Company profile

JD.com (09618.HK) is a company that started as an e-commerce platform and has evolved into a leading technology and service provider with a core focus on self-operated business models. It has expanded its operations into various sectors, including retail, technology, logistics, and healthcare. The group's subsidiaries include JD Health, JD Logistics, Dada Group, and others. In the current environment of moderate economic recovery, consumers continue to be highly sensitive to product prices, and the e-commerce industry is fiercely competitive. The company adopts a strategy of low prices and market penetration while also emphasizing quality and service to enhance the shopping experience and frequency of use for its core users.

Overall performance in 2Q24 exceeded market expectations with growing shareholder returns

In 2Q24, JD.com reported a year-on-year revenue growth of 1.2% to 291 billion yuan, mainly driven by the growth of service revenue. In terms of category, product revenue (1P) reached 234 billion yuan, while service revenue (3P) reached 58 billion yuan, with a 6.3% YoY increase. Breaking it down by business segment, JD Retail's revenue grew by 1.5% YoY to 257 billion yuan, and JD Logistics` revenue grew by 7.7% YoY to 44 billion yuan. Overall, the company's Non-GAAP operating profit increased by 33.7% YoY to 12 billion yuan, with an operating profit margin of 4.0%, primarily driven by the beyond-expectation performance of JD logistics. The Non-GAAP net profit attributable to ordinary shareholders of the listed company was 15 billion yuan, a 69.0% YoY increase. In terms of shareholder returns, as of June 30, 2024, the company has cumulatively repurchased US$3.3 billion, representing approximately 7.1% of the total outstanding common shares as of the end of 2023.

JD Retail: Platform ecosystem continues to show healthy improvement, and low prices and subsidies remain strategic focal points in the context of macroeconomic recovery

In the second quarter of 2024, JD.com achieved retail revenue of 257 billion yuan, representing a year-on-year growth of 1.5%, primarily driven by the growth in active users and order volume. Both purchase frequency and order volume achieved double-digit year-on-year growth this quarter, with third-party merchant order volume increasing by 20% year-on-year, reaching a new high in the past two years. Operating profit reached 10.1 billion yuan, with an operating profit margin of 3.9%, an increase of 0.7 percentage points year-on-year, mainly influenced by the reduction in free shipping thresholds and increased promotional marketing expenses. In terms of the breakdown by revenue category:

Product Revenue (1P): According to data from the National Bureau of Statistics, the total retail sales of consumer goods in the second quarter of 2024 amounted to 12105 billion yuan, a year-on-year decrease of 1.8%. In terms of online consumption, the online retail sales of physical goods reached 3176 billion yuan, a 10.2% increase, surpassing the overall growth rate of offline retail. Considering the government's new round of "trade-in" policies that will release pent-up demand and the expected continued recovery of the real estate market, we anticipate that revenue from JD.com's core categories such as 3C electronics will continue to grow, with year-on-year growth rates of 5%, 6%, and 6% in 2024, 2025, and 2026, respectively. At the same time, revenue from daily department stores will continue to benefit from platform improvements, and we predict a stable growth rate of 5%, 7%, and 7% year-on-year in 2024, 2025, and 2026, respectively.

Service Revenue (3P): The company has increased its efforts in building the 3P ecosystem and proactively optimizing the user experience, resulting in steady growth in monthly active users on the JD.com app. The company has implemented measures such as reducing commissions and service fees for 3P merchants, leading to a decrease in commission rates. As the 3P ecosystem is still in its early stages, the company is expected to continue investing in order to attract users from lower-tier cities through initiatives like enriching the supply of low-priced products and targeted subsidies. This may result in short-term or insignificant contributions to monetization.

However, as user experience continues to improve, user stickiness increases, and the business environment gradually improves, the monetization capabilities are expected to improve in the medium to long term. Furthermore, the growth in sales volume also brings about an increase in revenue from service-oriented businesses such as advertising placements and express logistics, as well as commission income. It also leads to efficiency improvements and lower raw material procurement costs, forming a virtuous cycle. Therefore, we anticipate that service revenue will return to healthy growth in 2024, with year-on-year growth rates of 10%, 13%, and 15% in 2024, 2025, and 2026, respectively.

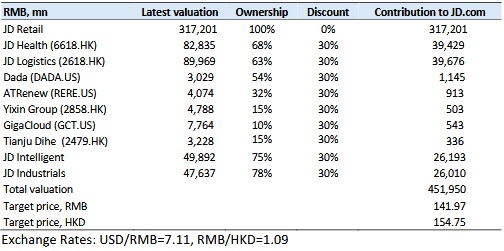

Considering that the adjustment period for JD Retail's business is coming to an end and the fundamental trends are gradually improving, there is hope that this will promote the restoration of investor sentiment. In addition, the company may benefit from the implementation of the domestic "trade-in" policy. We estimate the segment value of JD Retail in 2024 to be 317 billion yuan. Based on a forecasted PE ratio of 13.0 for 2024, there is a slight premium compared to the average PE ratio of comparable companies at 9.2x.

JD Logistics: Logistics industry shows stable recovery, and self-operated supply chain revenue remains stable

According to monitoring data from the State Post Bureau, as of June 30th, the express delivery volume in China has reached 800 million parcels this year, which is 59 days earlier than in 2023, indicating a steady recovery in the industry. In the second quarter of 2024, JD Logistics` revenue increased by 15.2% year-on-year to 44 billion yuan, and the operating profit increased by 328.0% year-on-year to 200 million yuan. With the improvement of the company's global supply chain network, the economies of scale are gradually manifesting. By providing one-stop services to support Chinese brands going global, the number of customers in the integrated external supply chain may steadily increase.

Company valuation

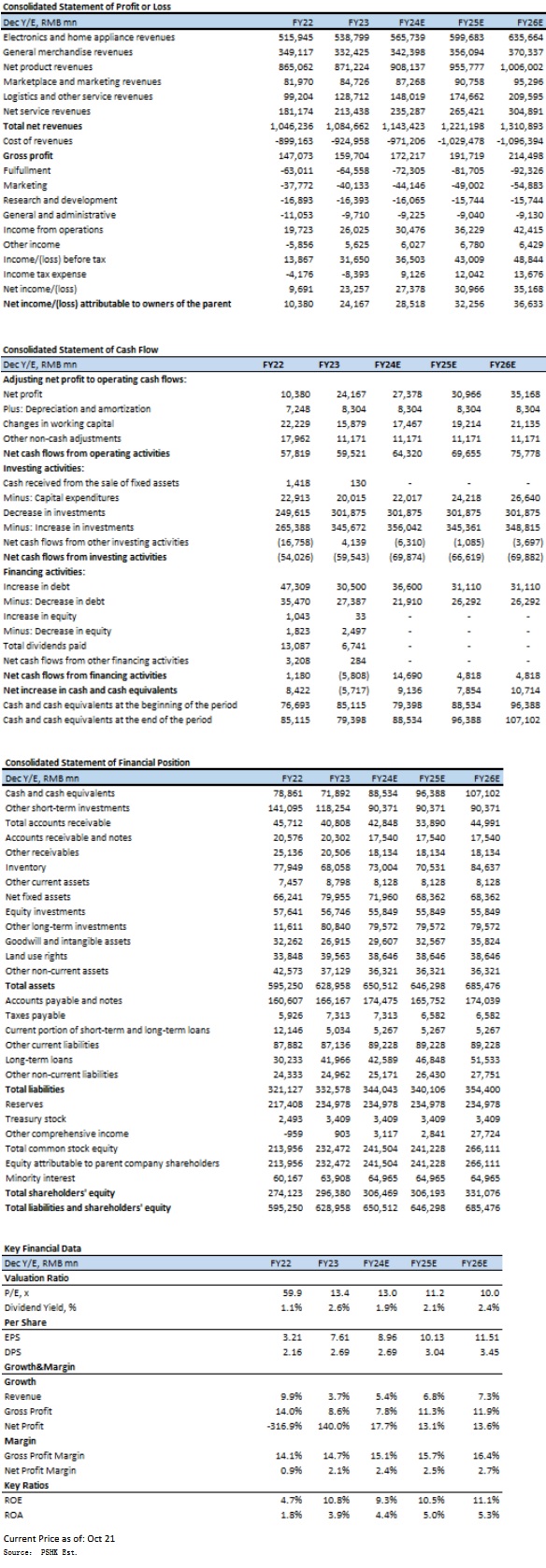

In 2024, JD.com will focus on improving user experience and increasing market share, continuing to promote price competitiveness and platform ecosystem construction. JD Retail will continue to implement a low-price strategy, and there is still significant room for online penetration in areas such as supermarkets, sports, furniture, home decor, automobiles, and services. With the overall consumption stabilizing and improving in 2024, the growth of various categories is expected to return to a healthy pace. The company's core categories, such as consumer electronics, are expected to continue gaining market share, and the supermarket category is expected to return to positive growth. Considering the intensified competition in the e-commerce industry and the relatively insignificant short-term contribution from the monetization end of the 3P ecosystem, with the effects of ecosystem construction being gradually released in the medium to long term, we project the company's operating revenue for 2024-2026 to be 1,144 billion yuan, 1,222 billion yuan, and 1,311 billion yuan, respectively, with net profit attributable to the parent company of 31 billion yuan, 35 billion yuan, and 40 billion yuan, corresponding to diluted EPS of 9.6 yuan, 11.0 yuan, and 12.4 yuan, and a corresponding PE ratio of 13.0x, 11.2x, and 10.0x. Based on the SOTP valuation method and on the latest market value or valuation of subsidiaries and investee companies with a 30% discount, we have set a target market value of 452 billion yuan for JD.com in 2024, corresponding to a target price of 144 yuan/155 HKD. We rate it as a "Hold" rating.

Risk factors

1) The monetization capabilities of the platform ecosystem may not meet expectations; 2) increased competition in the retail and logistics industries; 3) consumer demand may recover weaker than expected.

Financials

Click Here for PDF format...