Company Profile

MINTH Group Limited is China's leading supplier in design, manufacturing and sales of trim strips, decorative parts, body structural parts and other automotive components and parts. The revenue from its three major products accounts for 34%, 32% and 21.5% of total revenue, and core products take up more than 30% market share.

Its strong capability of R&D, cost control and quality control have greatly propped up and sustained business development. MINTH's R&D centers are located in China, Germany, North America and Japan, with thousands of R&D personnel. In recent years, R&D expenses have maintained an over 4% proportion of total expenditure. The company has the capability of synchronous design and development with OEMs, and has been an industry leader.

More than 30 manufacturing plants attached to OEMs have been built across China's Jiaxing, Ningbo, Guangzhou, Wuhan, Tianjin, Changchun and other cities, and manufacturing bases also scatter across foreign countries, including the United States, Mexico, Thailand and Germany, ensuring flexibility of manufacturing and lowering transport costs. On the other hand, the company's entry into automobile interior and exterior parts as early as 1993 has secured benefit from China's automobile industry boom. Its net profit margin and revenue CAGR between 2006 and 2015 stood up to 19% and 26%, respectively.

Customer and Regional Structure More Balanced, Gross Margin Gradually Stabilizes

The company's large customer base covers almost all joint-venture OEMs in China, among which the Japanese-car customers make up the largest proportion of 39%. In recent years, with active exploitation of customers of other car series, the proportion of European cars, American cars and self-owned cars has gradually increased to 17.3%, 32.5% and 7.5%, respectively.

The company owns a global production, R&D and sales network and a rapidly growing overseas business with the globalization of auto parts and components procurement. Currently, the revenue from overseas market accounts for more than 40% of total revenue, of which North America 25.6%, Europe 8.7% and the Asia-Pacific region 6.4%. The company aims for becoming a giant in global auto parts and components with the intended revenue from overseas business comprising 50% of total revenue to RMB10 billion by 2020.

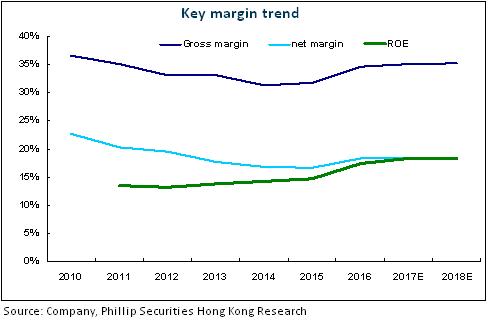

Though gross margin fell from 40% to 31% year by year due to appreciation of RMB, OEM price drop and labor-cost increase, the profitability has proved to be robust with gross margin higher than the industry high level of 30% and a net profit margin of 17%. Beginning from H2 2015, gross margin has resumed to 34% thanks to sales-structure optimization and capacity-utilization improvement after the Wuhan plant's reaching target output. We expect the pick-up trend to maintain as projects geared to BMW, Audi and other high-end customers proceed.

Strategic Layout of Four New Businesses Expected to Boost New Growth

MINTH's aims its enterprise strategy at becoming a giant in the global auto parts and components, and has actively developed the strategic products which sustain long-term growth, including four major businesses in body lightening (aluminum products), automotive intelligent electronics (vehicle cameras), motor and new energy automobile. In terms of light-weight products, the company has already been a core global supplier of BMW's aluminum strips and entered Audi's and Daimler's global procurement system, with anticipated CAGR exceeding 50%.

In terms of intelligent drive, it entered vehicle-camera sector in 2015 by acquisition of SPTek, an automotive electronics company in Taiwan for a 51% stake, formed a 60/40 JV with Japanese Fujitsu in 2016, and ran its Chunxiao camera plant in 2016, which is likely to be a new profit growth point if certification goes well.

Regarding high-performance electric drive system and new energy automobile, it formed a JV with the American Clean Wave in 2016 to produce advanced electric drive systems for new energy cars. Also, the subsidiary MINAN has recently obtained the qualification for making electric passenger vehicles. The company's layout in key sectors of new energy cars will lay a foundation for sustained growth in future results.

Investment Thesis

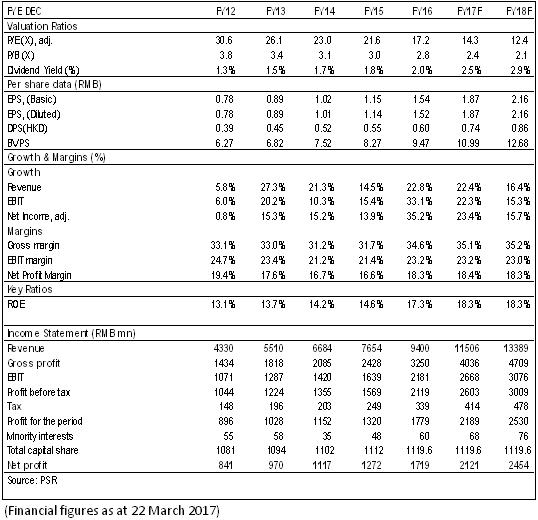

In summary, the existing businesses indicate a robust growth momentum, while great potential boom lies before the new ones. We believe that it is reasonable to give the company a valuation of 16.6x/14.3x P/E in 2017/2018, equivalent to target price of HK$ 34.45 and Accumulate rating. (Closing price as at 22 Mar 2017)

Financials

Click Here for PDF format...