Investment Summary

Earnings Decreased by 20% by Year in H1

In 2019H1, the revenue of CSA was RMB72.94 billion, an increase of 7.97% yoy, the net profit attributable to the parent company was RMB1.69 billion, a decrease of 20.92% yoy, and the net profit excluding non-recurring items was RMB1.43 billion, a decrease of 22% yoy.

In 2019 Q1 and Q2 the revenue of the Company reached RMB37.63 billion and 35.31 billion, respectively, an increase of 10.4% and 5.54% yoy, while the net profit attributable to the parent company was +RMB2.65 billion in Q1, an increase of 4.1%, and -RMB960 million in Q2, an increase of RMB550 million in loss.

Yield of Domestic Routes under Pressure in Q2

The trade friction between China and the United States have intensified, and the domestic macroeconomic downturn resulted in a sluggish growth in aviation demand. The fare level during the off-season (especially of domestic routes) was under pressure. Though the overall P L /F increased by 0.2 ppts yoy to 82.65%, the unit revenue per passenger kilometre dropped by 1.65% yoy to RMB0.478. The P L /F of domestic routes dropped by 0.12 ppts, and the yield level dropped by 1.52% yoy to RMB0.518. The P L /F of international routes increased by 0.84 ppts, and the yield level of the same dropped by 0.79%, while the P L /F of regional routes increased by 1.96 ppts, and the yield level of the same dropped by 1.21%.

Slightly Lower Revenue Growth than Expected, and Sound Control of Cost

In H1, the total revenue of the Company increased by 7.97% yoy to RMB72.94 billion, while the growth rate decreased by 4 ppts when compared to that of the corresponding period. In addition to the pressured demand, the suspension of Boeing 737MAX and the total quantity control of the Civil Aviation Administration also brought a drag on the Company's capacity release. The available seat kilometre increased by 10.14% yoy, which was below expectations and a decrease of 2 ppts, approx., when compared to that of the corresponding period. As a result, the passenger turnover growth decreased by 1.9 ppts yoy to 10.3%.

During the period, the Company continued to strengthen its control on major costs and optimize its flight operation mechanism, and the cost was saved effectively. The operating cost increased by 7.2% yoy, less than the increase in total revenue. The unit available ton kilometre cost decreased by 1.62% yoy to RMB2.846.

Financial Expense Increased Significantly Due to Changes in Accounting Standards

The financial expense reached RMB3,243 million, an increase of RMB1,207 million or 59% yoy, of which, the net exchange loss reached RMB312 million, a decrease of 25.7% when compared to that of the same period of last year. The interest expense excluding those capitalized was RMB2,876 million, a significant increase of RMB1.34 billion or 87% yoy, mainly due to the implementation of new lease rules and the rise of interest expense on lease liabilities. Meanwhile, due to the new lease rules, the total assets of CSA increased by 21.7% to RMB300,171 million from that at the beginning of the period, the total liabilities increased by 33.18% to RMB224,378 million from that at the beginning of the period, the ratio of USD liabilities increased by 16 ppts from that at the end of 2018, and the sensitivity of net profit to USD exchange rate increased from RMB195 million to RMB517 million.

Investment Thesis

In Q3, as the industry prosperity is basically flat with that of the previous year, it is expected that the redeployment of capacity will boost the operating efficiency of the domestic routes of the Company to a certain extent, while that of international routes will remain the same. In H2, the halving of the levy on the civil aviation fund will help reduce the cost, though the RMB exchange rate and oil price trend in the short term will be the most significant risk factors for performance.

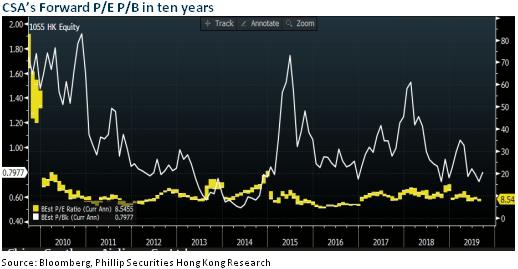

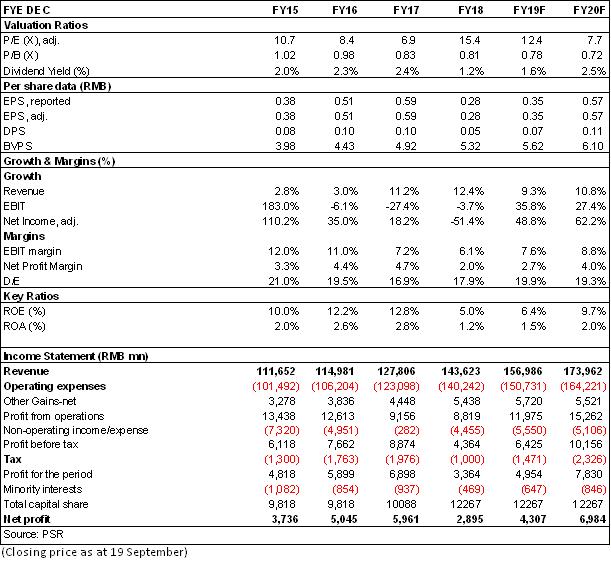

In accordance with the latest data, we adjust the estimate of the Company's EPS to RMB0.35/0.57 in 2019/2020. The target price is HK$ 6, equivalent to 15.4/9.5x and 0.96/0.88x estimated P/E ratio and P/B ratio, respectively, in 2019/2020. The "Buy" rating is maintaining. (Closing price as at 19 September)

Risk

Traffic demand languished for the deterioration of macro-economy;

The depreciation of the RMB against USD would bring exchange loss;

Oil prices rose exceeded forecast.

War, terrorist attacks, SARS and other emergencies;

Irrational inter-industrial price war;

Financials

Click Here for PDF format...