Sectors:

TMT, Semiconductors, Consumer & Healthcare (Eric Li)

Automobile & Air (Zhang Jing)

TMT, Semiconductors (Megan Tao)

TMT, Semiconductors, Consumer & Healthcare (Eric Li)

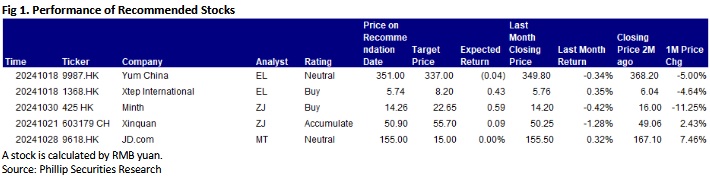

This month I released reports of Yum China Holdings, Inc.(9987) & Xtep International (1368.HK).

Yum China Holdings, Inc. (09987) is the largest restaurant company in China in terms of 2023 system sales, with 15,423 restaurants covering over 2,100 cities primarily in China as of June 30, 2024. Its growing restaurant network consists of our flagship KFC and Pizza Hut brands, as well as emerging brands such as Lavazza, Huang Ji Huang, Little Sheep and Taco Bell.

2Q2024FY, total system sales grew 4% YoY, excluding foreign currency translation ("F/X"), on top of last year's high base. The growth was primarily attributable to 8% of net new unit contribution. The Company opened 401 net new stores in the quarter. 99 net new stores, or 25%, were opened by franchisees. Total revenues increased 1% YoY to $2.68 billion, a record-high for the second quarter. Excluding F/X, total revenues would have been $85 million higher, or a 4% increase YoY. Same-store sales reached 96% of the prior year's level. Same-store transactions grew 4% YoY. Operating profit grew 4% YoY to $266 million, a record level for the second quarter. Excluding F/X, operating profit would have been $9 million higher, or a 7% increase YoY. Core operating profit grew 12% YoY to $275 million. OP Margin was 9.9%, an increase of 20 basis points YoY, supported by resilient restaurant margins and savings in G&A expenses. Restaurant margin was 15.5%. Excluding $12 million in items affecting comparability, restaurant margin was approximately the same as the second quarter last year. Improvement in operational efficiencies supported margin stability. Diluted EPS increased 17% YoY to $0.55, a record level for the second quarter, or up 19% YoY excluding F/X. Delivery sales grew 11% YoY, maintaining the double-digit growth Yum China has carried over the past decade. Delivery contributed ~38% of KFC and Pizza Hut's Company sales.

The Company's targets for the 2024 fiscal year remain unchanged from the prior period's disclosures. Open ~1,500 to 1,700 net new stores. Make capital expenditures in the range of approximately $700 million to $850 million. Return a Company record-setting $1.5 billion to shareholders through quarterly cash dividends and share repurchases.

Automobile & Air (Zhang Jing)

This month I released 1 update report of Minth (425.HK) and 1 initiation report of Xinquan (603179.CH).

Minth Group, in H1 of 2024, recorded a total revenue of RMB11.09 billion, up 13.78% yoy and 1.85% hoh. The net profit attributable to the parent company hit RMB1,068 million, up 20.4% yoy and 6% hoh. The main reason is the economies of scale driven by revenue growth, the continuous increase in the capacity utilization of the production line of battery house and the yoy increase in gross profit of each product line compared with 2023 due to the cost reduction and efficiency measures pushed by each product line. As a result, the Company generally maintained a good level of profitability.

During the Reporting Period, the gross margin was approximately 28.5%, up 2.2 ppts year on year. It was mainly driven by the increase in segment margin of plastic products and battery house by 2.0 ppts and 2.7 ppts, respectively. Specifically, the segment margin of the battery house business reached 20.6%, one step closer to the 25% target.

The Company continuously optimizes the operating efficiency of global factories. It has built "hub" central factories in various operating regions around the world, and established satellite factories around the hub factories, so as to achieve global capacity synergy and continuously improve the collaborative operation efficiency between various product lines. The Company continues to invest in R&D for innovative products and new materials including battery house, body and chassis structural parts, smart integrated exterior parts, hydrogen storage system, and storage and charging machine, and has gained multiple new business orders. Moreover, the development of new product tracks such as battery cell structural parts that have been laid out will drive the Company's long-term sustainable development.

Capital expenditure in H1 of the year fell 45.7% year on year to RMB1,093 million, and the full-year guidance is no more than RMB2.5 billion. After years of investment and construction of new business capacity (in particular, the layout of overseas factories), the Company has survived the stage of high investment and is expected to focus on equipment renewal and flexible transformation investment in the future. The Company's cash flow has also improved, with free cash flow going from negative (-RMB417 million) to positive (+ RMB637 million). It is expected to resume its suspended one-year dividend by the end of the year. Meanwhile, the Company has announced that it plans to use no more than HK$500 million for share repurchase, which conveys the confidence of the Management in the future development of the Company.

We slightly decreased the expected earnings per share for 2024/2025 to 1.97/2.35¡]from 2.17/2.53¡^, taking into account the pressure on the overall gross profit margin from new business during the ramp-up period.

We believe that it is reasonable to give the Company a valuation of 10.5/8.8/7.4x P/E and 1.2/1.1/1.0x P/B for 2024/2025/2026, equivalent to target price of HK$ 22.65 and BUY rating.

Xinquan, founded in 2001, offers a full range of interior and exterior trim assembly products for both commercial vehicles and passenger vehicles. The Company is capable of simultaneous development with OEMs.

Xinquan has realized mass production of trim products for key independent vehicle manufacturers, such as SAIC, Chang`an, Geely, GAC, BYD and Great Wall, since 2019, and in 2020, it became a supplier to Tesla, and started mass production of trim products for Tesla in 2021 In 2021, 2022 and 2023, the Company's operating income rose by 25.3%, 50.6% and 52.2% yoy to RMB4.61 billion, RMB6.95 billion and RMB10.57 billion, respectively, indicating its rapid business development. Tesla, Geely, Chery, Li and BYD were the Company's top five clients in 2023, contributing 22%, 19%, 16%, 9% and 5%, respectively, to the Company's operating income, which is expected to continue to grow at high rates in the future with the constant development of new energy vehicle manufacturers such as Tesla.

In 2024H1, the Company recorded an total income of RM6.1 billion, up 33% yoy, and a net profit of RMB 411 million attributable to the parent company, up 34.75% yoy, the result of sales volume increases of the OEM clients and the lift share of the Company among the OEM clients. The China Association of Automobile Manufacturers reported that Chinese vehicle manufacturers produced 13.25 million vehicles in H1, up 9.3% yoy, among which, Geely and Chery, the Company's core clients, saw a rapid yoy growth of the sales volume, being 41% and 48%, respectively, and Li, the Company's new-force client, saw a yoy growth of 36%.

Xinquan is a promising domestic automotive interior and exterior decoration enterprise. With the continuous expansion of the clients base and production capacity, it is expected to maintain sustained growth. We are optimistic about the long-term development of the Company and expect EPS to be 2.25/2.94/3.65 yuan respectively for 2024/2025/2026, a yoy increase of 36.6%/30.3%/24.5%. We offer a target price of 55.7 yuan, respectively 24.7/19/15.2x P/E for 2024/2025/2026, and an "Accumulate" rating.

TMT, Semiconductors (Megan Tao)

In this month, I published a research report on JD Group (9618.HK).

In the second quarter of 2024, the company's revenue increased by 1.2% year-on-year to 291.4 billion yuan (RMB, hereinafter), mainly driven by the growth in service revenue. In terms of categories, product revenue (1P) was 233.9 billion yuan, remaining stable year-on-year, while service revenue (3P) was 57.5 billion yuan, up by 6.3% year-on-year. Looking at the business segments, JD Retail's revenue increased by 1.5% year-on-year to 257.1 billion yuan, and JD Logistics` revenue grew by 7.7% year-on-year to 44.2 billion yuan. Overall, in the second quarter of 2024, Non-GAAP operating profit increased by 33.7% year-on-year to 11.6 billion yuan, with a Non-GAAP operating margin of 4.0%, primarily driven by the better-than-expected performance of JD Logistics` operating margin. Non-GAAP net profit attributable to ordinary shareholders of the listed company was 14.5 billion yuan, up by 69.0% year-on-year. Regarding shareholder returns, as of June 30, 2024, the company has repurchased $3.3 billion, representing approximately 7.1% of the ordinary shares outstanding at the end of 2023.

With continuously improving user experience, increasing user stickiness, and a gradually improving business environment, the company is expected to enhance its monetization capabilities in the medium to long term. The growth in sales volume has also led to an increase in revenue from advertising, express logistics, and other service-related businesses and commission income. This growth is expected to bring about efficiency improvements and lower raw material procurement costs, forming a virtuous cycle. Therefore, we anticipate that service revenue will return to healthy growth in 2024, with year-on-year growth rates of 10%/13%/15% for 2024-2026. Considering that the adjustment period for JD Retail is coming to an end and the fundamentals are gradually improving, this trend is likely to help restore investor sentiment. Additionally, the company may benefit from the implementation of the domestic "trade-in" policy. We estimate the standalone value of JD Retail in 2024 to be 317.2 billion yuan, based on a forecasted PE ratio of 13.0 for 2024, slightly premium to the average PE ratio of comparable companies at 9.2.

In 2024, JD will focus on improving user experience and increasing market share, continuing to enhance price competitiveness and platform ecosystem construction. JD Retail will continue to implement a low-price strategy, and there is still significant room for online penetration in sectors such as supermarkets, sports, furniture, home decoration, automobiles, and service industries. With overall consumer spending stabilizing and improving in 2024, growth in various categories is expected to return to healthy levels, with core electrified categories of the company likely to continue gaining market share and supermarkets returning to benign growth. Furthermore, considering the intensified competition in the e-commerce industry, the short-term contribution from the realization end of 3P is not significant, and the effects of ecosystem construction will be gradually released in the medium to long term. We project that the company's operating income for 2024-2026 will be 1,143.8 billion / 1,221.6 billion / 1,311.4 billion yuan, with net profit attributable to the parent company being 30.5 billion / 34.9 billion / 39.6 billion yuan, corresponding to diluted EPS of 9.6 / 11.0 / 12.4 yuan, and corresponding PEs of 13.0 / 11.2 / 10.0x. According to the SOTP valuation method, based on the latest market values or valuations of subsidiaries and investee companies and a 30% discount value, we give a target market value of 452.0 billion yuan for JD Group in 2024, corresponding to a target price of 144 yuan / 155 Hong Kong dollars, with a rating of "Neutral".

Click Here for PDF format...