Company profile

Tencent was founded in November 1998 and is currently one of China's largest comprehensive internet service providers. It is also one of the most widely used internet companies by Chinese service users. Tencent's communication and social services connect over 1 billion people worldwide, helping them stay in touch with family and friends and enjoy convenient travel, payment, and entertainment. Tencent has released a variety of globally popular electronic games and other high-quality digital content, providing rich interactive entertainment experiences for global users. Tencent also offers a range of enterprise services including cloud computing, advertising, and financial technology, supporting partners in achieving digital transformation and promoting business development.

Core business is making steady progress, and the ecosystem continues to be stable

In the third quarter of 2024, the company achieved a total revenue of 167 billion yuan. Compared to the same period last year, this represents an 8.1% increase. In terms of profitability, the unadjusted operating profit was 61 billion yuan, showing a growth of 18.6% year-on-year. The operating profit margin increased from 33.0% in the same period last year to 37.0%. The unadjusted profit for the period was 54 billion yuan, marking a 46.8% year-on-year growth.

Regarding departmental revenues, in Q3 2024, the gaming business revenue experienced strong growth, increasing by 12.6% year-on-year to 52 billion yuan. This growth was mainly driven by the steady performance of evergreen games globally and the contribution of new games with evergreen potential. Marketing services revenue grew by 16.7% year-on-year to 30 billion yuan, primarily due to strong demand from video accounts, mini-programs, and WeChat search. Fintech and business services business revenue increased by 2.1% year-on-year to 53 billion yuan, with a slight decrease in payment service revenue due to weak consumer spending.

Value-added services business: Evergreen games performed strongly, and social networks experienced healthy growth

Gaming business: In the third quarter of 2024, the company's gaming revenue increased by 12.6% year-on-year to 52 billion yuan. Among these, international market gaming revenue reached 15 billion yuan, up by 9.0% year-on-year, primarily driven by strong performances from games including "PUBG MOBILE" and "Wild Rift." "VALORANT" expanded from PC to PlayStation and Xbox, launching console versions in five key international markets, driving a revenue increase of over 30% year-on-year for the game. Domestic market gaming revenue grew by 14.1% year-on-year to 37 billion yuan, benefiting from healthy growth of flagship evergreen games like "Honor of Kings" and "Peacekeeper Elite," as well as game drivers including evergreen games like "Naruto" and "Fearless Agreement." Notably, with the introduction of new content and characters, "Naruto" surpassed 10 million monthly DAUs. We predict that the gaming revenue growth rate in the fourth quarter could reach 17.3%, mainly due to the strong user daily average usage time and retention rate performance of "Delta Operations," launched in September, and the income deferral cycle extension of some international market games will be reflected in the revenue of the coming quarters. Additionally, the company will launch Chinese New Year activities to further enhance user experience and game revenue.

Social network business: In the third quarter of 2024, the company's social network business revenue increased by 4.0% year-on-year to 31 billion yuan, mainly driven by the growth in virtual goods sales for mobile games, music subscription member revenue, and small game platform service fees, partially offset by declines in revenue from music live streaming and game live streaming services. Music subscription revenue increased by 20.0% year-on-year, primarily due to a 16.0% year-on-year growth in subscription numbers, reaching 119 million. During this period, the company improved its recommendation algorithms, expanded content supply, and upgraded audio quality.

Long video subscription revenue increased by 4% year-on-year. Benefiting from popular animations and TV dramas, video subscription numbers grew by 6.0% year-on-year, reaching 116 million. The QQ team comprehensively upgraded the platform's backend infrastructure and added and promoted new features such as Tencent Channel, AI Sketch, and Album Memories, driving a year-on-year increase in monthly active accounts for QQ's mobile terminals in the third quarter of 2024.

Marketing services business: Enhanced features bring different monetization opportunities and revenue growth

In the third quarter of 2024, the company's marketing services revenue increased by 16.7% year-on-year to 30 billion yuan, mainly driven by strong demand from advertisers for video accounts, mini-programs, and WeChat search inventory, as well as a modest one-time contribution from brand advertisements related to the Paris Olympics. Advertising spending in the gaming and e-commerce industries increased year-on-year, surpassing the reductions in spending in the real estate and food and beverage industries. By business type: 1) Video account advertising revenue in the third quarter increased by 60% year-on-year, mainly due to the systematic enhancement of WeChat's transactional capabilities, although the ad loading rate remained at 3-4%. 2) Mini-program marketing service revenue showed strong year-on-year growth, with mini-program GMV exceeding 2 trillion yuan in the third quarter, a growth of over 10% year-on-year. Game mini-programs and short video mini-programs provided high-value incentivized video ad inventory, generating incremental closed-loop demand. 3) WeChat search revenue more than doubled year-on-year, benefiting from increased commercial queries and improved click-through rates. The company leveraged LLM capabilities to enhance understanding of complex queries and content, improving the relevance of search results.

Fintech and Business services business: Macro environment remains a major influencing factor

In the third quarter of 2024, the company's fintech and business services revenue reached 53 billion yuan, a year-on-year increase of 2.1%. Management stated that the number of commercial payment transactions continued to grow at a healthy pace, increasing by approximately 10% year-on-year, although the average amount per transaction decreased. The decline in payment revenue was offset by the growth in wealth management service revenue. The number of users for wealth management and aggregated customer assets both increased year-on-year. Business services revenue in the third quarter grew year-on-year, benefiting from the growth in cloud service revenue and increased technology service fees due to the rise in e-commerce transaction volume. Due to increased contribution from higher-profit revenue streams and improved efficiency, gross profit margin for business services significantly increased within a year. Management indicated that the economic stimulus policies announced in October will take some time to impact the Chinese market, and they expect financial technology business revenue to remain stable in the fourth quarter.

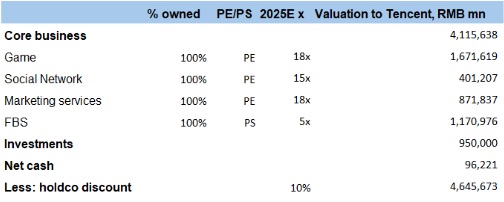

Company valuation

In terms of e-commerce business, management stated that since the end of September, Taobao has fully integrated with WeChat Pay, leading to an overall increase in e-commerce transaction volume and growth in payment revenue. Additionally, considering Tencent's strong user base in social networking services, the e-commerce business is expected to become a new growth node.

Regarding marketing services business, management mentioned that the ad loading for video accounts is still far below single-digit levels compared to peers. With the advancement of advertising technology and increased ad loading in the future, the company's advertising business is expected to continue outpacing industry growth.

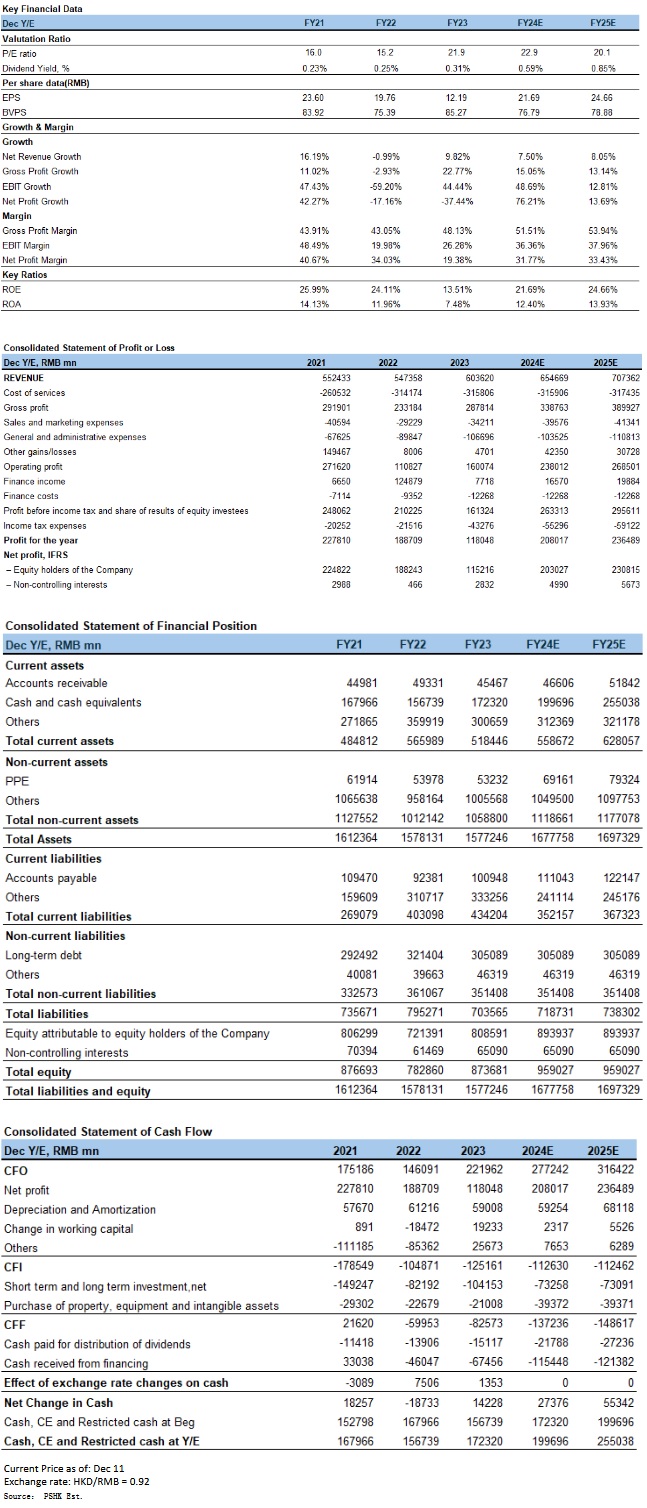

Overall, we are optimistic about the company's medium to long-term growth prospects. We expect the company's operating revenue for the years 2024 to 2026 to be 655/707/768 billion yuan respectively, and the unadjusted profits for the same periods to be 208/237/263billion yuan, corresponding to EPS of 21.7/24.7/27.5 yuan, and PE ratios of 22.9/20.1/18.1x. Based on the SOTP valuation method using the latest market values or valuations of subsidiaries and investee companies with a 10.0% discount, we assign a 2025 Tencent total target market value of 4.6 trillion yuan, corresponding to a target price of 496 yuan/540 HKD, and rate it as a "Buy".

Risk factors

1) Strict gaming regulations; 2) Weak macroeconomic environment; 3) Potential competitive threats from existing and emerging social platforms.

Financials

Click Here for PDF format...