Company Profile

Weichai is one of the automobile and equipment manufacturing groups with the strongest comprehensive strength in China's heavy truck industry. Based on the powertrain system including engine, axle and gearbox, the Company extends upstream components and downstream heavy trucks, and takes the lead in forklifts and intelligent warehousing. After years of development, the Company has built a synergetic development pattern of four major industrial segments including powertrain (engine, transmission, axle/hydraulics), vehicle and machinery, intelligent logistics and other segments.

Investment Summary

Performance Review: Nearly 30% Increase in Profit in the First Three Quarters

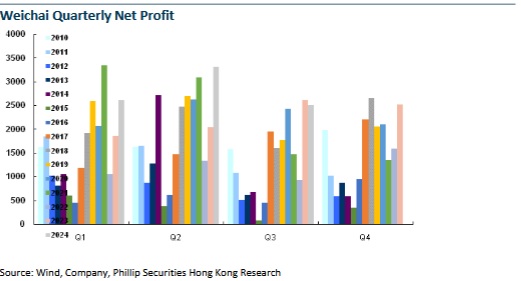

In accordance with the reports of Weichai Power for the first three quarters: The Company's revenue grew by 1.0% year on year to RMB161.95 billion from January to September 2024. The net profit attributable to the parent company stood at RMB8.4 billion with a yoy growth of 29.2%. The basic earnings per share was RMB0.97, compared to RMB0.75 in the same period of the previous year. By quarter, the Company's revenue was RMB56.38 billion (up 5.5% yoy) in Q1, RMB56.11 billion (up 6.5% yoy) in Q2, and RMB49.46 billion (down 8.8% yoy) in Q3, and the net profit attributable to the parent company was RMB2.6 billion (up 40.1% yoy), RMB3.3 billion (up 61.7% yoy) and RMB2.5 billion (down 4.0% yoy), respectively. The strong performance in Q1 and Q2 was largely driven by high demand for heavy-duty CNG vehicles, which significantly boosted the Company's sale of natural gas engines. However, in Q3, performance declined, primarily due to the volatility in the heavy-duty CNG vehicle sector, which impacted the sale of high-margin natural gas engines. Additionally, consumers` hesitation ahead of the release of the specific trade-in policy also contributed to the decline.

Performance Outpaces the Industry with Rising Profitability

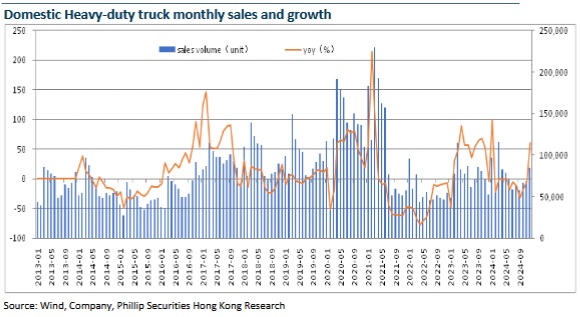

According to the statistics from the China Association of Automobile Manufacturers (CAAM), domestic sales of heavy-duty trucks totaled 683,000 units in the first three quarters of 2024, representing a yoy decrease of 3.3%. In Q3 alone, sales reached 178 thousand units, marking a yoy decrease of 18.2%. Accordingly, the Company's revenue growth rates in Q1 and Q2 were +1.0% and -8.8%, respectively, with a net profit growth rate of +29.2% and -4.0%, respectively, all outpacing the industry performance. This was largely driven by the Company's strategic focus on off-road engines, particularly large-cylinder models, which, alongside its involvement in the heavy-duty truck industry chain, helped cushion the cyclical fluctuations in the heavy-duty truck sector. In terms of sales volume, the Company sold 221 thousand heavy-duty truck engines in the first three quarters, including 89 thousand units for heavy-duty CNG trucks (a yoy increase of 8.8%), 42 thousand units for 6¡Ñ4 tractors with 500 horsepower or more (a yoy increase of 29%), and nearly 6 thousand large-cylinder units.

In terms of profitability, the Company's gross margin and net profit margin in the first three quarters of 2024 were 21.9% and 6.4%, respectively, representing a yoy increase of 1.6ppts and 1.4ppts. In particular, the Company recorded a gross margin of 22.11%, 21.39% and 22.12%, reflecting a yoy increase of 3.4ppts, 1.2ppts and 0.35ppts, respectively, in 2024Q1, Q2 and Q3, and a net profit margin of 5.93%, 7.18% and 6.00%, reflecting a yoy increase of 1.73ppts, 2.36ppts and 0.07ppts, respectively, showing a steady upward trend with improvements. This was primarily driven by the enhanced profitability of the Company's subsidiaries, Shaanxi Heavy Duty Automobile and KION, as well as the successful implementation of supply chain optimization and cost reduction and efficiency improvement across various processes. In the first three quarters, the sales expense ratio was 5.64%, down 0.34ppts yoy, the administration expense ratio was 4.66%, up 0.30ppts yoy, and the R&D expense ratio was 3.83%, up 0.31ppts yoy.

Optimistic about Policy-driven Sales Rebound and the Growth Potential of its Large-cylinder Engines

At the policy level, the new trade-in policy introduced at the beginning of 2025 further expands its coverage and scale compared to its 2024 version. It extends the scope of the scrapping and renewal subsidy to include commercial trucks that meet or fall below the China IV vehicle emission standard. For a new energy heavy-duty truck, the sum of the scrapping subsidy and the new purchase subsidy may be up to RMB140,000, and for a heavy-duty truck meeting the China VI vehicle emission standard, it may reach up to RMB110,000. We expect that, with the support of the said policy, the potential demand for vehicle replacements will drive a rebound in heavy-duty truck sales, and the Company will benefit directly as a leader in heavy-duty truck engines. In the mid-run, the positive fiscal and monetary policy stimulus, alongside the upcoming upgrade of emission standards in the industry, is expected to boost heavy-duty truck sales.

Meanwhile, fueled by the soaring demand for backup power engines in large data centers, large-cylinder engines are experiencing a period of rapid growth. The Company's large-cylinder engine business has begun to take shape. In an on-site acceptance test by a renowned Internet company in October 2024, the Weichai 2,000kW high-voltage generator set successfully ran for 242 hours with zero faults. It is expected to become the Company's another key growth driver in the future.

Investment Thesis

Overall, the Company's strategic framework of "Power + Hydraulics + New Energy" has been well-defined, its leading advantage continues to strengthen, and its dividend rate is expected to remain high.

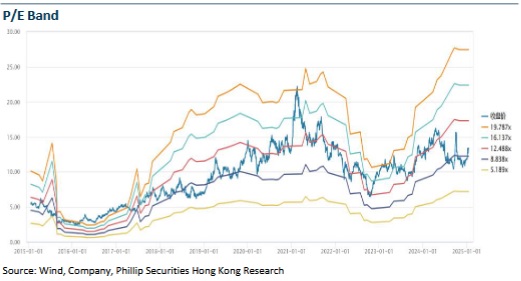

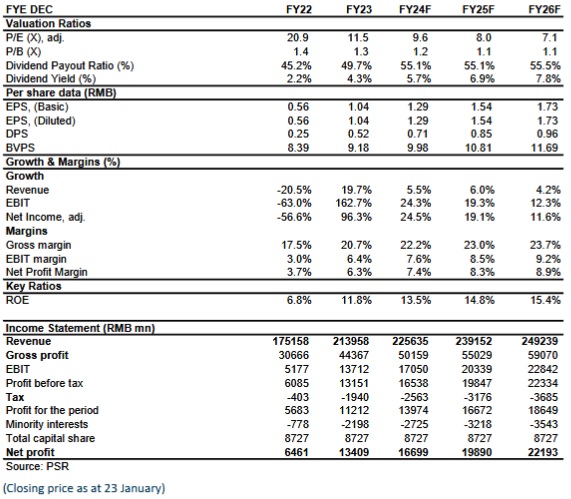

We forecast the EPS of the Company to be RMB 1.29/1.54/1.73yuan in 2024/2025/2026. We will also revise target price to 17.97 HKD (13.1/11.0/9.8x P/E and 1.7/1.6/1.4x P/B for2024/2025/2026) and BUY rating. (Closing price as at 23 January)

Financials

Click Here for PDF format...