Investment Summary

HKBN Ltd. (01310) faced multiple challenges during FY2024 (for the fiscal year ending August 31, 2024), including weak mobile sales and headwinds from the high-interest-rate environment. However, the company's core business performance remained resilient, particularly in EBITDA growth and operational efficiency improvements. Despite a revenue decline, HKBN managed to turn a profit, posting a net profit of HKD 10.277 million, primarily due to sustained cost management and growth in its core telecommunications business. The Board has proposed a final dividend of 16.5 HK cents per share, bringing the full-year dividend payout to 31.5 HK cents per share, reflecting the company's cash flow pressures and the impact of higher interest rates. Overall, HKBN is focused on maintaining steady dividends while enhancing shareholder value and pursuing long-term growth. Our investment rating is ¡§Accumulate¡¨, with PT of HKD5.05.

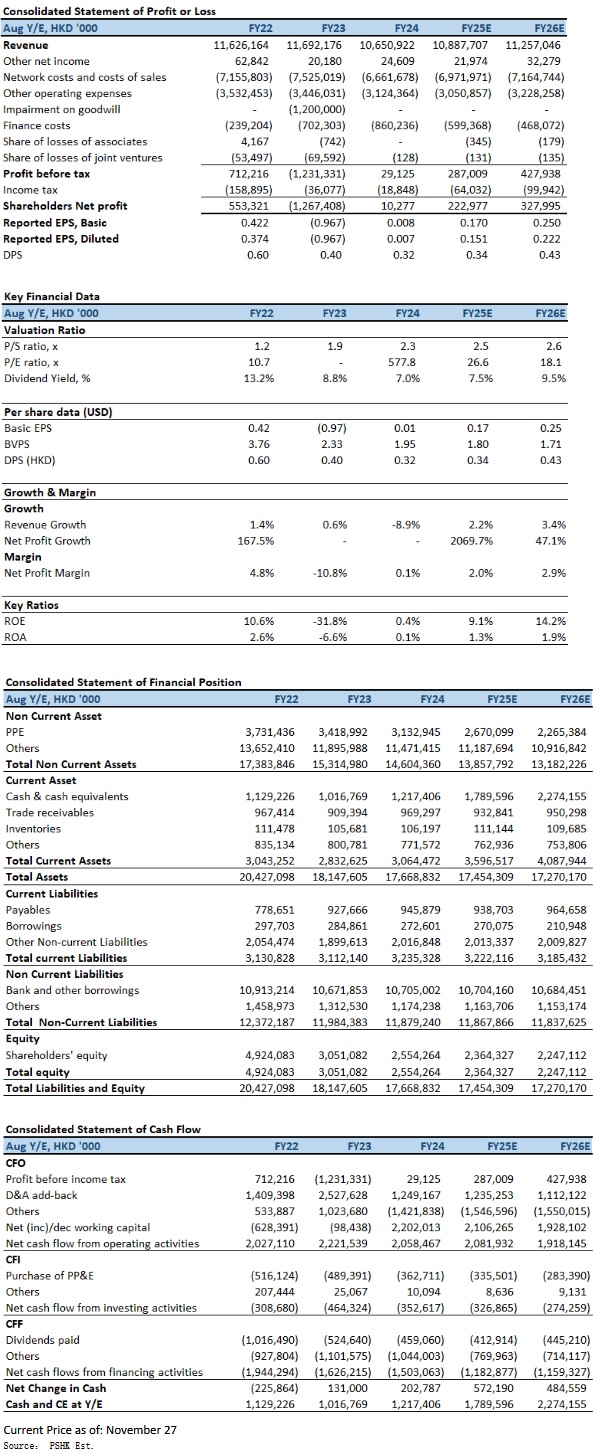

Total Revenue Decline, but Core Business Remains Solid

FY2024, HKBN reported a 9% year-on-year drop in total revenue to HKD 10.651 billion, mainly due to weaker-than-expected sales of mobile and other products. Excluding mobile sales, revenue only declined by 1%, demonstrating the stability of its core fixed telecommunications network services. Enterprise solutions revenue remained flat, although growth in the cloud and ICT services sectors provided some support.

EBITDA Growth and Improved Operational Efficiency

HKBN's EBITDA rose by 3% year-on-year to HKD 2.365 billion, with a particularly strong performance in the second half of FY2024, during which EBITDA grew by 11% year-on-year to HKD 1.214 billion. This reflects significant progress in cost control and capital expenditure management, particularly in driving growth in its Fixed Telecommunications Network Services (FTNS) and ICT solutions.

Return to Profitability

Compared to a loss of HKD 67 million in FY2023, HKBN recorded a net profit of HKD 10 million for FY2024. This positive shift was largely due to the absence of goodwill impairment and growth in its core business. Despite the challenging economic environment, HKBN has demonstrated adaptability and resilience. Adjusted free cash flow declined by 19% year-on-year to HKD 620 million, primarily due to a 41% increase in interest expenses in the high-interest-rate environment.

Enterprise Solutions business experienced a marginal year-on-year revenue decline of 1% to $6,675 million. However, the business has made notable progress in strengthening core business performance and recorded a 1% increase in enterprise services revenue ¡X excluding international telecommunications services. Residential Solutions business exhibited resilience in a highly competitive marketplace, experiencing a modest revenue decline of 2% to $2,344 million. This was a result of the company strategic focus on direct subscriptions while deliberately decelerating our resell business. Service revenue remained steady, which features major platforms like Netflix, Disney+, myTV SUPER, and iQIYI. This, in turn, contributed to a notable rise in ARPU, with residential ARPU rising by 2% to $182.

Growing Demand for Data and Enterprise Services

The global high-interest-rate environment has put pressure on HKBN's interest expenses, affecting its free cash flow. Additionally, competition in the telecommunications industry remains intense, particularly in the mobile and product sales segments, where the company faces significant challenges from other telecom operators. Despite weak mobile sales, enterprise demand for cloud services and data transmission continues to grow. HKBN has capitalized on this trend by expanding its ICT solutions and cloud services, strengthening its competitiveness in the enterprise market. The company's rollout of high-speed broadband services (e.g., 10Gbps to 25Gbps) is also meeting growing market demand for faster network speeds, which should support stable revenue growth in the future..

Investment Thesis

HKBN faced multiple challenges during FY2024, particularly from the high-interest-rate environment and declining mobile sales. However, the company's stable performance in its core business, as well as its expansion into ICT and cloud services, has laid a solid foundation for long-term growth. Given the potential investors of the company that has received non-binding proposals from China Mobile Hong Kong Company Limited, we expect FY2025E-FY2026E BVPS to be $1.80 and $1.71 respectively, with PT of HKD5.05, implies a FY2025E P/B of 2.44x (~the highest average price-to-book ratio in the past five years). Our investment rating is ¡§Accumulate¡¨.

Risk factors

1) The prolonged high-interest-rate environment could continue to pressure HKBN's financing costs; 2) Intensifying competition from telecom operators could further erode HKBN's market share; 3) Macroeconomic uncertainties could affect enterprise spending.

�Financial

Click Here for PDF format...