Investment Summary

BYD Took a Firm Lead by Achieving Exceptional Results in Q3

In the first three quarters of 2024, BYD recorded total revenue of RMB502,251 million, up 18.94% yoy, and net profit attributable to the parent company of RMB25,238 million, up 18.12% yoy. The basic ESP was RMB8.68, from RMB7.35 in the same period of the previous year. By quarter, the Company's net profit attributable to the parent company was RMB4.57 billion in Q1, RMB9,062 million in Q2 and RMB11,607 million in Q3, climbing by 10.62%, 32.8% and 11.47% yoy, respectively, and revenue was RMB124,944 million in Q1, RMB176,182 million in Q2 and RMB201,125 million in Q3, representing yoy growth rates of 3.97%, 25.89% and 24.04%, respectively..

BYD's Gross Profit Margin Recovered Notably Q-o-Q and R&D Input was Increased

In Q3, the Company's gross profit margin stood at 21.89%, the fifth highest since the Company's listing and representing a substantial qoq increase of 3.2 ppts, despite a slight yoy decrease of 0.23 ppts. The main reason lies in the optimised sales structure of the Company's models in Q3, in contrast to the fierce price competition in the auto market in Q2. The increased sales share of DM5.0 and the scale effect driven by lower raw material prices and expanding sales (sales volume in Q3 surged by 38% yoy and exceeded one million) significantly bolstered profitability.

In Q3, the sales expense ratio was 4.77%, up 0.83 ppts yoy as primarily driven by higher advertising and exhibition expenses and amortisation charges, and the administration expense ratio was 2.34%, up 0.21 ppts yoy. To maintain its competitive edge in battery technology and autonomous driving, the Company increased R&D input up to RMB13.7 billion, up 52% yoy and 23.4% qoq, representing an R&D expense ratio of 6.81%, basically flat with that of the same period of the previous year. The financial expense ratio rose by 0.58 ppts yoy to 0.48%, mainly due to the impact of exchange rate changes on exchange gains and losses. Excluding the performance of BYD Electronic, automobile business saw a growth rate of financial data basically the same as the overall growth rate, and a net profit attributable to the parent company of RMB10.59 billion, a yoy increase of 12.6% and qoq increase of 28.1%. This translated to a single-vehicle net profit of RMB9.3 thousand, reflecting a qoq increase of 7.3% as driven by the roll-out of the high-end DM-i 5.0 generation in the Company's Dynasty-series and Ocean-series, which boosted the average single-vehicle price and profit. However, on a year-on-year basis, the single-vehicle net profit fell by 17%, mainly because the Company introduced the lower-priced Glory edition to cope with the market's price war, resulting in a fall in the average single-vehicle price.

In Q3, the operating cash flow saw a net inflow of RMB42,095 million, up RMB26.2 billion yoy and RMB38.1 billion qoq. As at the end of September, the Company spent 71.9 days on inventory turnover and 38.0 days on accounts receivable turnover, representing a significant qoq improvement.

BYD is Anticipated to Further Boost Export and High-end Business, Powered by Strong Technological Strength

The Company has developed expertise in key technologies such as blade battery, 5th-generation DM technology, e-Platform 3.0, CTB body integration, Yisifang and BYD DiSus, and has constructed a hierarchical brand matrix composed of Dynasty, Ocean, Fangchengbao, Tengshi and Yangwang, ranging from passenger cars to premium cars and covering general and customised segments. The Company is ushering in a virtuous circle, with the rapid expansion of its product lines and the ongoing advancement of its high-end business that bolsters its competitiveness and influence in domestic and foreign markets. In May, the Company launched its 5th-generation DM technology, featuring upgrades to the power architecture, thermal management system and electronic and electrical systems, allowing for a minimum charge-sustaining fuel consumption of 2.9L/100km and a total range of up to 2,100 km. Models equipped with this technology, including Qin L, Seal 06, Song L, Song PLUS, Han, Sealion 05, Song Pro and Tang DM-i Modified, have been launched successively since May, further driving up the competitiveness and pricing of the Company's products. From January to October 2024, the Company sold 3,250 thousand vehicles, up 36% yoy. Specifically, domestic sales reached 2,920 thousand vehicles, up 32.5% yoy, while overseas sales surged to 329 thousand vehicles, up 86.9 yoy. Overseas sales accounted for 10.2% of total sales, representing a yoy increase of 2.7 ppts. Sold high-end brand models totalled 144 thousand vehicles with yoy increase of 39%, accounting for 4.5% of total sales, representing a yoy increase of 0.1 ppts. The upcoming launches of high-end models, such as Tengshi Z9 and Z9GT, Han L, Tang L, Fangchengbao 3, Fangchengbao 8 and Yangwang U7, and increase in overseas seals owing to the ramp-up of productivity abroad and positive expansion in Asian, African and Latin American markets (overseas sales are expected to surpass 450 thousand vehicles in 2024 and reach 800 thousand vehicles by 2025) will further contribute to the growth of Company's earnings..

Investment Thesis

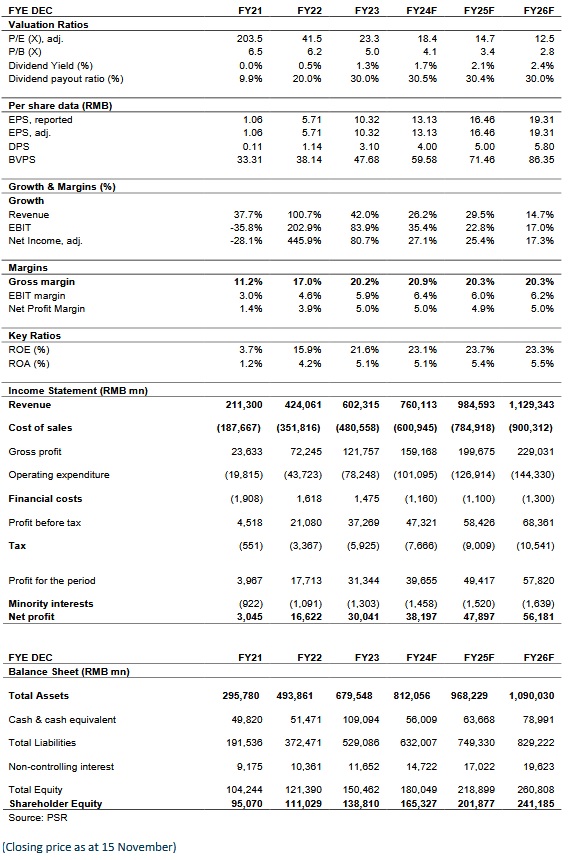

For valuation, we revised the EPS forecast for 2024/2025 to 13.13/16.46 yuan, and introduce 2026E EPS to 19.31 yuan. Therefore, we given the target price of 337 HK$, corresponding to 2024/2025/2026 23.5/18.8/16x P/E, BUY rating. (Closing price as at 15 November)

Risk

Sales of NEVs is not as good as expected

New business risk

Slow-down of Hand-set components business

Financials

Click Here for PDF format...