Investment Summary

The company's 1Q21 result missed market expectation

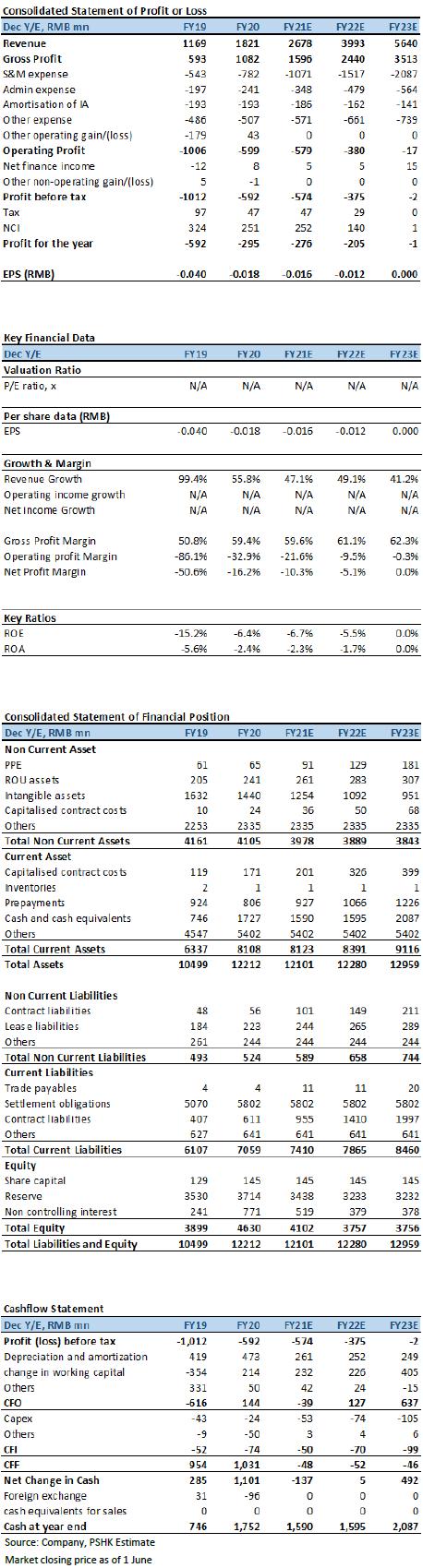

The company announced its 1Q21 result on May 10, and the result missed market expectations. The 21Q1 GMV was RMB 23.6 billion (+13.5% YoY), which was lower than market expectations. The GMV growth in the past few quarters have maintained at a high level (the average YoY growth rate of GMV in the past four quarters is roughly 75.9% YoY). Therefore, compared with the past data, the deceleration of the 21Q1 GMV growth was relatively obvious. The slowdown in GMV growth was mainly due to the drop in GMV from Kuaishou. The GMV from Kuaishou fell by 43.4% YoY to RMB 4.7 billion. We expect the GMV growth will resume rapid growth in 21H2. The company's management maintains their previous target YoY GMV growth rate of 50% in 2021 and expects that the GMV contribution from Kuaishou will drop to 10% by the end of 2021 (Kuaishou GMV accounted for 40% of total GMV in 2020).

In terms of revenue, the company's 21Q1 revenue was RMB 417 million (+11.9% YoY), which was also below market's expectation. In terms of breakdown, the subscription solution revenue was RMB 257 million (+20.7% YoY) and the merchant solution revenue was RMB 157 million (-0.2% YoY). Excluding the transaction fee revenue, the revenue from merchant solutions increased by over 20% YoY. The revenue from other business was RMB 3.55 million (+12.4% YoY).

In terms of GP, the 21Q1 GP was RMB 245 million (+15.7% YoY), with GPM at 58.7% (1.9ppts YoY). The GP from subscription solution was RMB 190 million (+21.1% YoY), with respective GPM at 73.8% (+0.2ppts YoY). The GP from merchant solution was RMB 55 million (+0.9% YoY), with respective GPM at 35.1% (+0.4ppts YoY).

In terms of the expenses, the company's S&M expense in 21Q1 was RMB 209 million (+29.9% YoY), with respective expense ratio at 50.3% (+7.0ppts YoY). The increase in both S&M expense and expense ratio was mainly due to the fact that the company has expanded its direct sales team and established operation service centers in both Wuhan and Nanjing in 21Q1. The newly hired sales team tend to have lower revenue conversion efficiency. The admin expense in 21Q1 was RMB 71 million (+56.4% YoY), with respective expense ratio at 16.9% (+4.8ppts YoY). The rise in both admin expense and expense ratio was because the 21Q1 admin expense has included one-off expenses such as the related expenses of the take private and main board listing proposal. The 21Q1 other operating expense was RMB 137 million (+34.7% YoY), with respective expense ratio at 32.7% (+5.5ppts YoY). The increase in both the expense and expense ratio was due the fact that the company has increased investment in R&D for Youzan PaaS platform and other new products.

In terms of profit, the company's 21Q1 net loss attributable to the parent was approximately RMB 91 million. The net loss was further increased by 21.7% YoY. The NPM was -21.8% (-1.8 ppts YoY).

The structure mix of new paying merchants optimized

The number of new paying merchants in 21Q1 was 7,961 (-43.1% YoY). The main reason for the YoY decline in the number of new paying merchants was that there were many small merchants set up online stores through company's SaaS products in 20Q1, due to the pandemic and hence the corresponding base in 21Q1 was high. Further, Q1 is typically the sales offseason. Although the number of new merchants in 21Q1 dropped sharply YoY, the structure mix of new merchants has been significantly optimized. Among the new paying merchants, the proportion of merchants subscribing to the high end products was close to 50%. The optimization of the merchant structure mix will affect positively to the future key operating indicators such as renewal rate, ACV, ARPU, LTV etc. The number of paying merchants as of the end of 1Q21 was 95,692, which reflects a decrease of 1.5% comparing to the 97,158 at the end of 20Q4. The decrease in the number of the paying merchants was mainly due to the loss in Kuaishou and other small merchants during the period. On the other hand, the company's 21Q1 ACV reached RMB 13,060 (+9.9% QoQ).

The company's offline commerce SaaS business has been developing well. The number of paying merchants from Youzan Retail, Youzan Chain, Youzan Beauty and Youzan Education have all increased QoQ. The number of paying merchants from Youzan Chain, Youzan Beauty and Youzan Education increased by over 100% YoY respectively.

The launch of new products enriches the company's product matrix

The company has recently launched a few new products, including Youzan WeCom Assistant and WowShop.

1) Youzan WeCom Assistant is an individually selling product, that empowers merchants in customer acquisition, activation and operation. Merchants can accumulate customer assets in WeCom and drive the activity and conversion rate of its customers. Youzan WeCom Assistant is usable with Youzan WeiMall, Youzan Retail, Youzan Chain, Youzan Beauty and Youzan Education. WeCom Assistant is currently the only office tool that is linked with Wechat, and can solve many of the shortcomings of operating a business through personal WeChat accounts. At present, the product is divided into basic version (charging RMB 3,800/year) and professional version (charging RMB 6,800 year).

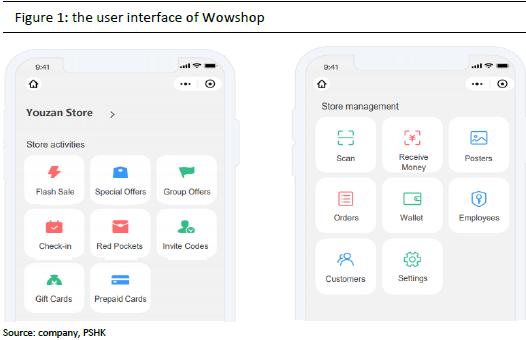

2) Wowshop is an all-in-one marketing and store management toolkit focusing on physical stores in lower-tier cities. It mainly provides store activities function (including flash sales and special offers to attract customers to physical stores offline) and store management services (including order and employee's management). The user interface of Wowshop is relatively simple, which greatly reduces the threshold for merchants in low-tier cities to use digital marketing tools. Since the product is positioned to serve merchants in the lower-tier cities, hence the subscription fee is relatively low, with an annual subscription fee of RMB 1,888/year.

Valuation and Investment Thesis

The company's 1Q21 result missed expectation, but we expect it to gradually picking up strong growth momentum in 2Q21 and 2H21. Considered that the number of the paying merchants in 21Q1 was lower than we expected, we trim the company's 2021/2022/2023 revenue forecast to RMB 2.68/3.99/5.64 billion from RMB 2.81/4.15/5.86 billion. We lower the SaaS and extended services target P/S to 25x and the transaction and other business P/S to 5x, in order to reflect the current market's more cautious view on high valuation companies. We cut our TP to HKD 3.04 (-23%). We maintain BUY rating. (Market closing price as of 1st June) (exchange rate: RMB 0.85/HKD)

Risk

1) The delay in Youzan Technology listing and take private of China Youzan 2) The expansion of SaaS customers is worse than expected 3) The increased industry competition 4) GMV increase less than expected 5) Merchants renewal rate less than expected

Financial Statements

Click Here for PDF format...