|

JOINN(6127)

Analysis¡G

JOINN LABORATORIES (6127) is principally engaged in providing non-clinical drug safety assessment services to pharmaceutical and biotechnology companies. Its business comprises three segments : non-clinical studies services, clinical trial and related services, sales of research model. With the development of the novel coronavirus infection, the Company responded quickly and established a non-clinical evaluation system for COVID-19 vaccines, targeting different types of vaccines (including inactivated vaccines, recombinant vaccines, viral vector vaccines, mRNA vaccines, DNA vaccines, peptide vaccines) and antibodies, formulated a scientific and detailed evaluation programme, organized a professional evaluation team, and maximized the mobilization of company resources and prioritized the the evaluation of COVID-19 projects (including vaccines, antibodies, therapeutic drugs, etc.). (I do not hold the above stock)

Strategy¡G

Buy-in Price: $150, Target Price: $175, Cut Loss Price: $140

|

CHINA LIT(772)

Analysis¡G

China Literature Limited (772) is principally engaged in the provision of reading services, copyright commercialization, writer cultivation and brokerage, operation of text work reading and related open platform, which are all based on text work, and the realization of these activities through technology methods and digital media in China. The company has recently announced a brand new strategy during its annual conference. The company will take online literature as the cornerstone, and continuously improve its writer ecology, IP operation, and visual development. We are optimistic about the company`s IP development and operation system and believe that the IPs of the company will continuously generate value for the company.

Strategy¡G

Buy-in Price: $88.00, Target Price: $96.00, Cut Loss Price: $83.00

|

|

Weimob Inc. (2013.HK) - 1Q21 result beat market expectation, raised up USD 600 million to accelerate the investment ecosystem construction

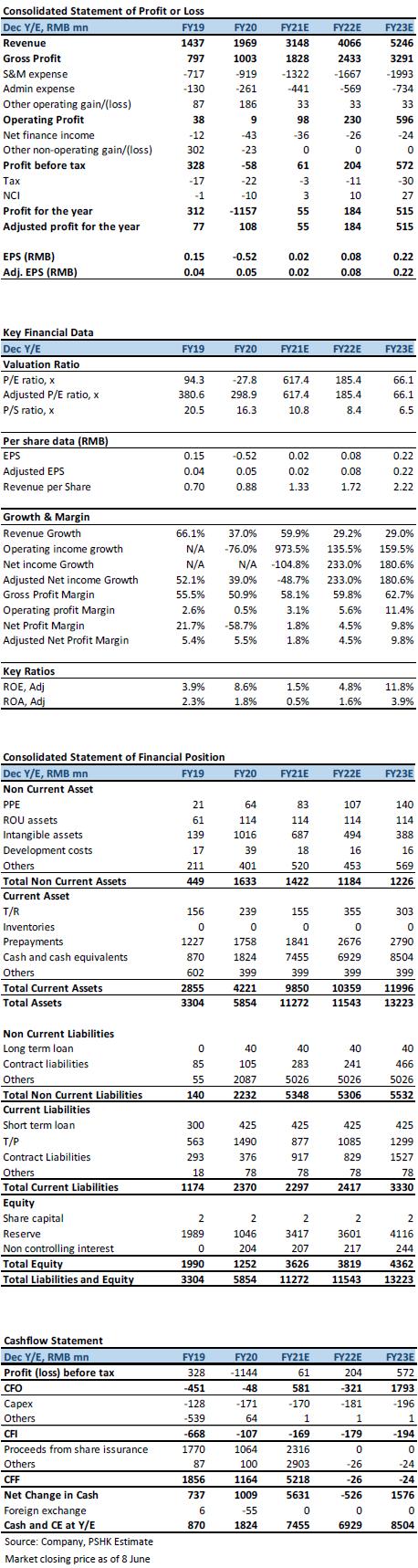

Investment Summary1Q21 result beat market expectation According to the company's announcement, the company's revenue from Subscription Solutions in 1Q21 represented an increase of over 100% as compared to 1Q20, which beat the market expectation. Further, as at the end of 1Q21, the number of paying merchants increased by approximately 21.9% as compared to 1Q20. The attrition rate was approximately 4.3%, with corresponding annualized attrition rate at 17.2%, which represented a huge improvement as compared to the 26.1% in 2020. On the other hand, the revenue from Merchant Solutions in 1Q21 was up by over 50% YoY. Raised up USD 600 million to accelerate the investment ecosystem construction According to the announcement on 25th of May, the company placed 156 million new shares with placing price at HKD 15.00, which represents a discount of approximately 6.6% to the closing price of 24th of May. The placing has been completed on 1st of June. At the same time, the company has proposed to issue USD 300 million of zero coupon guaranteed convertible bonds due 2026, with initial conversion price of HKD 21.00, which represents a premium of approximately 30.8% over the closing price of 24th of May. The placing and bond issuance will raise USD 600 million for the company and the proceeds will be used for improving the company's comprehensive research and development capabilities, upgrading the company's marketing system, supplementing working capital and general corporate purposes. The new share placing and the bond issuance recorded 8 times and 5 times subscription, respectively and many well-known and long term institution investors have shown interest, which fully demonstrated their recognition of the company's long term value. We believe the company will have sufficient capital for product R&D as well as M&A in various vertical industries, in order to further consolidate its competitive advantages in the market. ValuationWe continue to be optimistic about the company's 1) the KA customer expansion in various vertical industries 2) three core strategies, 3) TSO (Traffic + SaaS + Operation) operation model. We believe that the TSO model is expected to further increase the ARPU of the KA customers, thereby uplifting the ceiling of the company's future growth. We maintain our previous forecast on 2021-2023 Subscription Solutions revenue and adjust our forecast on 2021-2023 targeted marketing gross billing to HKD 15.8/20.8/26.9 billion (previous forecast was HKD 15.2/19.9/25.7 million). But since we expect the company to invest in PaaS and TSO continuously in the foreseeable future, we cut our 2021-2023 adjusted Net profit forecast to HKD 55/184/515 million (previous forecast was HKD 184/347/766 million). We maintain our 2022 targeted marketing target PE of 18x and 2022 subscription solution target PS of 23x, adjust TP slightly downward to HKD 26.46 (-0.9%), to reflect our more optimistic view on the company's targeted marketing business and to reflect the dilution effect as a result of the newly issued shares. The TP corresponds to adjusted PE of 966x/290x/103x in 2021/2022/2023, respectively. We maintain Buy rating. (Market closing price as of 8 June) (exchange rate: RMB 0.85/HKD) Risk1) The expansion of SaaS customers is worse than expected 2) The increased industry competition 3) Advertising demand is less than expected 4) Targeted marketing business mainly relies on the cooperation with Tencent 5) Valuation of the SaaS sector drops Financial Statements

Click Here for PDF format...

| Recommendation on 10-6-2021 | | Recommendation | Buy | | Price on Recommendation Date | $ 16.920 | | Suggested purchase price | N/A | | Target Price | $ 26.460 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2021 Phillip Securities (HK) Ltd. All Rights Reserved.

|