Sectors:

Air & Automobiles (Zhang Jing),

TMT & Education (Kevin Chiu)

Consumer & Property Management (Timothy Chong)

Automobile & Air (ZhangJing)

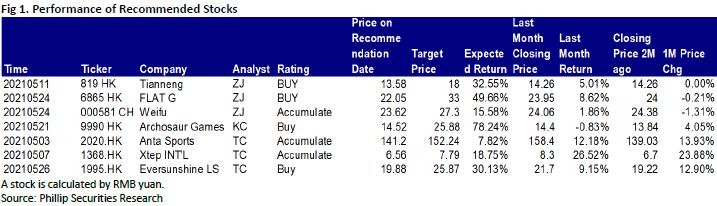

This month I released 3 updated reports of Tianneng Power (819.HK), FLAT Glass (6865.HK) and Weifu (000581.CH) which got success by their unique Competitive edge. Among them, we highly recommend FLAT Glass .

Benefiting from the continuation of the industry's high boom and the launch of new production lines, Flat Glass recorded operating revenue of RMB2,057 million in the first quarter of 2021, up by 70.95%yoy. The net profit attributable to the parent company was RMB838 million, up by 289.38% yoy and up by 2.6% qoq, hitting new record high again. In the first quarter, the price of photovoltaic glass remained in a high range between RMB40 and RMB32 per square meter, which was approximately RMB11 to RMB14 higher than the same period in previous years. It is a prerequisite for photovoltaic glass manufacturers to maintain high profitability. In terms of product mix, the proportion of thin glass with high gross margin increased to over 30% by 19 ppts yoy. The continued optimization of the product mix increased the gross margin. The Company recorded a 58.2% gross margin in the first quarter, an increase of 18.4 ppts yoy, and a slightly decrease of 0.3 ppts qoq.

The Company displayed good performance in period expense ratio. The sales, administrative, R&D and financial expense ratios changed by -1.5 ppts, +0.7 ppts, +0.9 ppts, and -2.1 ppts, respectively. The administrative expenses increased, mainly due to the rise in share incentives and employee salaries. The R&D expenses climbed mainly because of more R&D projects. The main reason for the decrease in financial expenses was the decrease in interest expenses and the growth in exchange gains. The final net profit margin was 40.74%, up by 22.9 ppts yoy and up by 4.33 ppts qoq. The profitability indices all hit record highs.

From the end of March to early April, with the rapid release of industry supply, the downstream gradually entered the off-season, and the demand growth rate slowed down. The Company took the initiative to significantly lower product prices by approximately 30%. It is expected to ease downstream cost pressures and increase demand. On the other hand, it will also help restrain the excessive expansion of the industry production capacity and optimize the industry supply. Benefiting from the advantages in technology, scale, capital and customers, the Company's cost advantages will become more prominent as market price falls. Its market share is expected to increase. On March 29, the Company announced that it would invest RMB5.8 billion to add six new production lines with production capacity of 1,200 tons per day (two production lines in Jiaxing + four production lines in Anhui). The production lines are expected to be put into production in 2022-2023. At the end of 2020, the Company's production capacity was approximately 6,400 tons per day. The current production capacity is 8,600 tons per day. By the end of this year, the production capacity is expected to reach 12,200 tons per day. After full production, the Company's total production capacity is expected to reach 19,400 tons per day, with its leading position more stabilized.

TMT & Education (Kevin Chiu)

This month, I have released an update report of Archosaur Games (9990.HK).

The company's revenue was RMB 1.21 billion (+13.3% YoY) in 2020. Within it, the revenue of the developing and licensing sector /the integrated game publishing and operation sector were RMB 597.3/611.5 million (-27.3% YoY/+148.9% YoY), respectively. In terms of the geographical breakdown, the company's revenue from overseas region in 2020 was RMB 788.3 million (+129.1% YoY), with a revenue proportion of 65.2% (+33.1ppts YoY). The high growth in revenue from overseas region was mainly attributable to the impressive performance of Dragon Raja (Às±Ú¤Û·Q). On the other hand, the revenue from domestic region in 2020 was RMB 420.5 million (-41.8% YoY), with a revenue proportion of 34.8% (-33.0ppts YoY). The steep decline in domestic revenue was primarily due to the delay of the launching of the Under the Firmament¡]ÂE¹Ï¤§¤U¡^and The New World¡]¹Ú·Q·s¤j³°¡^in 2020.

The company's GP in 2020 was RMB 925.9 million (+4.1% YoY), with respective GPM at 76.6%(-6.8ppts YoY). The YoY drop in GPM was mainly due to the fact that the revenue proportion of the integrated game publishing and operation sector rose in 2020 and the GPM of the sector is lower in general comparing to the developing and licensing sector, hence dragging down the company's overall GPM (the integrated game publishing and operation sector recognized the full gross billing as revenue, while gross billings` share to payment channels and distribution channels are recognized in the CoGS, hence lower GPM).

In terms of the expenses, the company's R&D expense / selling expense in 2020 were RMB 540.4 million (+38.8% YoY)/RMB 161.0 million (+40.6% YoY), with respective expense ratios of 44.7% (+8.2ppts YoY)/13.3% (+2.6ppts YoY). The increase in both R&D expense and selling expense ratios was mainly attributable to the mismatch in return vs investments (the delays in the launching of games caused a drop in the revenue growth, while the growth rates of expenses were quicker than that of the revenue). The admin expense of the company in 2020 was RMB 138.3 million (+160.9% YoY), with corresponding expense ratio of 11.6% (+6.2ppts YoY). The rose in the admin expense ratio was mainly due to the one-off listing expense recorded in 2020. The adjusted NP of the company in 2020 was RMB 218.8 million (-38.3% YoY), which is in line with our previous forecast.

Following the successful launch of Dragon Raja (Às±Ú¤Û·Q) in China, the company had successfully launched four new regional versions of Dragon Raja (Às±Ú¤Û·Q) in Europe and the Americas, Japan, Southeast Asia and Vietnam with outstanding results. In specific, the Japanese version of Dragon Raja (Às±Ú¤Û·Q) became the first Chinese mobile MMORPG to top the Top Free Games Charts of both iOS App Store and Google Play in Japan, once again demonstrating the company's leading R&D and distributing capabilities in MMORPG game genre. On the other hand, the company will continue to expand the game genres in its game portfolio, including SLG and female-oriented game genres. In particular, Under the Firmament (ÂE¹Ï¤§¤U) launched in October 2020 is the company's first try in SLG and the gross billing of the game exceeded the RMB 100 million mark in the first month since launching.

Tencent has further accumulated the company's share, increasing its shareholdings to 16.88% from 12.88%, fully demonstrated Tencent's high recognition of the company's R&D capabilities.

Consumer & Property Management (Timothy Chong)

I have released there update reports covering Anta Sports (2020.HK), Xtep INTL(1368.HK) and Eversunshine LS (1995.HK) this month. Between them, we highly recommend Eversunshine LS (1995.HK).

Eversunshine's annual revenue was CNY 3.12 billion, an increase of 66.1% Yoy. In terms of business, Property management services revenue recorded CNY 1.757 billion, an increase of 64.2%, while Community VAS and VAS to non-property owners increased 63.8% and 76.1% Yoy to CNY 790 million and 572 million. Property management services are the company's main source of revenue, accounting for 56.4% of the total revenue. Community VAS and VAS to non-property owners are 25.3% and 18.3%, respectively. The proportion of revenue from Community VAS has increased, an increase of 3.6 ppts from last year. Mainly due to the continuous expansion of customer base and expansion of business scope. As of December 31, 2020, the company's contracted GFA reached 181 million square meters, with 985 contracted projects, an increase of 63.9% and 61.7% Yoy; GFA under management 102 million square meters, an increase of 56.0% Yoy, and the company have sufficient reserves GFA, about 79 million square meters, the future growth is expected to be sustainable.

The company also gave guidance on profit growth in the next three years at the conference meeting. The management expects that between 2020 and 2023, profits will grow at a CAGR of 45%-55%, which is in line with the company's previous five-year tenfold growth target in 2019 which the company's net profit in 2018 is approximately CNY 100 million, and the company's revenue guidance will reach CNY 1 billion in 2023. According to the company's current operating conditions, we believe that the company can complete its strategic goals on schedule.

The company announced on April 14 that it would terminate the acquisition of 65% of the issued share capital of Zhangtai Service Group Company Limited, mainly due to the determination after due diligence and further consideration of all circumstances of the acquisition. Zhangtai Service is a reputable property management services provider in Guangxi Zhuang Autonomous Region, China. The contracted GFA is approximately 24.78 million square meters, of which GFA under management is approximately 11.97 million square meters. The original purchase price was approximately CNY 434 million, which corresponds to approximately 8x FY20 P/E. On April 16, another company announced the acquisition of an 80% stake in Zhangtai at a consideration of CNY 800 million, corresponding to FY20 P/E of 12x. We believe that although this incident has hindered the company's acquisition and development process, it also reflects the company's detailed acquisition considerations while industry integration. The company's current cash level is sufficient. As of December 31, 2020, the company's cash level is CNY 3.171 billion. It can also be properly grasped when there are new acquisition targets in the future, and expand different business formats through mergers and acquisitions.

Click Here for PDF format...