Established in 2002, Tianli International (01773) is a comprehensive education service operator in Western region of the PRC, providing with comprehensive education management and diversified services. With a presence in Sichuan province where Tianli International is based in, its school spans across 36 cities in Inner Mongolia, Shandong, Henan, Guizhou, Jiangxi, Zhejiang, Yunnan, Gansu, Anhui, Guangxi, Guangdong, Shaanxi, Shanghai, Chongqing and Hubei. As of 29 February 2024, it principally provided students with comprehensive education services in 50 schools. For the same period, the number of full-time teachers employed by Tianli self-owned schools was 2,060 (as of 28 February 2023: 1,654). There were 36,708 high school students in the Company's school network as at the beginning of the 2023 fall semester, representing an increase of 43.8%, among which the enrollment number of new high school students was 19,071, representing an increase of 41% as compared with the enrollment number of new high school students as at the beginning of the 2022 fall semester.

Revenue from comprehensive education service growth has been robust

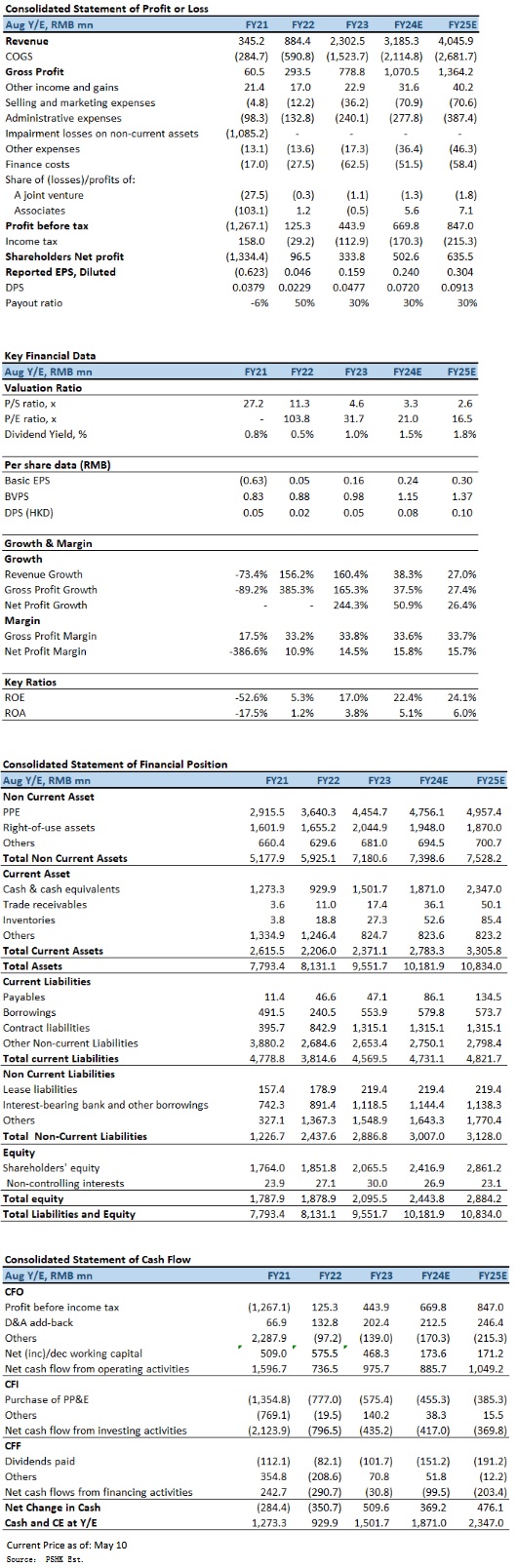

For the year ended 31 August 2023 (FY2023), revenue increased by 160.3% to RMB2302 million, primarily driven by increase of revenue from comprehensive educational services and sales of products. Adjusted profit for the year was RMB366 million, an increase of 276.4% YoY. During the period, basic EPS were RMB15.90 cents, the full-year dividend was RMB4.77 cents per share, and the dividend payout ratio was 30%.

The gross profit was RMB779 million, representing an increase of 165.3%, primarily due to the increase in the number of high school students enrolled and the revenue from the provision of comprehensive quality services and product sales. The gross profit margin was 33.8%, representing a slight increase of 0.6 percentage points.

The cost of sales consists of material consumption, staff costs, depreciation and amortization, procurement cost of products, teaching activity costs, utilities and others. The cost of sales increased by 157.9% to RMB1524 million, primarily due to the significant increase in revenue resulting in the corresponding increase in costs related to business operations.

Material consumption costs increased by 34.7% to RMB340.6 million, primarily due to the increase in the number of diners in the canteens operated. Staff costs increased by 232.2% to RMB397 million, primarily due to the increase in labor cost as a result of the recruitment of new teachers resulted from the increase in the number of high school students, and the provision of comprehensive quality services, product sales business, etc.. Depreciation and amortization costs increased by 56.8% to RMB184 million, primarily due to the increase in depreciation as a result of the high schools newly opened in September 2022 and the completion of the spin-off and consolidation of four additional high schools. Procurement cost of products increased by 911.9% to RMB459 million, primarily due to the increase in procurement costs as a result of a significant increase in product sales revenue of 837.8%. Teaching activity costs increased by 223.6% to RMB107 million, primarily due to the increase in teaching service costs related to the business of study tours which is in line with its significant growth. Utilities cost increased slightly by 6.0% to RMB16 million, due to the fact that on one hand, the increased number of students served would increase the costs, and on the other hand, the Group promotes the green office and frugality convention, and integrates environmental awareness and green actions into school daily management to improve operational efficiency.

The revenue from comprehensive educational services increased by 253.8% to RMB1223 million, which is primarily due to : 1) the increase in high school students enrollment; 2) the new separation of 4 for-profit high schools with independent operating licenses from the integrated schools, and hence the consolidation of the financial results of such high schools into the consolidated financial statements of the company; 3) the provision of comprehensive quality services by the company to tens of thousands of people of appropriate age, including but not limited to sinology, technology, sports, art, etc., which aimed at facilitating all-round development of students and cultivating comprehensive talents; and 4) the end of the pandemic, which led to an explosive growth in the study tour business. The sales revenue of RMB555 million, including revenue of RMB160 million from the sale of student supplies, such as school uniforms, bedding, daily necessities and stationery provided to students through the online campus store; and revenue of RMB395 million from the supply and sales of agricultural and sideline products through the integration of channel resources and logistics system. The revenue from canteen operations increased by 12.3% to RMB485 million, primarily due to the increase in the number of students served by the company. The revenue from management and franchise fees decreased by 17.7% to RMB39 million, primarily because the company adjusted its cooperation model with suppliers, resulting in a decrease in revenue from supply chain management services.

Maintained strong interim growth

For the six months ended 29 February 2024 (1HFY2024), revenue increased by 73.8% to RMB1645 million. Among which, revenue from comprehensive educational services increased by 64.4% to RMB851 million, which is primarily due to the increase in high school students enrollment; the end of the pandemic, which led to a significant growth in the study tour business. Sales revenue increased by 1.8 times to RMB474. The revenue from canteen operations increased by 19.9% to RMB294 million, primarily due to the increase in the number of students served by the company. The revenue from management and franchise fees increased by 34.9% to RMB26.056 million, primarily because of the addition of three schools to the company's entrusted school network. The gross profit margin 35.4%, representing a slight decrease of 3.8 percentage points. Adjusted profit was RMB319 million, a year-on-year increase of 70.0%.

Company valuation

The government has released the "Opinions on Further Reducing the Homework Burden and Off-campus Training Burden of Students in Compulsory Education" (¡mÃö©ó¶i¤@¨B´î»´¸q°È±Ð¨|¶¥¬q¾Ç¥Í§@·~t¾á©M®Õ¥~°ö°Vt¾áªº·N¨£¡n), with the aim of effectively reducing the heavy workload and off-campus training burden of students in the compulsory education stage. This policy is commonly referred to as the "double reduction" (¡uÂù´î¡v). However, as a result, the education and training industry suddenly entered a period of decline, leading to a significant number of job losses. Nevertheless, in February 2024, the Ministry of Education announced the "Regulations on the Management of Off-campus Training" (draft for public opinion) (¡m®Õ¥~°ö°VºÞ²z±ø¨Ò¡n¡]¼x¨D·N¨£½Z¡^), which specifically mentioned guidelines for non-educational off-campus training institutions to participate in after-school services and address the reasonable needs for after-school training. The Regulations also propose encouraging and supporting institutions such as youth centers and science museums to offer off-campus training, enriching curriculum offerings, and expanding enrollment numbers. Local governments are explicitly permitted to introduce non-subject-based off-campus training institutions to participate in after-school services through various means, adopting multiple measures to meet students` reasonable and diverse educational needs. As the policy further defines and clarifies the boundaries of off-campus training, and with the industry's regulatory policies becoming more transparent, with a focus of for-profit high schools, providing students with comprehensive operational services, including but not limited to a series of other value-added services such as online campus store, logistical integrated services, study guidance for arts and sports oriented schools, international education, overseas studies consulting and study tours, Tianli is expected to benefit from sustainable development. Taking all these factors into consideration, we anticipate the company's basic earnings per share (EPS) for the FY2024E & FY2025E to be RMB$0.24 and RMB$0.30, with a target price of HKD6.01, corresponding to a FY2024E P/E of 23.3 times (similar to the industry's average). Our investment rating is ¡§Accumulate".

Risk factors

1) Policy changes impacting the industry's operating environment; 2) Intensified industry competition; and 3) Lower-than-expected student enrollment.

Financial

Click Here for PDF format...