Company Profile

Founded in 2004 and listed on the Stock Exchange of Hong Kong (Stock Code: 272) in October 2006, Shui On Land Limited is a flagship property management company in Chinese mainland established by Shui On Group. Shui On Land is engaged in residence development, commercial property investment & operation and hotel management business in core cities of Chinese mainland. And currently, it has 8 projects in different development stages in prime locations of Shanghai, Wuhan, Chongqing, Foshan and Dalian with a land reserve up to 13.2 million square meters. ¡§Xintaindi¡¨ is a famous commercial real estate band under the company and also its core business.

Investment Overview

The total income of Shui On Land decreased by 43% on a year-on-year basis to RMB 4.8 billion in 2012, and the core net profit sharply reduced by 87% to RMB 201 million. The main reasons for the significant decline of business include less delivery area, entry area declined by 30% and the annual sales volume of RMB 5.7 billion, which was far less than the sales target of RMB 12 billion. For the weak sales in good market conditions of 2012, my opinion is that there is lack of flexibility in sales strategies, the sales structure has changed and the recovery degree of high-end property is limited.

The company's rent and relevant incomes in 2012 increased by 47% on a year-on-year basis to RMB 1.25 billion, among which the rent and relevant incomes of investment property were up to RMB 1.06 billion, increasing by 26% on a year-on-year basis, and the rest RMB 190 million was from the hotel business. Shanghai Taipingqiao office and retailing property including Shanghai Xintiandi, Corporate Avenue Phase I and Shui On Plaza is the most excellent investment property of Shui On Land, although it only accounts for 38% in the total renting area, it contributes 66% of the rent income.

We can see the sign of Shui On Land in improvement of sales, it has increased the sales promotion scale, improved sales speed and accelerated the backflow of sales fund. We think, according to the current sales promotion speed, the residential sales volume of Shui On Land is very likely to break through RMB 12 billion, creating a new high, while the overall commercial sales income target of RMB 12 billion is expected to be reached.

In order to release more current funds and realize the investors` returns, Shui On Land established China Xintiandi Co., Ltd. to be dedicated to the development and operation of investment property. And it is planned to realize spin-off listing in the future. We think the spin-off of Xintiandi will be a win-win solution. On one hand, the company can use the fund financed to accelerate the development of sales property and improve asset turnover; on the other hand, China Xintiandi can attract investors paying attention to stable dividend yield to improve the estimation.

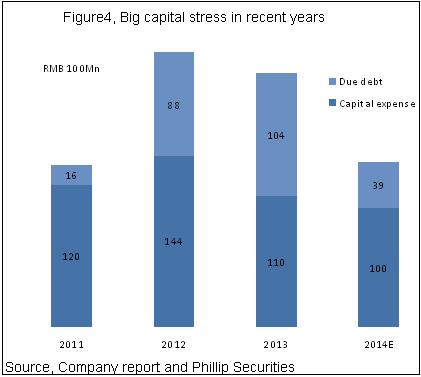

What drives Shui On Land to accelerate its sales is the realistic debt payment pressure. In 2013, Shui On Land needs to repay due debt of RMB 10.4 billion, including bank loan of RMB 5.1 billion, convertible loan of RMB 2.3 billion and bill of RMB 3 billion. In 2015, the company will need to repay a huge debt of RMB 19.2 billion, including three groups of bills. Overall, the company is confronted with a huge debt payment risk.

We think accelerating asset turnover, quick sales, low-cost financing and Xintiandi spin-off in planning area are all effective methods to improve the asset conditions of Shui On Land. The company is urgent to accelerate the development of the existing residential projects, accelerate sales and take all necessary methods to improve the sales income. After all, a sound and energetic sales cash flow is the key point for the company to thoroughly get rid of the debt crisis.

After the poor annual performance and allotment of stock, the stock price of Shui On Land has declined to HKD 2.4, and recently, the stock price has been stable and gradually rebounded. We think, in the future, Shui On Land will still face a large operation risk and heavy debt payment pressure, but the current stock price basically reflects the unfavorable factors of the fundamentals. Currently, the stock price of the company has been bottomed by stage, and there is expected to be a new round of rebound. The driving factors include the sales income and entry sales of Shui On Land are expected to be improved significantly in 2013 and the spin-off of China Xintiandi is expected to be listed in the market.

Based on our estimation of NAV of HKD 7.06 and 55% of the allowance to Shui On Land, we give 12m TP of HKD 3.40, which is equivalent to 5 times of EPS in 2014. We give the rating of ¡§Accumulate¡¨ to Shui On Land.

Click Here for PDF format...