Company Profile

As a large automobile manufacturer in China, GAC has JVs with Toyota, Honda, Mitsubishi and Fiat; the former two constitute 80% of its sales volumes and the majority of profit. It has an independent brand ¡§Trumpchi¡¨. GAC Won nod for privatization of Denway (203@HK) in HKEx on Aug, 2010, and was listed in Shanghai Stock Exchange in March 2012.

Summary

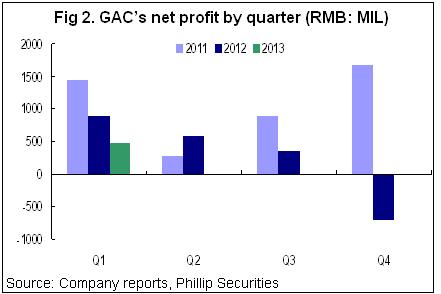

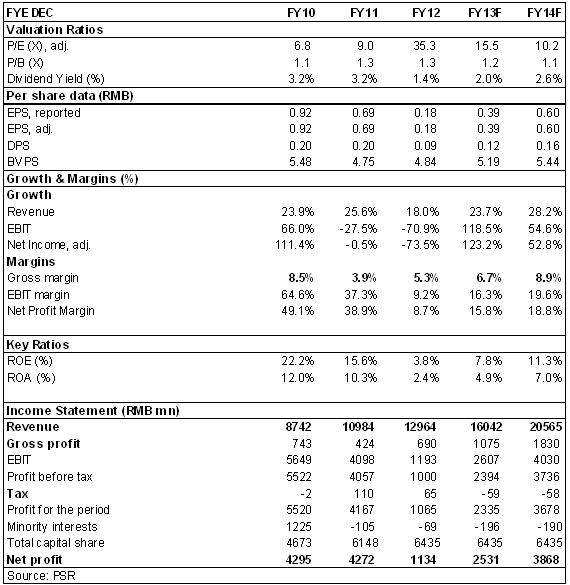

-Influenced by China-Japan Diaoyu Islands Event and the fact that the new joint ventures are still at the beginning, the net profits of GAC in the whole year of 2012 and the first quarter of 2013 respectively reduced by 73.5% and 47% to RMB 1.134 billion and 478 million yoy, in which the investment incomes respectively reduced by 43% and 17% respectively yoy. The final earrings per share were RMB 0.18 and RMB 0.07 respectively, while those of the same period in the last year were respectively RMB 0.69 and RMB 0.15. The board of directors proposed a final dividend of RMB 0.02/share, together with the medium-term dividend of RMB 0.07, also the dividend rate of the whole year of about 51%.

-Heavily affected by the anti-Japanese events and due to the ageing of main car models ¡§Highlander¡¨ and ¡§Accord¡¨, the sales volume of two JVs, GAC-Toyota and GAC-Honda respectively reduced by 8.9% and 12.7% yoy to 250,000 and 316,000 in 2012 and the productivity utilization was declined to 65%, in which the sale volume of the two both reduced by above 40% in 2012Q4 and the investment incomes contributed changed from positive to negative. The first car models of the new JVs GAC-Fiat and GAC-Mitsubishi was respectively launched in September and November, which was limited by the beginning and had not brought obvious benefit. Driven by SUV model, the independent brand ¡§Trumpchi¡¨ has a substantial increase of sales volume by 92% to 32,600 in 2012.

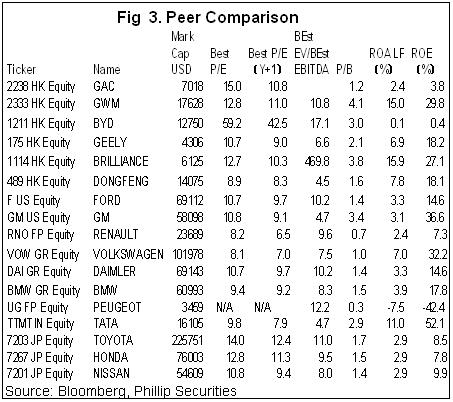

-During 2013M4, sales volume of GAC increased by 19% to 227,000, in which the sales volume of GAC-Toyota started to significant rise, with accumulative yoy growth from flat to 8.4%, while the sales volume of GAC-Honda was relatively plain, with accumulated sales volume increasing by 1.1% yoy. The overall market share of Japanese cars in China reduced to 8.96% in October 2012. With the gradual mitigation of anti-Japanese events, the sales of Japanese cars have been recovered month by month. In April 2013, the overall market share of Japanese cars rebounded to about 18%, further shortening the gap with the previous level. Profit from GAC-Honda and GAC-Toyota has accounted for over 90% of total profit of GAC Group and the improving of productivity utilization will bring a restorative growth to the Group's profit.

-As for new models, GAC-Honda plans to launch the 9th generation of Accord, the facelift EverusS1 and crossover vehicle - Crider specially aimed at the Chinese market in 2013, the latter positioned between Accord and Civic will fill in the blank of corresponding product chain. As most of the new models will be launched in the second half of the year, it is expected that the sales volume of GAC-Honda in the second half of the year will rebound significantly. There are fewer new models of GAC-Toyota in 2013, only including the facelift Verso and new model of Camry as well as the new generation of Yaris. It is expected that with the new production capacity of 240,000 is put into production, GAC-Toyota will accelerate the release of new models in 2014 and 2015. The independent brand of passenger vehicles of GAC started relatively lately, so the influence on profit in a short term is still limited

-As for new JVs, the two-compartment version of Viaggio from FIAT and Pajero Sport from Mitsubishi are hopefully to come into season in the latter half of the year, but it is difficult to contribute profits in 2013 due to the start-up cost and channel construction limitation. However, FIAT-Chrysler Alliance owns relatively sufficient product lines. It is hopeful for Jeep Cherokee to put into production in the latter half year of 2014 and to introduce at least 2 sets of new SUVs in 2015. By virtue of gradual introduction of booming SUV, GAC FIAT is expected to be the new profit increase point of the company in following three years.

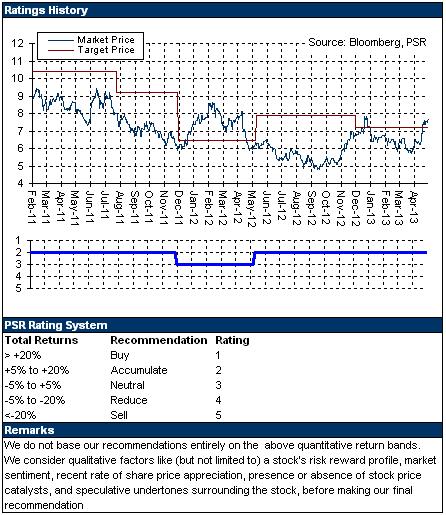

-Because there still is a lot of capital expenditure in this year and the next year, we predict that 2013 will still be the ¡§ready-year¡¨ of GAC. There will be an expecting substantial growth of achievements in 2014. We adjust predicting EPS in 2013 and 2014 to RMB 0.39 and RMB 0.60, converting into HKD 0.49 and 0.76. Our 12-month target price of the GAC is HKD 8.6, equivalent to 17.4x and 11.3 P/E in 2013 and 2014, and 11% higher than current price, remains an ¡§Accumulate¡¨ rating.

Click Here for PDF format...