Company profile

Trip.com Group, founded in 1999, is a global leading one-stop travel platform that offers a comprehensive range of travel products, services, and differentiated travel content. The group provides over 1.2 million accommodation options worldwide, more than 480 international airlines, and over 310,000 destination activities. Its main operating brands include Trip.com, Qunar, Trip.com, and Skyscanner. The company offers one-stop travel services through Trip.com and Qunar, and provides travel product bookings for users outside of mainland China through Trip.com and Skyscanner. Currently, Trip.com holds a leading position in the online travel service market and is one of the top three online travel service companies globally in terms of market capitalization.

3Q24 performance: significant progress across all business lines, with outbound tourism surpassing 2019 levels

In 2024, outbound travel continued to be a key driving force for the advancement of China's tourism market. With international flight capacity roughly doubling and visa waiver policies further facilitating travel in the Asia-Pacific region, the company achieved total revenue of 15.9 billion yuan in Q3 2024, a year-on-year increase of 15.5%, primarily due to rising demand in domestic and outbound travel. In the third quarter, hotel and flight bookings on the international OTA platform Trip.com grew by over 60% year-on-year. Hotel and flight bookings in the outbound travel market have rebounded to 120% of 2019 levels. In terms of profitability, adjusted EBITDA reached 5.7 billion yuan, a year-on-year increase of 23.9%, while Non-GAAP net profit was 6 billion yuan, up 21.8% year-on-year. In terms of segment revenue, Q3 2024 accommodation booking revenue was 6.8 billion yuan, a year-on-year increase of 21.7%, driven by strong growth in domestic and outbound hotel business due to a reduction in hotel ADR decline; transportation ticketing revenue was 5.7 billion yuan, a year-on-year increase of 5.3%; travel vacation revenue was 1.6 billion yuan, up 17.3% year-on-year, mainly due to increased holiday travel demand; and business travel management revenue was 700 million yuan, a year-on-year increase of 11.0%, primarily due to the rising demand for corporate travel management services. Regarding expenses, total operating expenses for the quarter were 8.1 billion yuan, a year-on-year increase of 9.5%, which was lower than the revenue growth rate.

Domestic travel: online penetration rates have been increasing year by year, while the recovery of outbound travel has led to a redistribution of demand

According to the Ministry of Culture and Tourism, there were 4.9 billion domestic tourist visits in 2023, with total domestic travel spending reaching 5 trillion yuan, recovering to 81.4% and 85.7% of 2019 levels, respectively. Key holiday visitor numbers have fully surpassed pre-pandemic figures. In Q3 2024, the number of domestic trips increased by 15.3% year-on-year, and total tourism consumption in the first three quarters of 2024 grew by 17.9% year-on-year, reflecting a continued increase in service consumption and the ongoing release of compensatory travel demand.

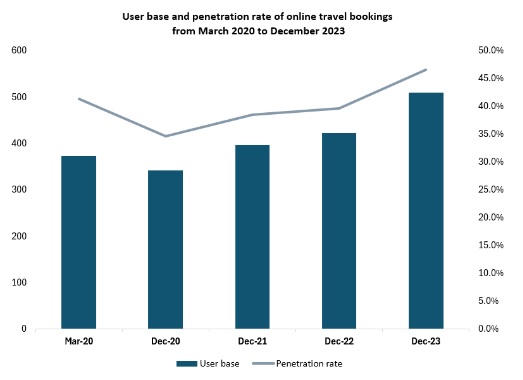

According to data from the China Internet Network Information Center, as of December 2023, the user base for online travel bookings reached 500 million, a year-on-year increase of 20.4%, accounting for 46.6% of all internet users. In the long term, online travel booking platforms possess strong consumer insights and supply chain integration capabilities, aligning with the changing trends in travel supply and demand. They are expected to timely offer travel product combinations that cater to local hotspots, thereby continuously enhancing the online penetration rate of travel product bookings.

Given the high resilience of travel demand, coupled with the steady increase in online travel booking penetration in the post-pandemic era and the evolving mindset of Chinese consumers toward seeking personalized and high-quality travel experiences, we anticipate further growth in the company's domestic travel business. At the same time, considering the rationalization of domestic consumption and the accelerating recovery of outbound travel leading to some redistribution of demand, we expect that overall hotel ADR will face challenges in achieving year-on-year increases against a high base, primarily influenced by the decline in industry-wide ADR and the increase in platform hotel supply.

Outbound Travel: business is expected to benefit from the recovery of flight capacity and the increased convenience of visa processing

In 2023, outbound travel showed a gradual recovery, with the number of outbound tourists returning to 56.0% of 2019 levels. Due to the continued recovery of international routes, mutual visa exemption agreements, and expedited visa processes, the Ministry of Culture and Tourism projects that the number of outbound trips will reach 130 million in 2024, a year-on-year increase of 49.0%, recovering to 84.0% of 2019 levels. Considering that outbound travel is still in the recovery stage, visa policies and flight capacity directly impact the growth or slowdown of outbound demand, while an increase in outbound demand helps to boost flight capacity. This interaction may lead to price decreases, further stimulating travel demand and creating a positive effect.

According to a report by Tongcheng Travel, during the summer vacation, outbound travel accounted for 21.6% of total trips, and during the National Day holiday, it accounted for 13.7%, significantly higher than during other holidays. It is anticipated that outbound travel will accelerate in the second half of the year. With the recovery of outbound travel, Trip.com Group, which holds a significant market share, is expected to benefit the most. Data from the Trip.com platform indicates that the number of visa applications in the second quarter doubled year-on-year in 2023, achieving a 20.0% increase compared to 2019.

Trip.com: incremental market growth driven by increased online penetration and travel revenue

In Q3 2024, total revenue for the international OTA platform Trip.com grew by approximately 60.0% to 70.0% year-on-year, contributing about 9.0% to overall revenue, with revenue from the Asia-Pacific market increasing by over 70.0%. Alongside the rising cross-selling ratio from transportation to hotels, hotel revenue's share surpassed 40.0%. In Q3 2024, mobile bookings on Trip.com accounted for 65.0% to 70.0% of total bookings globally, with the Asia-Pacific region exceeding 70.0%, highlighting how increased online penetration is driving incremental market growth.

Investment thesis

The company has established a comprehensive supply chain and fulfillment system targeting the mid-to-high-end customer segment to build competitive barriers, while deeply expanding its global OTA business. Coupled with ongoing cost optimization and AI innovations enhancing user experience, the online travel industry's operational ecosystem has significantly improved compared to pre-pandemic levels. The increase in online penetration, combined with the company's stable market share in domestic and outbound travel, is expected to accelerate short-term performance recovery.

In the medium term, domestic and outbound businesses are likely to provide a cash cow foundation for the company. Drawing reference from more proactive shareholder returns of leading overseas companies, the firm is expected to achieve strong valuation premiums during its steady growth phase. Trip.com is currently in a rapidly developing incremental market, with ample growth potential and a clear development path. The future integration of domestic and outbound travel is anticipated to create effective synergies, further solidifying the company's leading position.

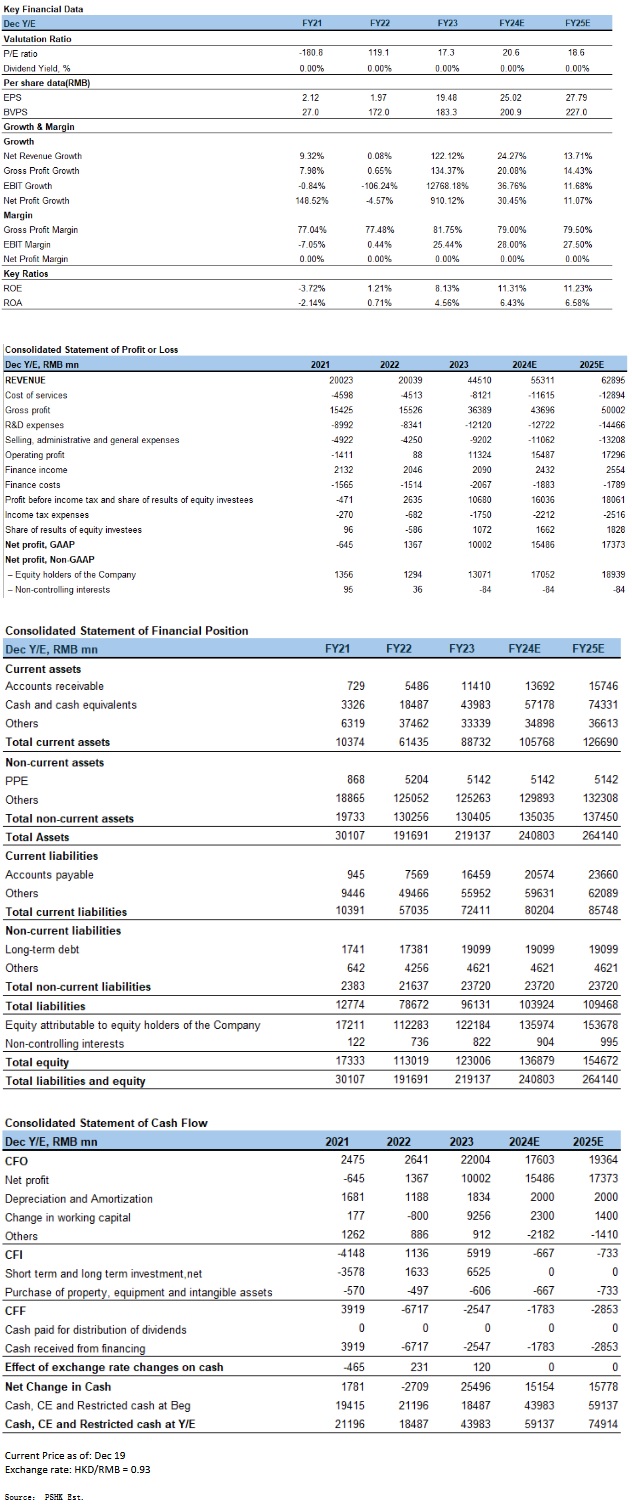

Therefore, we forecast the company's operating revenues for 2024 and 2025 to be 55.4 billion yuan and 63 billion yuan, respectively, with Non-GAAP net profits of 17.1 billion yuan and 18.9 billion yuan, corresponding to diluted EPS of 25 yuan and 28 yuan, and PE ratios of 21x and 19x.

We adopt domestic and international OTAs Booking, Expedia, Airbnb, and Tongcheng Travel as comparable companies. The industry average PE for 2025 is 20x, similar to the average PE of the past two years. Based on this, Trip.com Group's total target market value for 2025 is estimated to be 378.8 billion yuan, with a target price of 597.7 Hong Kong dollars, rated as `Accumulate`.

Risk factors

1) Domestic consumption demand is weaker than expected; 2) International business expansion is slower than anticipated; 3) Hotel ADR and airfare pricing pressures are greater than expected.

Financials

Click Here for PDF format...