Overview

ENN ENERGY (2688.HK) is one of the largest clean energy distributors in China. Its main business includes investing, constructing, operating and managing gas pipeline infrastructure in China, selling and distributing pipeline gas, liquefied natural gas and other multi-category clean energy products and providing customers with digital intelligence services related to low-carbon overall solutions and the development of diversified value-added business based on customer needs. As of June 30, 2024, the company operated 260 urban gas projects which covered a population of 140 million.

2024H1 Performance review

In the first half of 2024, the company's revenue was 54.59 billion yuan (RMB, the same below) with a year-on-year increase of 0.9%; gross profit was 6.47 billion yuan with a year-on-year decrease of 9.7%, mainly due to the reduction of international market opportunities, decline in gas wholesale business revenue and gross profit and the engineering installation business was dragged down by the weak domestic real estate situation; profit attributable to shareholders was 2.57 billion yuan with a year-on-year decrease of 22.8%; core profit was 3.26 billion yuan with a year-on-year decrease of 16.6%, of which domestic basic business was 3.08 billion yuan with a year-on-year increase of 9.5%, achieving solid growth. EPS was 2.29 yuan with a year-on-year decrease of 22.4%. The company's operating cash inflow was 3.27 billion yuan which was relatively stable, and its free cash flow amounted to 630 million yuan. The company has ample cash at hand and is actively repaying debt. An interim dividend of HK$0.65 per share was paid. The company began to pay dividends in 2004, and the dividend amount had been steadily increasing for most of the time.

In the first half of 2024, the company's gross profit from continuing business such as retail gas sales, integrated energy and value-added business accounted for 87.3% with a year-on-year increase of 8.6 percentage points, indicating that the company's profit quality continued to be optimized. The company has abundant customer resources, and the potential customers it can reach out and around the area covered by its operating rights are constantly growing thus there is still a lot of room for business development. The company's debt structure had been continuously optimized, effectively reducing the proportion of overseas debt and significantly reducing debt levels. Interest-bearing liabilities had been reduced to 19.83 billion yuan, compared with 21.92 billion yuan in 2023, and the comprehensive financing cost was 3.4%. Capex was 2.74 billion yuan with a significant year-on-year decrease of 20%, indicating that the company maintained a prudent investment strategy to ensure that the company had stable cash flow.

Q3 Operating situation

In the first three quarters of 2024, the company's retail gas volume was 18.82 billion cubic meters with a year-on-year increase of 4.8%, of which the industrial and commercial gas volume was 14.84 billion cubic meters with a year-on-year increase of 5.7%, and the civil gas volume was 3.75 billion cubic meters with a year-on-year increase of 3.4%; the new opening gas volume was 11.13 million cubic meters/day, the number of new household users was 1.10 million. The company's integrated energy sales volume was 29.67 billion kilowatt-hours with a year-on-year increase of 21.4%. The company has 347 integrated energy projects in operation and 59 integrated energy projects under construction, with a maximum energy consumption scale of more than 63.47 billion kilowatt hours. In the first three quarters, 643 new park projects, 332 new factory projects and 115 new construction projects were signed for the integrated energy business. In terms of value-added business, the company got 5.06 million e-city door-to-door service orders in the first three quarters with a year-on-year increase of 8.6%. The sales volume of smoke and heat stove mining products was 268,500 units with a year-on-year increase of 23.4%.

Investment Thesis

The company had made full-year guidance for each business. Retail gas volume will increase by 5%, new industrial and commercial opening gas volume will be 12-14 million cubic meters per day, retail gas business gross profit will increase by 10%+; integrated energy sales volume will increase by 20%-30% and gross profit will increase by 20%-30%; gross profit of value-added business will increase by 20%-30%. On December 25,2024, the National Development and Reform Commission released the National Natural Gas Operation Express Report for November 2024. According to the statistics, in November 2024, the apparent consumption of natural gas nationwide was 34.86 billion cubic meters with a year-on-year decrease of 0.5%. From January to November 2024, the apparent consumption of natural gas nationwide was 388.57 billion cubic meters with a year-on-year increase of 8.9%. China Petroleum Economics and Technology Research Institute predicts that China's natural gas demand will continue to grow in the future, and China's natural gas demand will be 610 billion cubic meters in 2035. In 2023, the National Development and Reform Commission issued the "Guiding Opinions on Establishing and Improving the Upstream and Downstream Price Linkage Mechanism for Natural Gas." Under this guidance, different cities have continuously introduced and improved local natural gas upstream and downstream price linkage mechanisms based on the development of the local natural gas industry and economic conditions and have launched or accelerated price linkage reforms. The company has actively followed the reform trend and promoted price adjustments for residents. As of the end of July 2024, the company's cumulative completion rate for gas price adjustment was approximately 59% of residential gas volume. As the gas price gradually rationalizes, the company's performance will gradually improve. Since 2024, the Ministry of Commerce has taken the lead in the implementation of the trade-in of old consumer goods, and various regions have also launched detailed implementation plans based on local conditions, which have achieved good results and greatly promoted consumer demand. The company has continuously improved core products and services, improved the operation system of its own brand Gratle, and standardized the process of serving households. In addition, it also upgraded its products through intelligentisation for scenarios such as safety, kitchen and community. With the further implementation of the old-for-new policy, the company's value-added business revenue is expected to continue to grow.

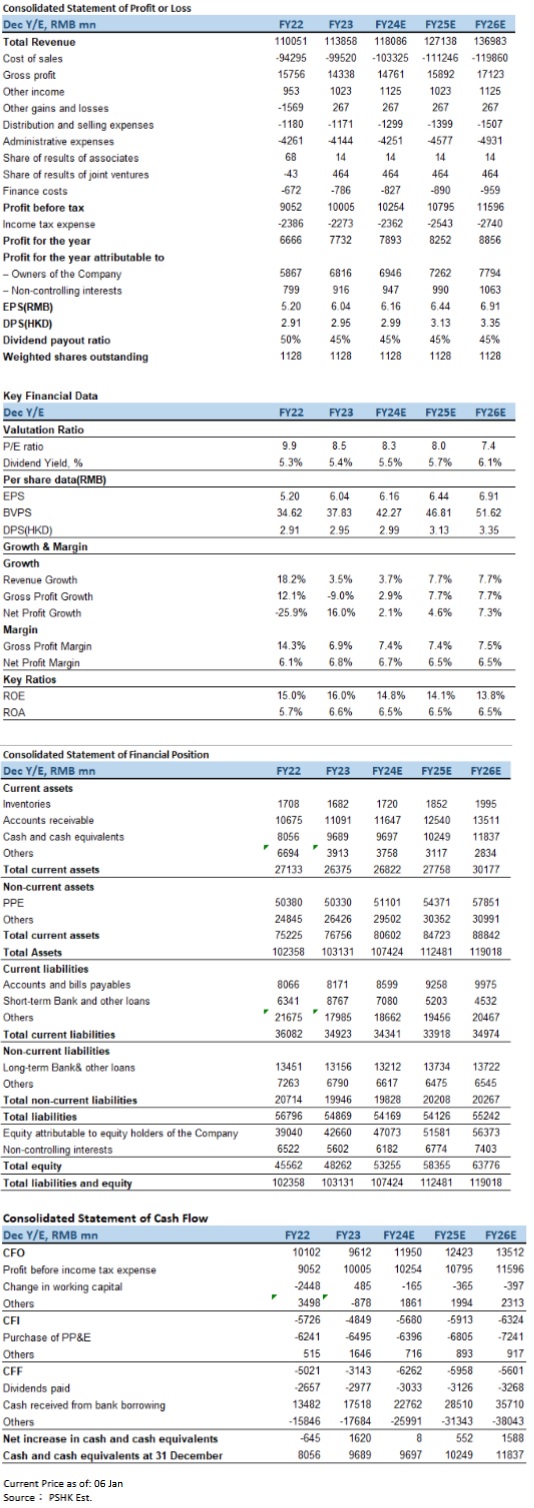

We predict that the company's operating income will be 118.09 billion yuan, 127.14 billion yuan and 136.98 billion yuan respectively in 2024-2026. EPS will be 6.16/6.44/6.91 yuan, corresponding to the P/E of 8.3x/8.0x/7.4x. It has now entered the peak winter natural gas demand season, which may make up for the impact of the company's summer sales decline. The company is given a P/E of 9 times in 2024, with a target price of HK$58.81, and our investment rating is " Accumulate ". (Current price as of Jan 6)

Risk factors

Supply and demand adjustments, real estate industry downturn, natural gas price fluctuations, and national policies.

Financial

Click Here for PDF format...