Investment Summary

Revenue Restored to 1.1 Times while Profit was Only 30% of Pre-pandemic Level

In the first three quarters of 2024, Shanghai Airport (Group) Company, Ltd. ("AVINEX" or the "Company") reported operating revenue of RMB9.19 billion, up 16% yoy, and net profit attributable to the parent company of RMB1.2 billion, up 142% yoy. The growth in operating revenue was mainly driven by the low base effect resulting from the pandemic overpeak in the first quarter of last year, and the increase in the Company's aviation revenue, benefiting from the ongoing restoration of operational performance, which, however, was partially offset by a decline in non-aviation revenue due to a cut in the sales commission rate for duty-free goods. Compared with the pre-pandemic level, the Company's revenue restored to 112% of the same period in 2019, but the net profit attributable to the parent company lagged far behind at only 30%.

International Routes Experienced Sharp Rebound, Driving Continued Restoration of Operational Performance

In the first three quarters, the Company's air passenger markets experienced a rapid recovery and sustained strong growth.

Owing to the sharp rebound of international routes, the aircraft movements, passenger throughput and cargo and mail throughput of Shanghai Pudong International Airport ("Pudong Airport") increased by 27.1%, 48.8% and 11%, respectively, reaching 103%, 99.6% and 105% of the same period in 2019. Specifically, domestic routes saw the sharpest rebound, with aircraft movements, passenger throughput and cargo and mail throughput up by 9.4%, 22.5% and 25.6% yoy, respectively, reaching 117.7%, 119.8% and 101.7% of the same period in 2019; international routes recorded higher growth rates, with aircraft movements, passenger throughput and cargo and mail throughput up by 85.6%, 150% and 10.2% yoy, respectively, reaching 88.6%, 81.6% and 106.7% of the same period in 2019.

Shanghai Hongqiao International Airport ("Hongqiao Airport") maintained rapid growth on last year's high base, with aircraft movements, passenger throughput and cargo and mail throughput up by 3.2%, 14.5% and 22.3% yoy, respectively.

In the first three quarters, the total passenger throughput of the two airports reached 93.43 million, with international routes contributing 22.3% (34.7% at Pudong Airport and 6.5% at Hongqiao Airport)..

Non-aviation Revenue Fell Significantly Alongside Revenue from Duty-free Goods

In the first three quarters of 2024, the Company recorded operating revenue of RMB3,127 million and net profit attributable to the parent company of RMB387 million, up 2.5% and 6.2%, respectively, and reaching 113.6% and 29.9% of the same period in 2019. In Q3, the combined aircraft movements, passenger throughput and cargo and mail throughput of Pudong Airport and Hongqiao Airport increased by 8.0%, 18.7% and 6.8% yoy, respectively, outpacing the growth in operating revenue. The significant fall in non-aviation revenue alongside revenue from duty-free goods was the primary cause. In Q3 2024, the Company saw only RMB267 million of revenue from duty-free contracts, down 49.62% yoy, mainly because revisions to the duty-free agreement with China Duty Free ("CDF") made at the end of 2023, which adjusted the calculation method and lowered the proportion of the minimum monthly sales commission from 42.5% to 18% to 36% according to the status quo of sales of duty-free goods at airports. In Q1 and Q2, revenue from duty-free goods totaled RMB347 million and RMB301 million, respectively, showing a quarterly decline. The downturn in the consumption environment was the primary cause.

Investment Revenue and Others Boosted Performance

In Q3, the profit margin on sales was 22.44%, up 0.7 ppts yoy, mainly due to the relatively stable operating cost that grew by only 1.55% yoy - lower than the 2.46% growth rate of revenue and much lower than the 18.7% growth rate of business volume. However, the gross margin remained well below the 51.68% recorded in the same period in 2019, largely due to a reduced sales commission rate for duty-free goods, disrupted duty-free channels at airports and weak consumption momentum. Comparatively, the administration expense ratio was 4.62% and the financial expense ratio was 4.75%, up 0.06 ppts and 0.41 ppts yoy, respectively, and the net profit ratio rose by 0.43 ppts yoy to 12.37%.

In Q3, the Company recorded investment revenue of RMB210 million, representing a yoy increase of 28%, which was driven by the yoy improvement in the operating benefit of several controlled or invested companies. In H1, the Company's investment revenue surged by 65% yoy to RMB360 million, with Uni-champion contributing RMB97 million (compared to a loss of RMB8.39 million in H1 2023) and Shanghai Pudong International Airport Aviation Fuel Supply Co., Ltd. contributing RMB120 million. On October 30, the Company released the Announcement on Matters Concerning Compensation for Property Expropriation, stating its intention to accept RMB689 million in compensation for property expropriation in monetary form. The time of fulfillment will depend on the completion of property delivery and relevant formalities.

Investment Thesis

In the new winter-spring flight season in 2024, Pudong Airport's domestic passenger flight volume is expected to remain stable, while international, Hong Kong, Macao and Taiwan flights are anticipated to grow by approximately 5.2% yoy. 35 new intercontinental passenger destinations and more frequent flights to Los Angeles, London, Sydney, Melbourne, Brisbane, Egypt and Cairo are scheduled. The Company expects international traffic to continue growing, driving further improvements in business results through the growth of both aviation and non-aviation revenue. In the medium and long run, the Company will gain leverage in price negotiations for duty-free goods and eventually restore its valuation through the growth of international traffic, supported by the economic advantages of being located at the heart of the Yangtze River Delta and capacity expansion following the completion of Phase IV Pudong Airport Scale-up Project. However, it shall wait for and observe the recovery of consuming capacity in the short run.

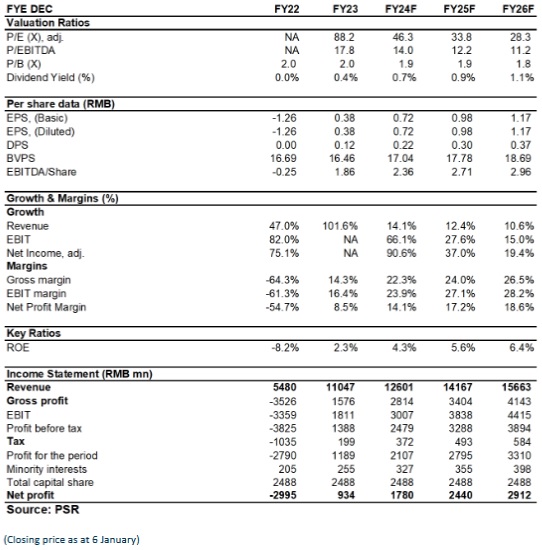

We expect the net profit attributable to the parent company for 2024-2026 to be RMB 17.8/24.4/29.12 billion, EPS to be RMB 0.72/0.98/1.17yuan, and EBITDA per share to be RMB 2.36/2.71/2.96yuan. Correspondingly adjust the target price to RMB 37.85 (originally RMB 64.5), corresponding to P/EBITDA per share multiples of 16/14/12.8 x, and the "Accumulate" rating is given. (Closing price as at 6 January)

Financials

Click Here for PDF format...