retail revenue, with livestreaming sales on the Douyin platform growing approximately 200% year-on-year. Looking ahead, the company remains focused on digital transformation and expanding into emerging markets such as outdoor sports and IP cultural segments to drive its next phase of growth. While short-term profitability remains under pressure, Topsports` solid financial foundation and flexible operational strategies provide a strong platform for sustainable long-term growth.

Revenue and Profitability Under Pressure, Cash Flow Stable

For the six months ended August 31 2024, Topsports` revenue declined by 7.9% year-on-year to RMB 13,054.7 million, primarily due to weak offline foot traffic and higher discounting in online channels. Inventory write-downs and changes in the business mix further compressed margins, with gross profit margin declining by 3.6 percentage points to 41.1%. Operating profit fell by 35.1% to RMB 1,120.9 million, while profit attributable to equity holders decreased to RMB 873.8 million, with net profit margin dropping from 9.4% to 6.7%.

Despite the revenue and profit challenges, the company displayed strong cost control. Selling and distribution expenses, as well as general and administrative expenses, fell by 7.4% year-on-year. However, due to lower operating leverage from declining offline traffic, the expense ratio slightly increased by 0.2 percentage points to 33.1%.

Cash flow remained a bright spot during the period. Operating cash inflows rose by 2.5% year-on-year to RMB 2,613.5 million, representing 3x the profit attributable to equity holders. At the end of the period, cash and cash equivalents increased to RMB 2,839.6 million, underscoring the company's strong cash management. Supported by this robust cash flow, the board declared an interim dividend of RMB 14.00 cents per share, reflecting a payout ratio of 99.4%, significantly higher than the 74.2% recorded in the prior year.

Omnichannel Retail and Digital Transformation

In response to declining offline traffic, Topsports has continued to optimize its store network by closing underperforming locations and focusing on high-performing stores for its core brands. As of August 31, 2024, the number of directly operated stores decreased by 6.4% year-on-year to 5,813, while the total sales area declined by 1.9%. This store rationalization strategy has effectively mitigated the negative impact of low-efficiency assets on profitability, highlighting the company's focus on operational efficiency.

On the digital front, Topsports has aggressively expanded its online operations, leveraging a comprehensive omnichannel strategy that includes platform e-commerce, content-driven e-commerce, and private-domain traffic management. During the period, the number of mini-program stores expanded significantly, while livestreaming sales on Douyin grew approximately 200% year-on-year. Online sales accounted for 30% of total retail revenue, demonstrating the company's ability to capitalize on growth opportunities in the digital space.

In terms of inventory management, the company adopted a ¡§one inventory¡¨ strategy to improve stock turnover efficiency. As of August 31, 2024, inventory levels decreased by 2.6% quarter-on-quarter to RMB 6,119.9 million, signaling gradual relief from inventory pressure. Additionally, the company expanded its brand portfolio by partnering with HOKA ONE ONE, KAILAS, and Fanatics, further advancing into niche markets such as outdoor sports and IP-driven cultural products.

China's retail market remains under pressure in the short term. In the first half of 2024, GDP grew by 5.0% year-on-year, but social retail sales only increased by 3.7%, reflecting weak consumer confidence and spending power. The sportswear market is undergoing a shift from incremental growth to a more competitive, stock-driven environment. Offline channels are challenged by lower foot traffic, while online channels face intense competition and price wars, further squeezing margins.

Despite these challenges, the long-term growth potential of China's sportswear market remains intact, driven by rising awareness of health and fitness. Topsports is well-positioned to capture this growth opportunity, thanks to its leading position in omnichannel retail, digital transformation, and brand portfolio expansion, which are expected to serve as new growth drivers in the coming years.

Company valuation

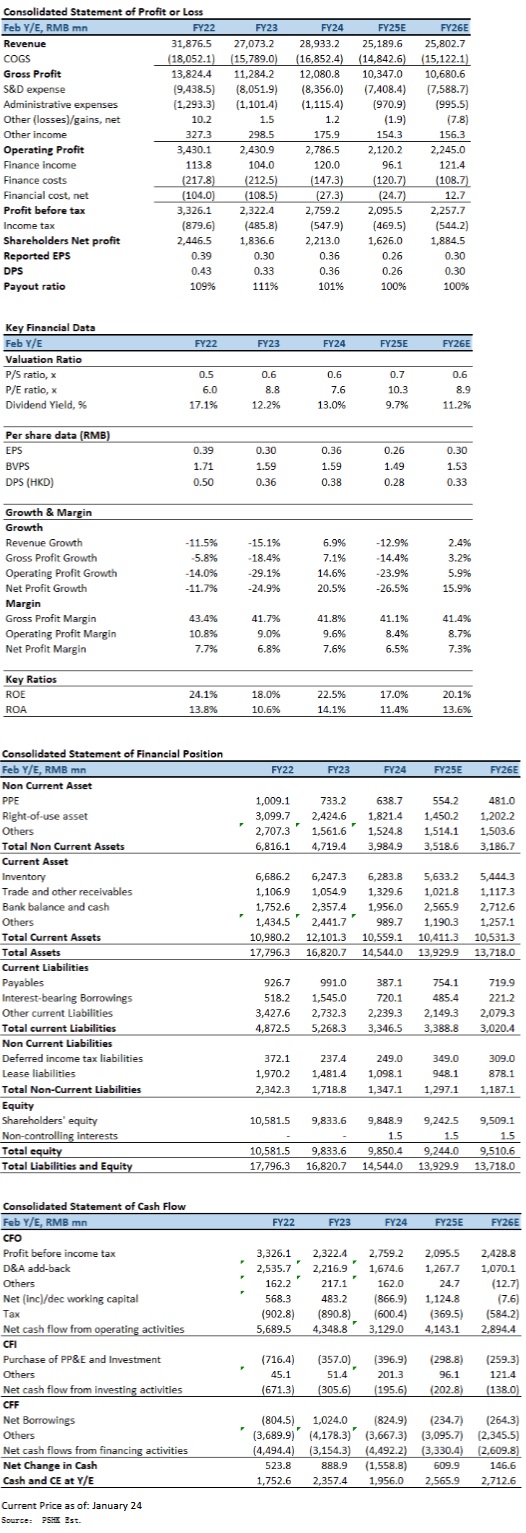

Topsports` short-term performance reflects the challenges posed by a weak consumption environment and intense industry competition. However, its strong cash flow and high dividend payout ratio make it an attractive option for defensive investors. The company's progress in digital transformation, inventory optimization, and brand expansion will be key to its future recovery. In view of the above impact, we expect FY2025E-FY2026E EPS to RMB 0.26 and RMB 0.30 respectively, with TP is HKD3.36, implies a FY2025E P/E of 11.8x (~2-yrs historical average). Our investment rating is ¡§Accumulate¡¨.

Risk factors

1) The pandemic has worsened more than expected; 2) Intensified competition in the industry; and 3) the slowdown in international brand sales is worse than expected.

Financial

Click Here for PDF format...